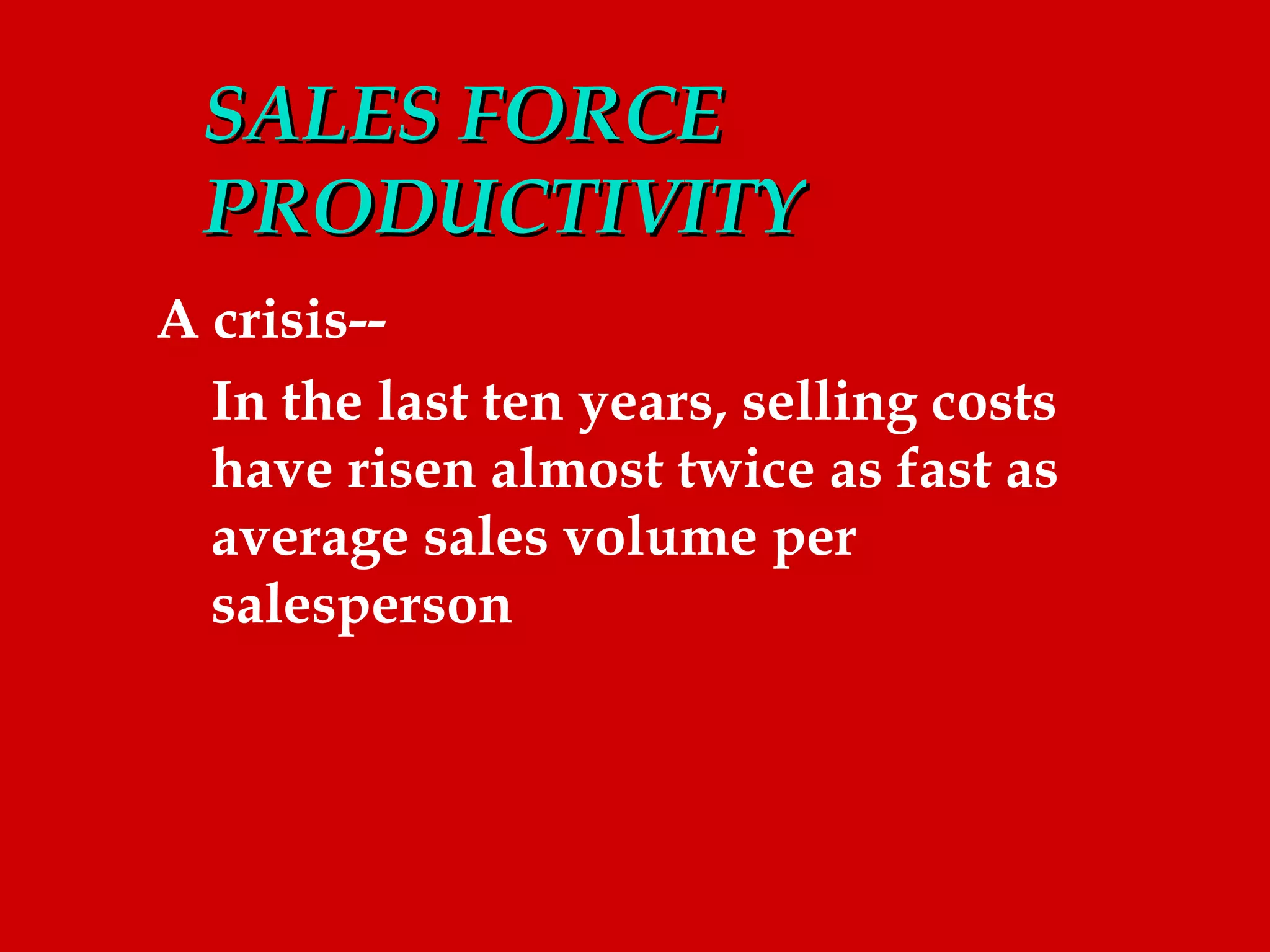

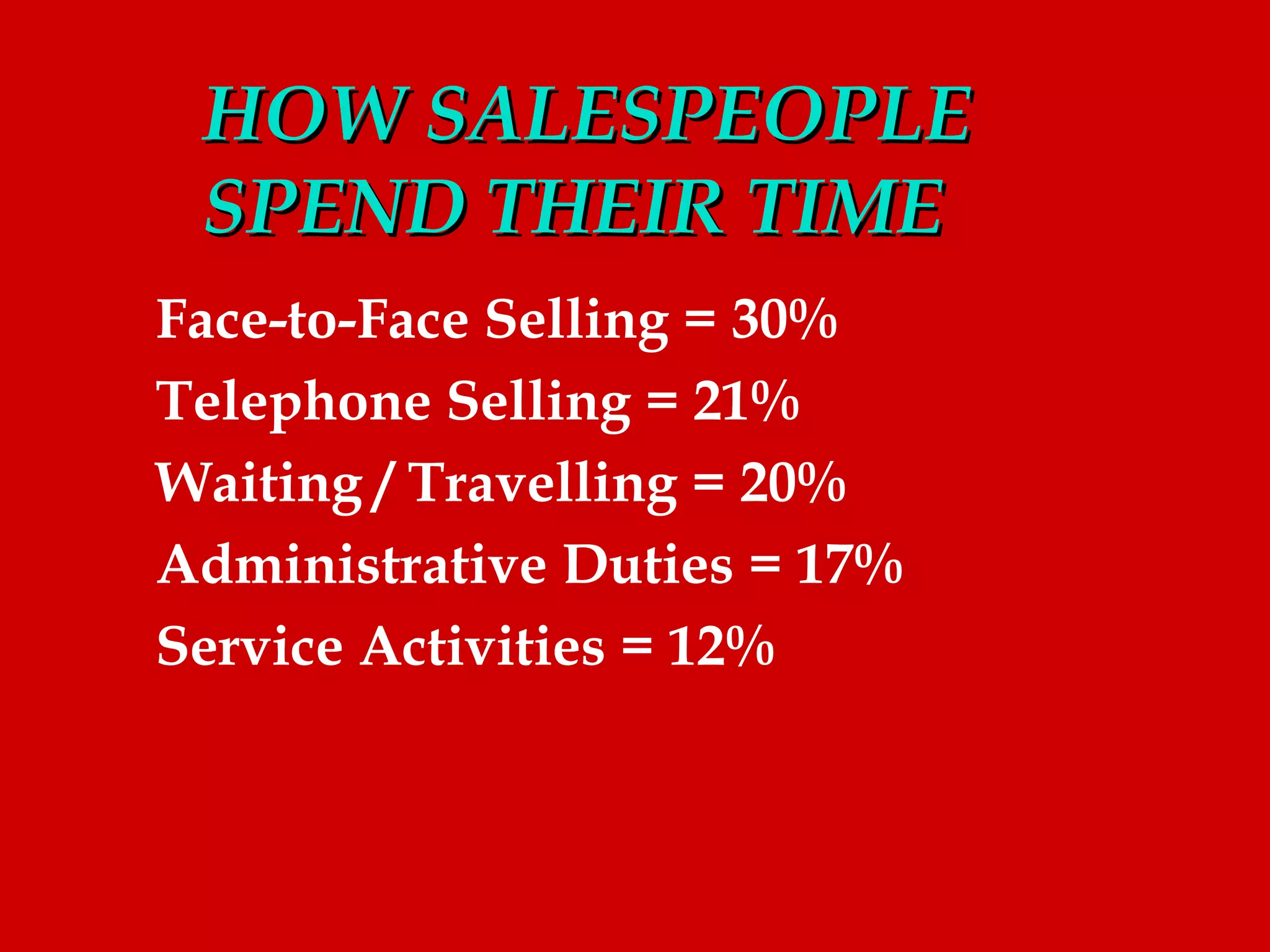

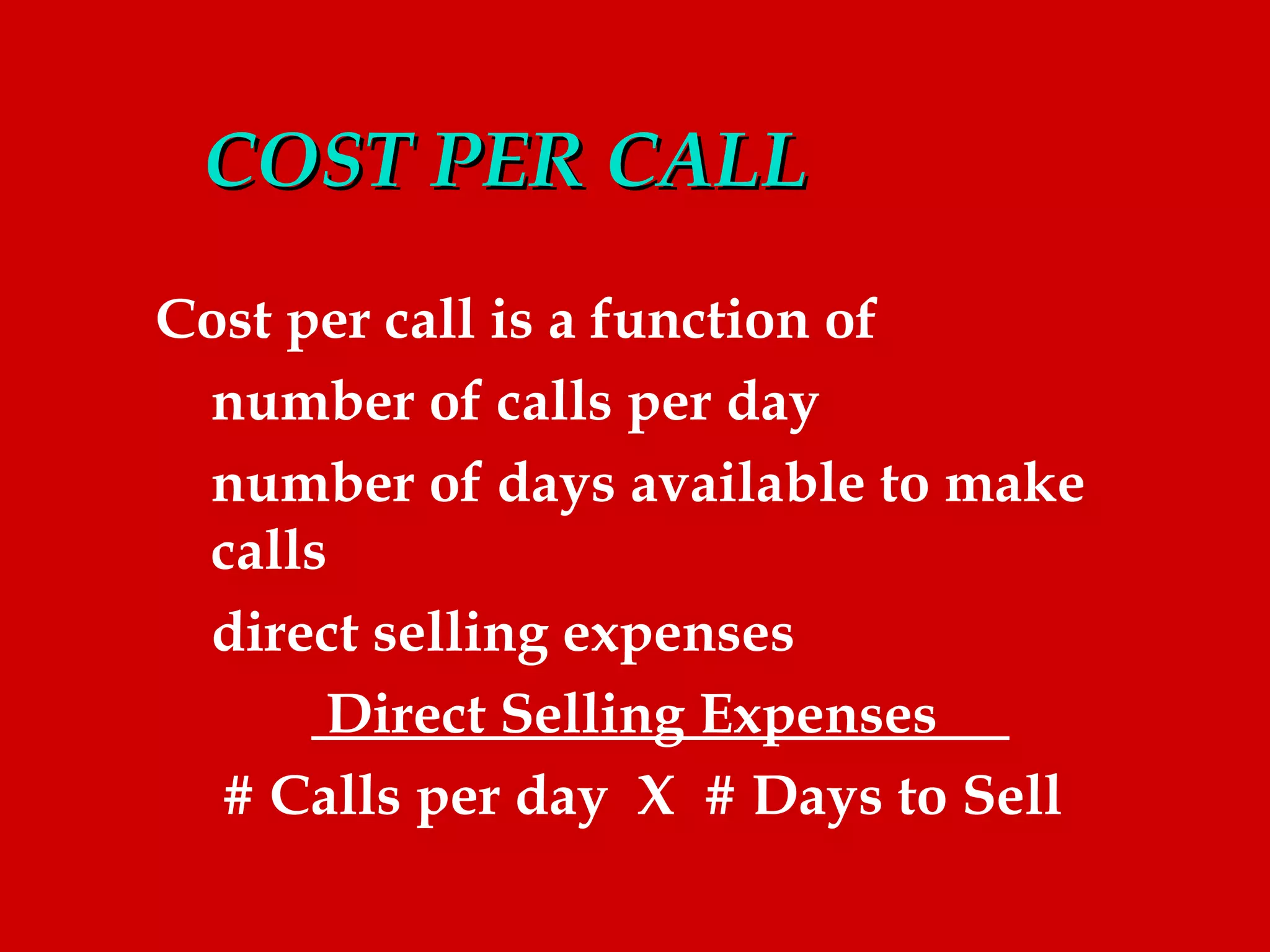

