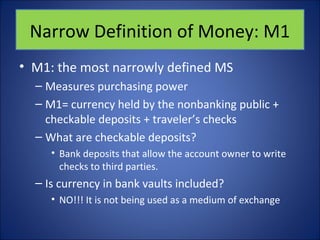

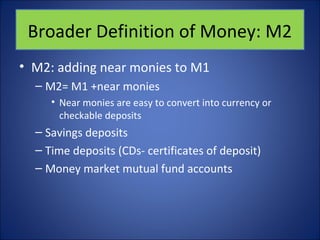

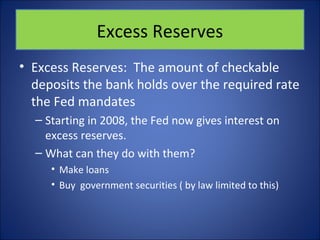

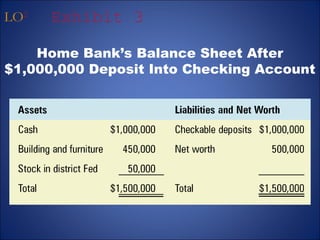

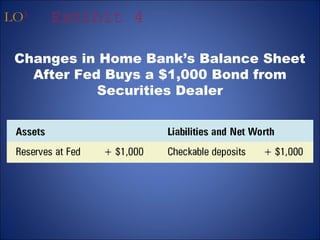

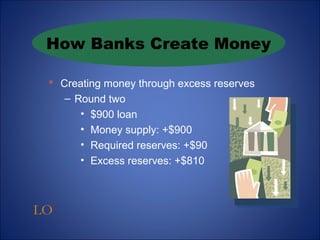

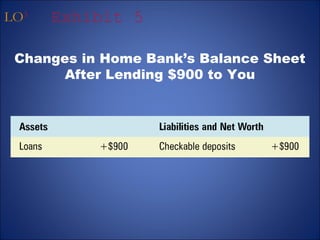

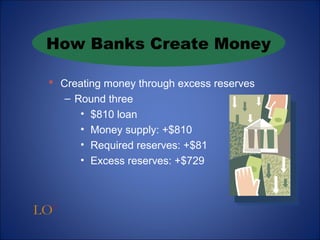

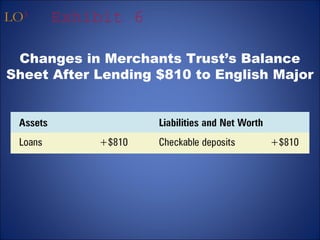

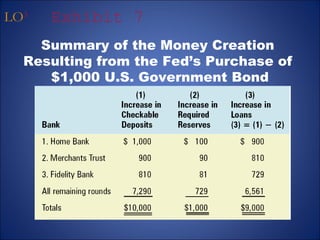

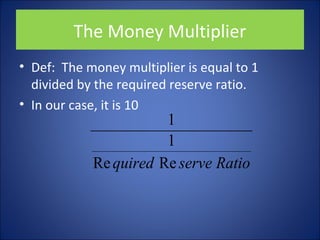

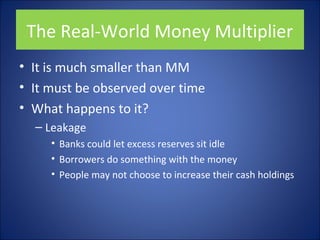

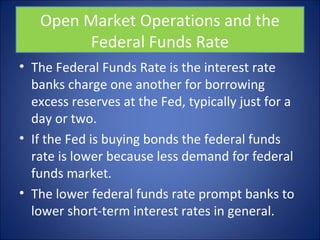

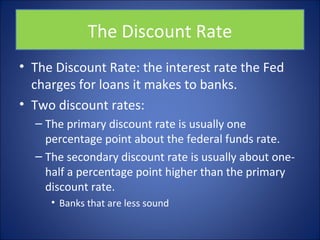

This document discusses measures of the money supply (M1 and M2) and how banks create money through the money multiplier effect. It explains that the money supply expands as banks make loans from their excess reserves. The money multiplier is equal to 1 divided by the required reserve ratio, so in this example the money multiplier is 10. When the Fed conducts open market operations by buying bonds, it increases bank reserves and allows the money supply to expand through additional lending. The Fed uses tools like open market operations, reserve requirements, and interest rates to influence the money supply and control monetary policy.