Downloaded 38 times

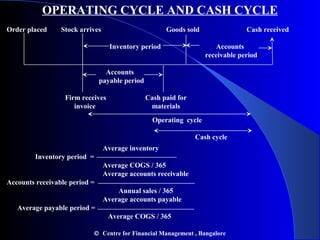

This document discusses working capital management. It defines current assets and outlines factors that influence working capital requirements, such as a firm's nature of business and production seasonality. The document also discusses determining the optimal level of current assets by balancing liquidity and carrying costs. Additionally, it examines financing current assets through a mix of long-term and short-term sources and calculating cash requirements for working capital based on a firm's operating cycle.

![Dividends and _dividend_policy_powerpoint_presentation[1]](https://cdn.slidesharecdn.com/ss_thumbnails/dividendsanddividendpolicypowerpointpresentation1-130929215028-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)