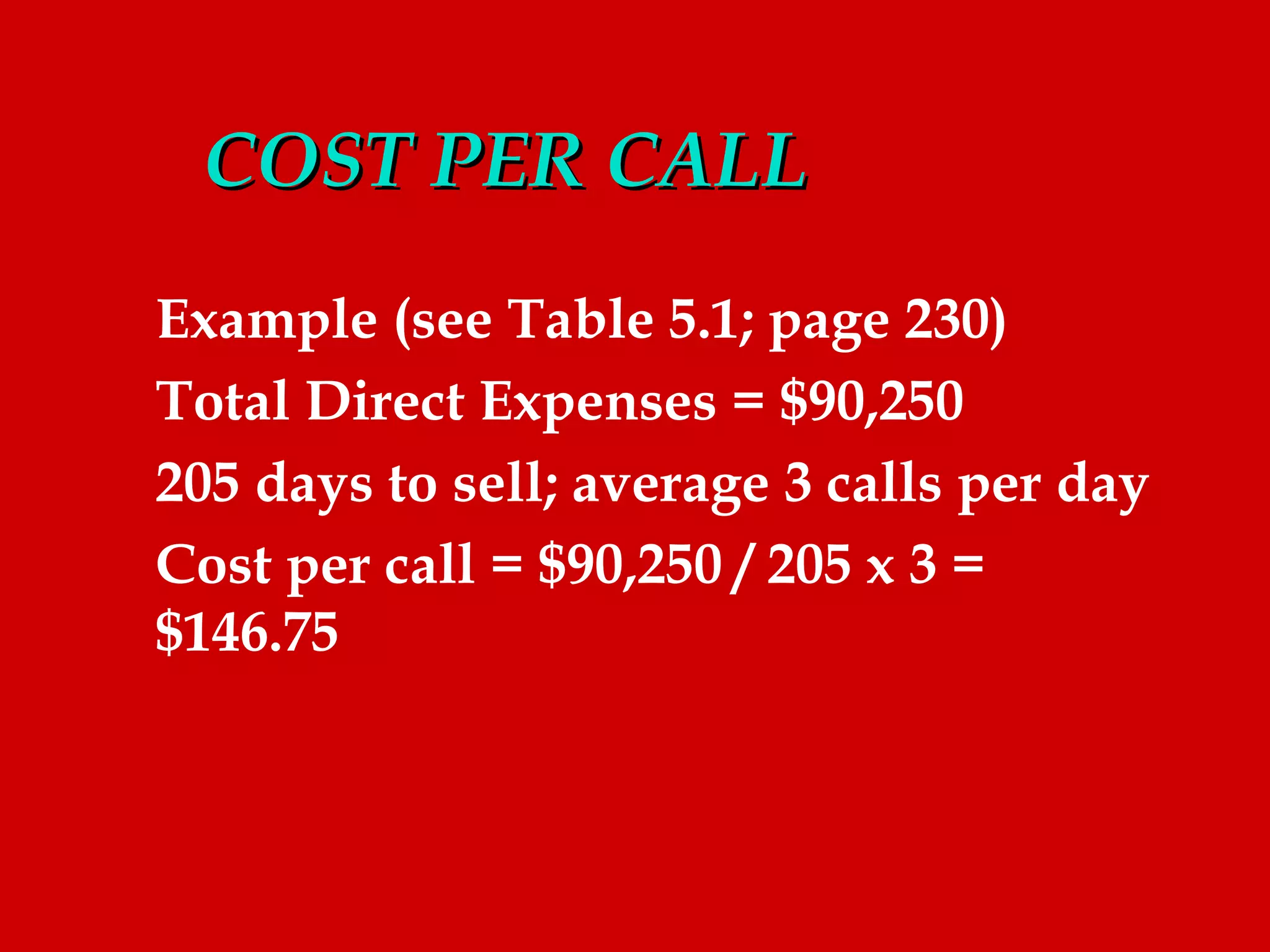

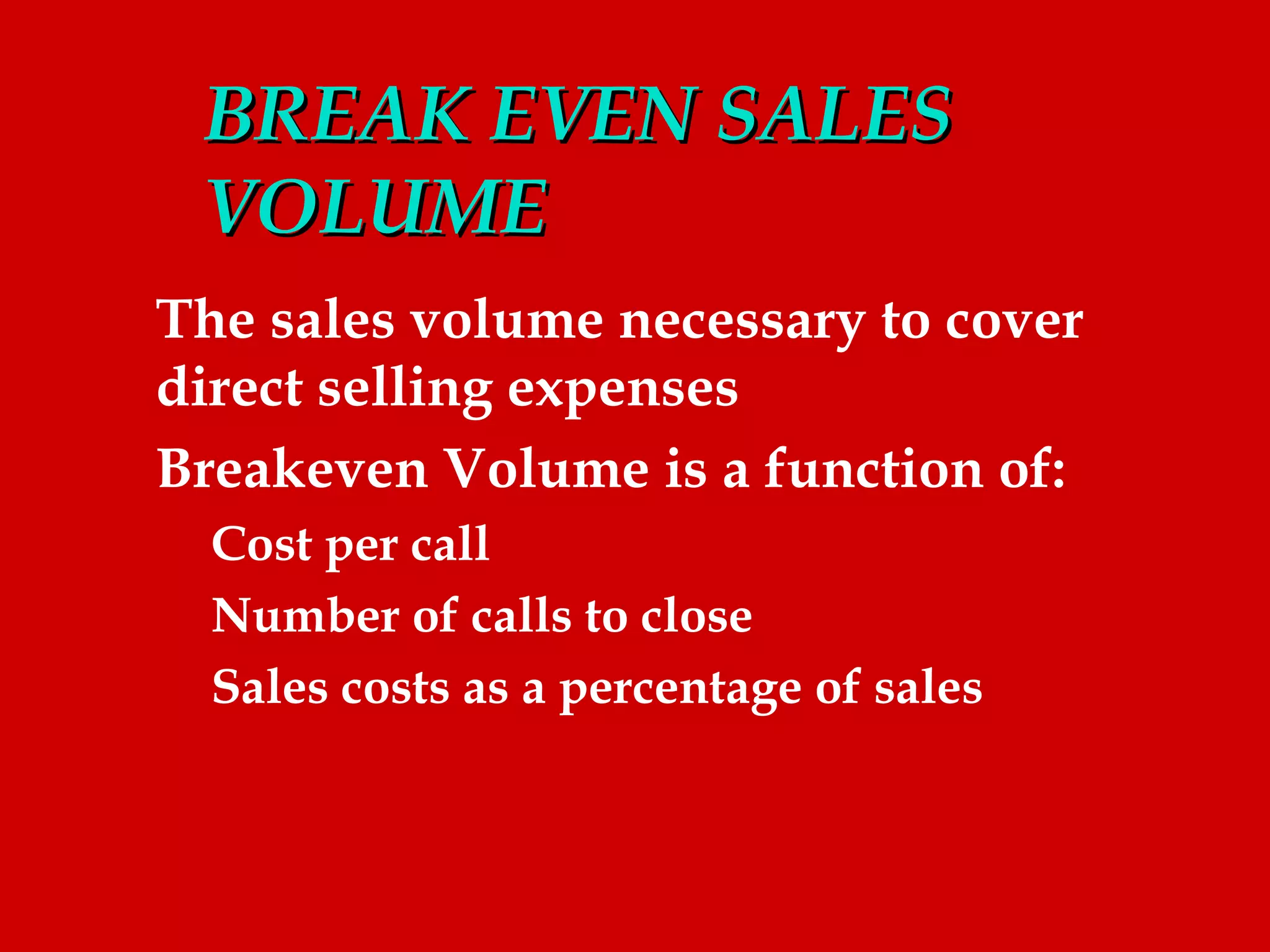

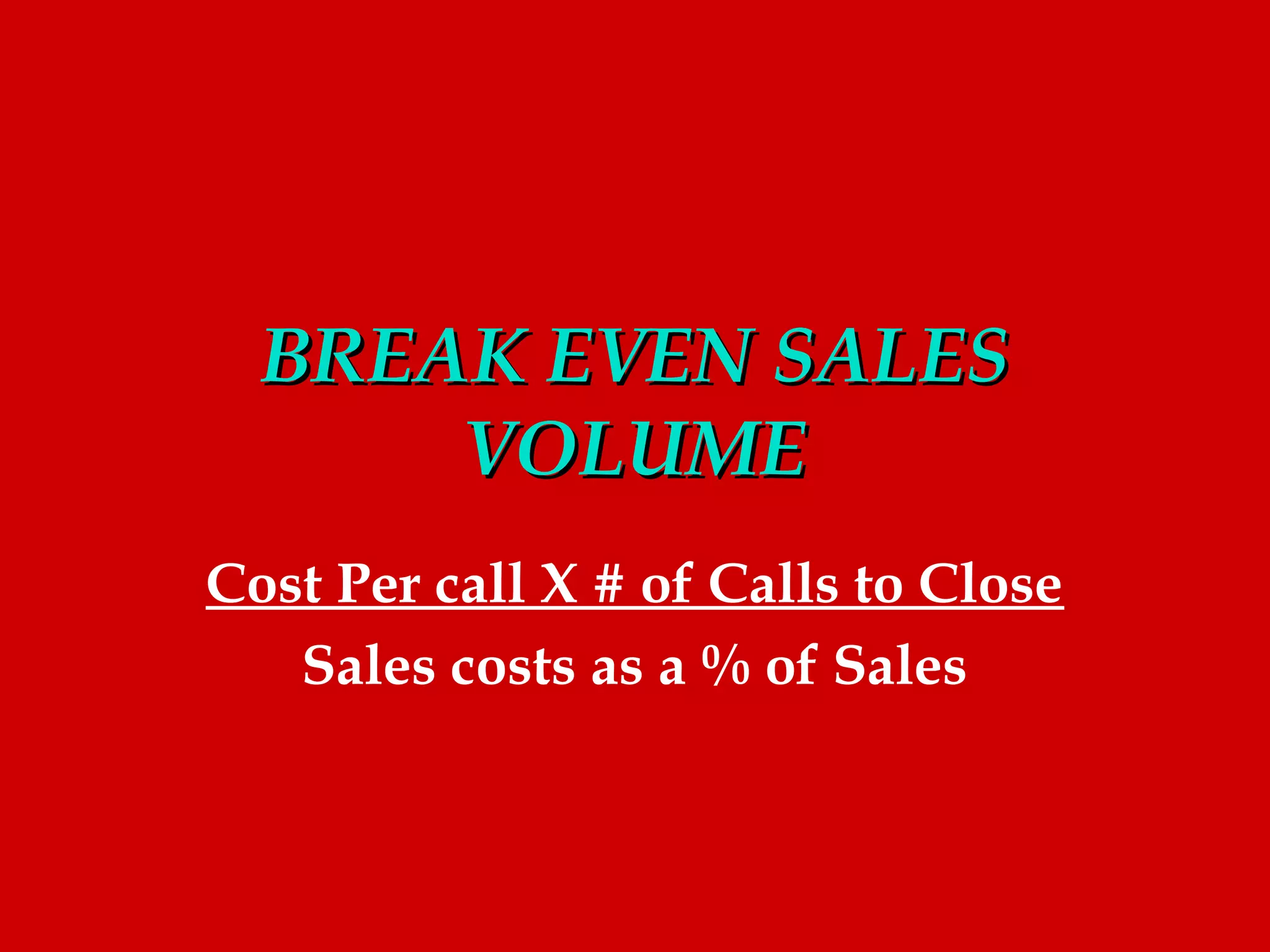

