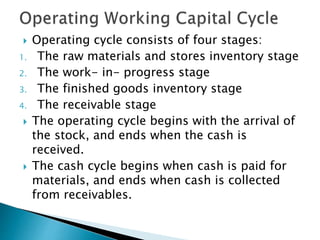

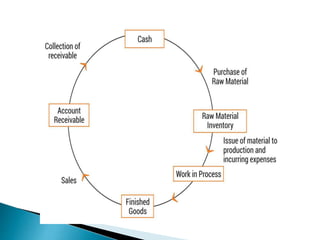

The document provides an extensive overview of working capital (w.c.) in accounting, defining it as the difference between current assets and liabilities, and exploring various types including net working capital, gross working capital, and permanent working capital. It discusses factors influencing working capital requirements, such as industry nature, sales volume, and business cycles, emphasizing the importance of efficient management to meet operational needs and maintain liquidity. Additionally, the text highlights the significance of the operating cycle in determining working capital needs and mentions different financing options for current assets.