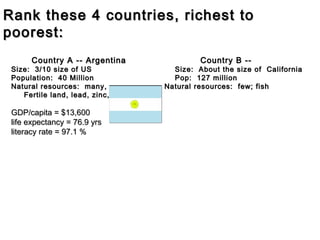

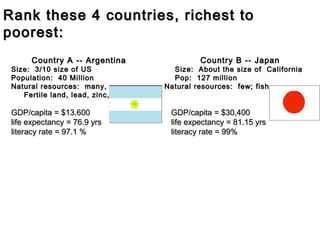

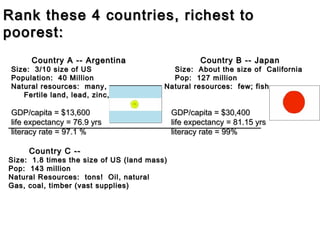

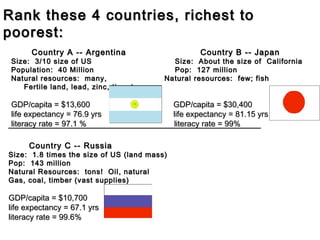

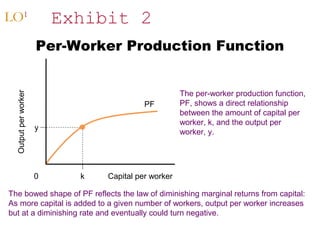

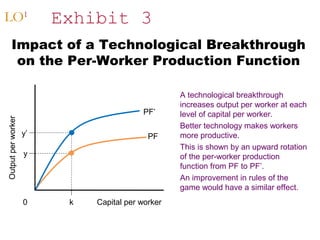

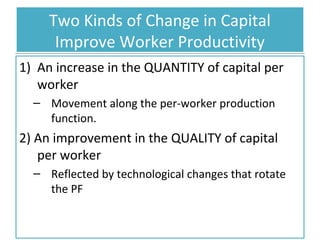

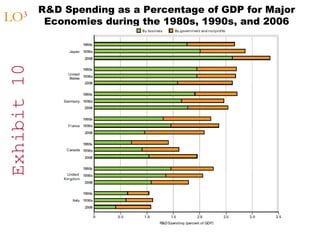

The document discusses productivity and economic growth. It begins by defining productivity as the efficient use of resources and measuring it as the ratio of total output to a specific input, such as labor. Productivity increases when there is more capital investment per worker (capital deepening) or technological improvements. Countries with higher levels of education, political stability, defined property rights, and greater investments in research and development tend to be more productive and have higher standards of living. While technological change may temporarily displace some workers, it ultimately benefits the economy by increasing productivity and the availability of affordable products.