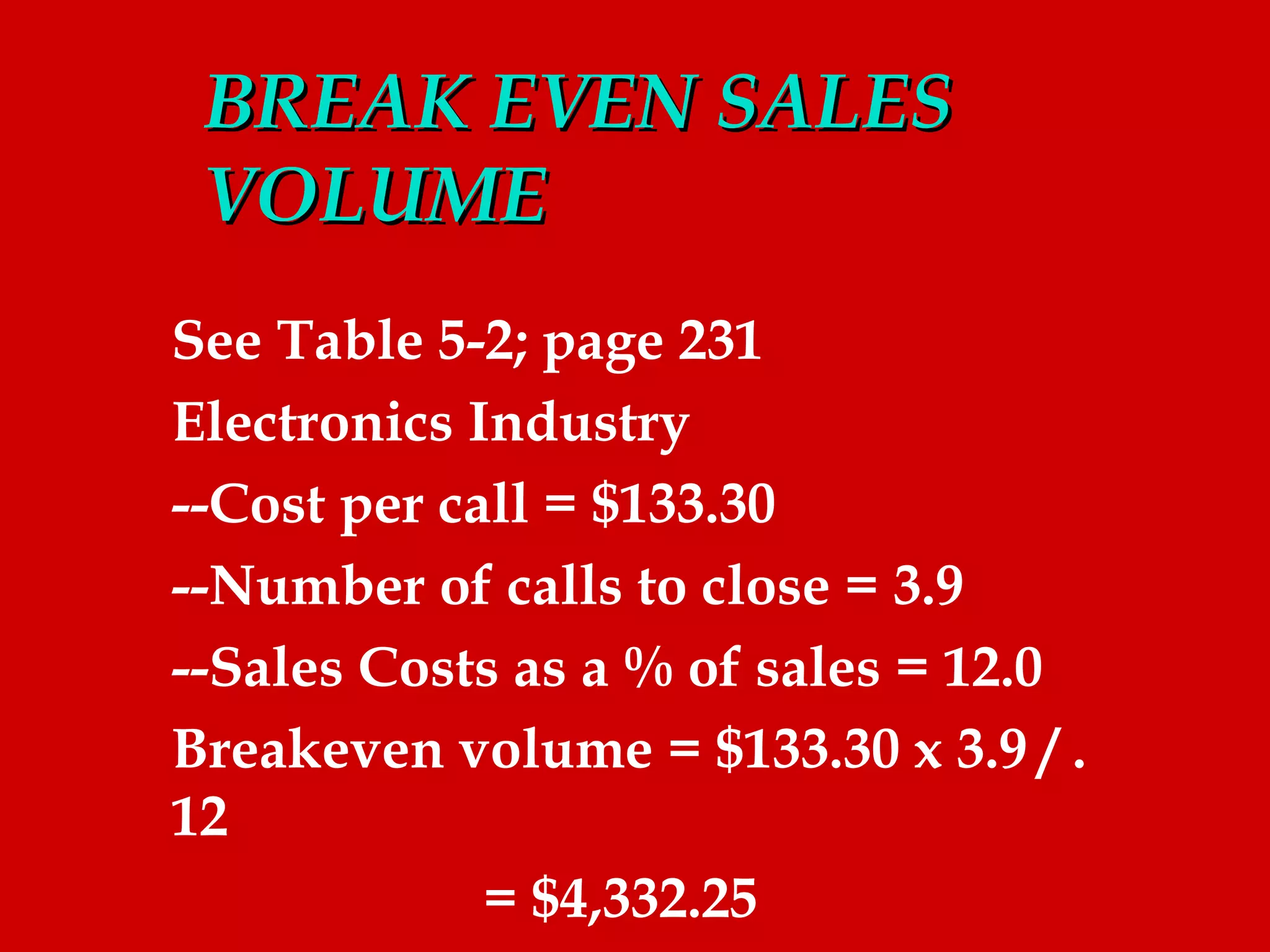

This document discusses territory management and sales force productivity. It notes that selling costs have risen faster than sales volume per salesperson. Salespeople spend only 30% of their time doing face-to-face selling. To improve productivity, the document recommends focusing on high volume accounts and selling time. It also advises not pursuing unprofitable accounts. The concept of cost per call and break even sales volume are introduced to determine the sales needed to cover costs. Different models for allocating selling effort are presented.