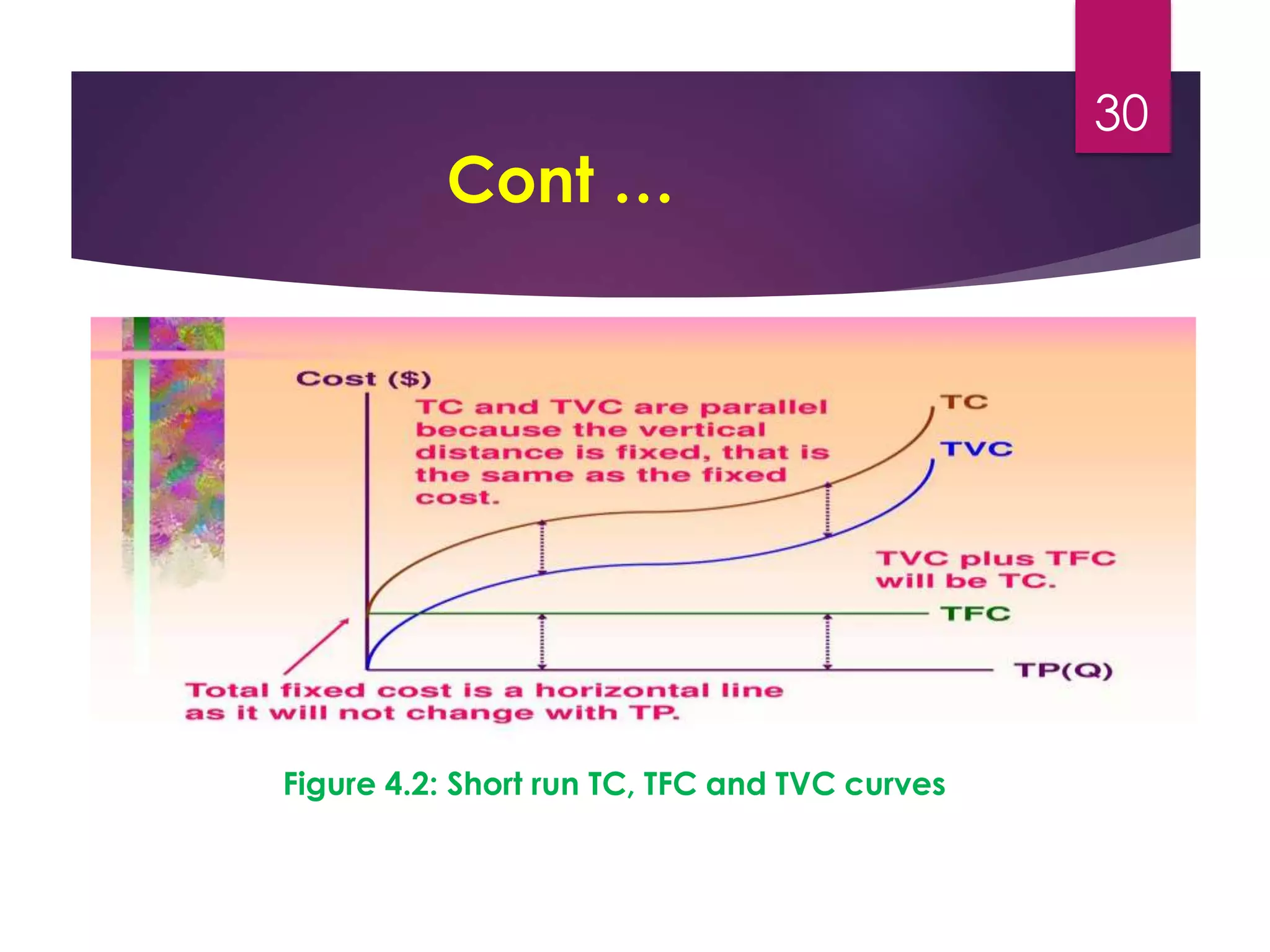

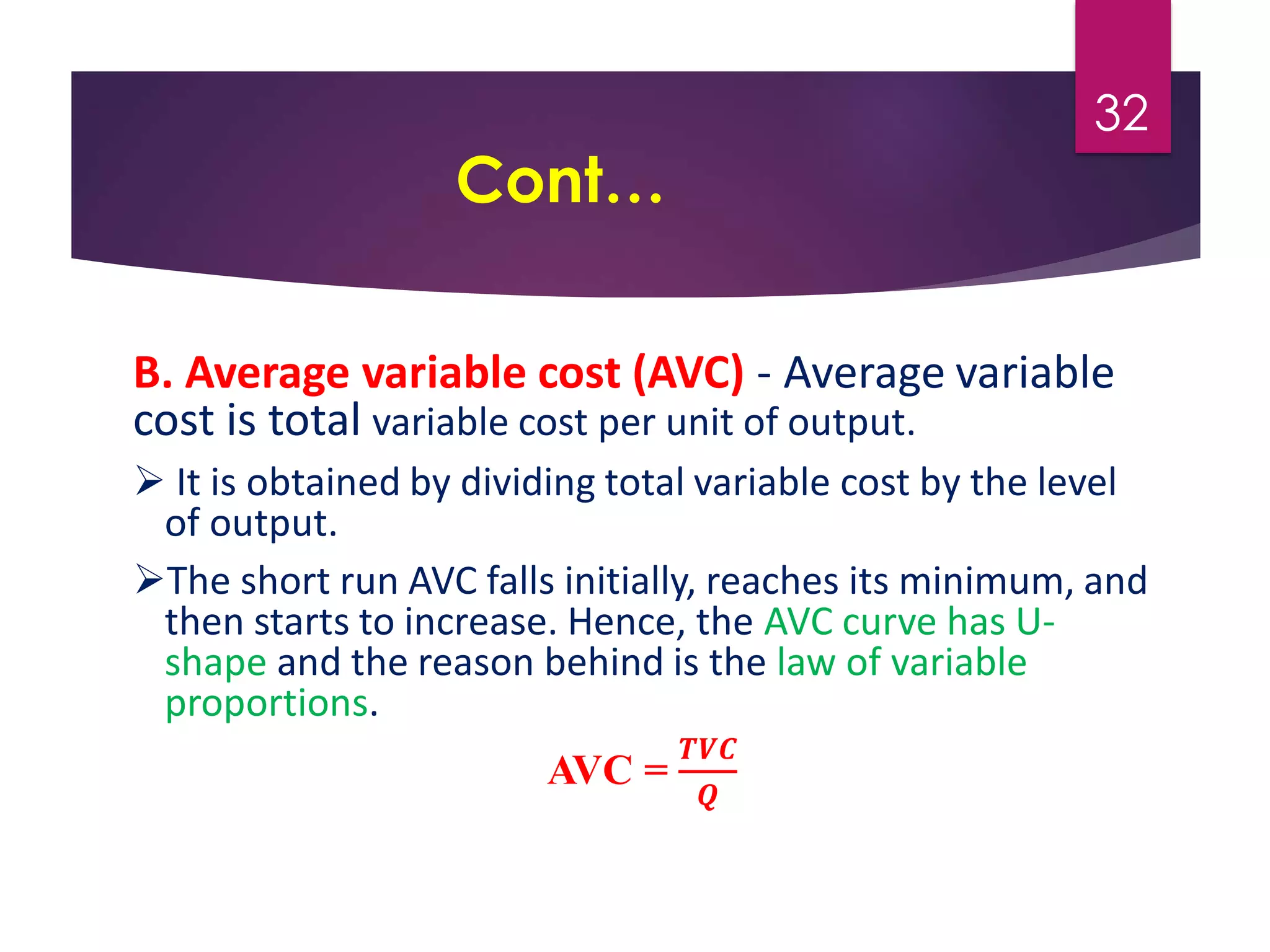

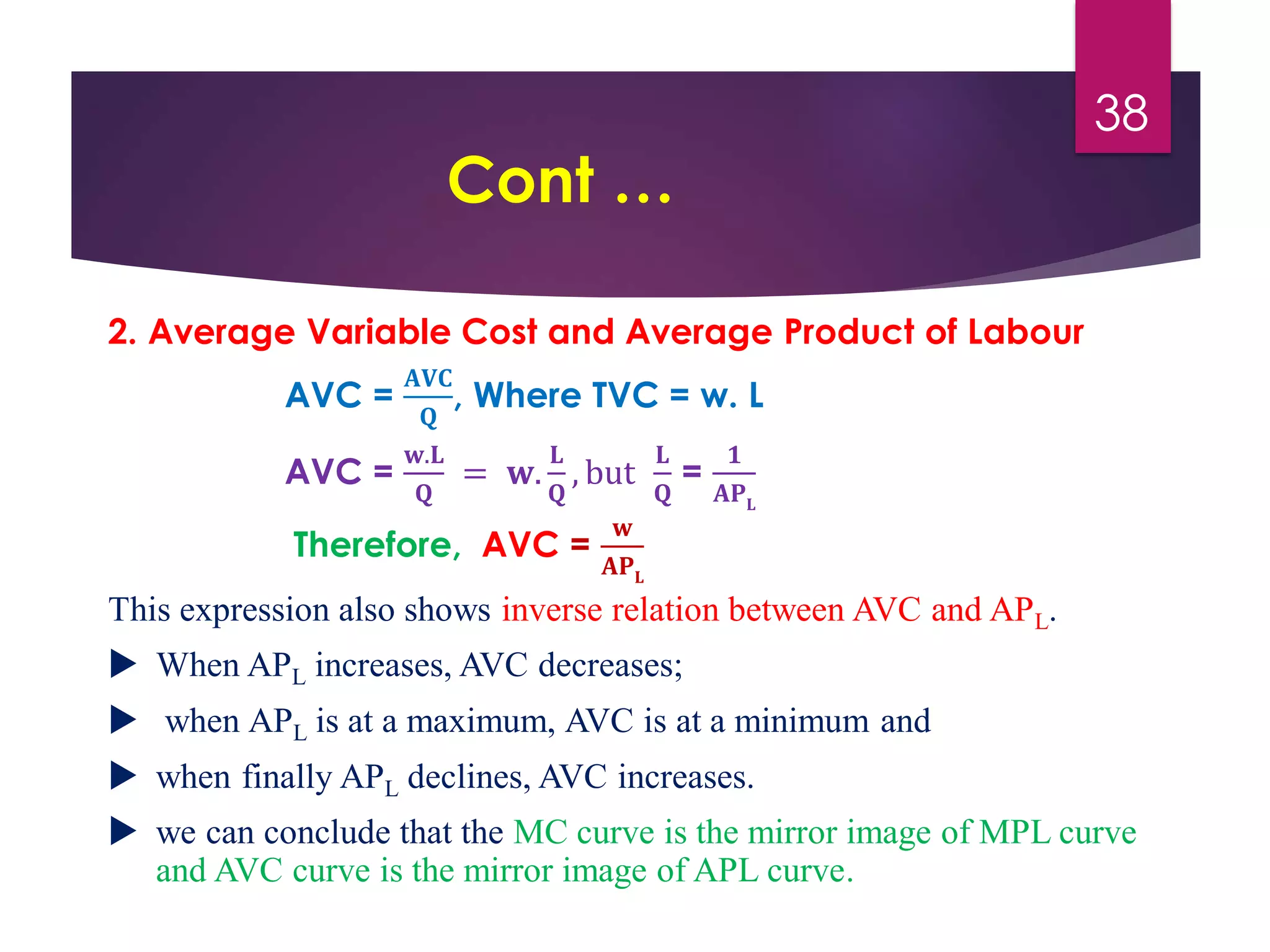

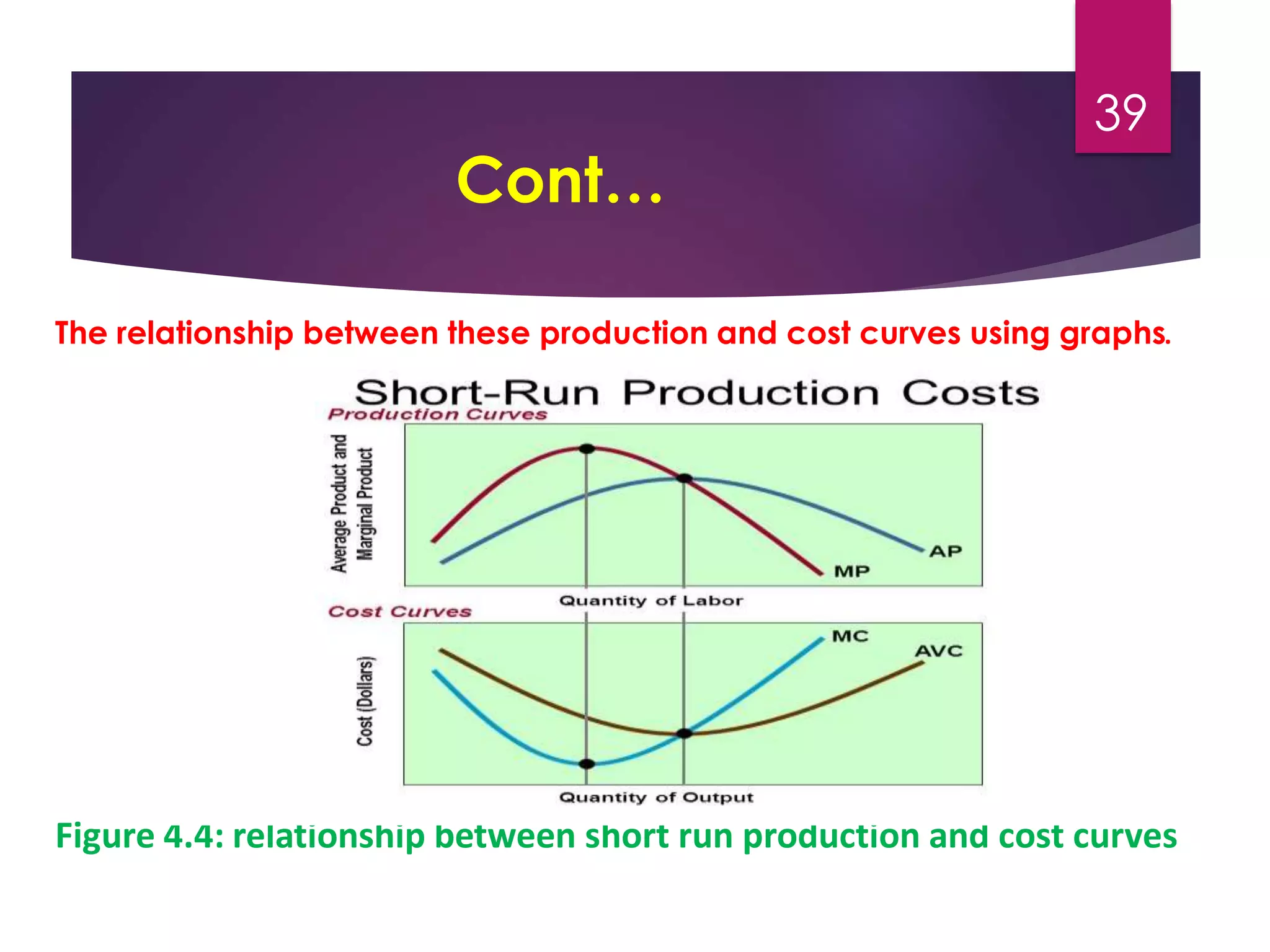

The document discusses the theory of production and costs in the short run. It defines production as the process of transforming inputs into outputs. The production function shows the maximum output that can be produced from a fixed amount of inputs using existing technology. In the short run, at least one input is fixed, while variable inputs can be changed. Total, average, and marginal product are discussed in relation to variable inputs. Total cost is the sum of total fixed costs, which do not vary with output, and total variable costs, which do vary with output. Average and marginal costs are also discussed. The relationships between production and cost curves are explained, showing marginal cost is the mirror image of marginal product and average variable cost is the mirror image of