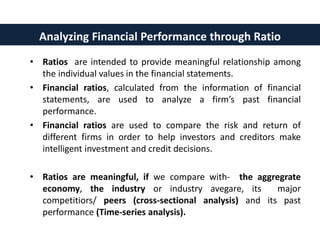

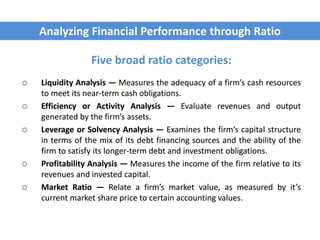

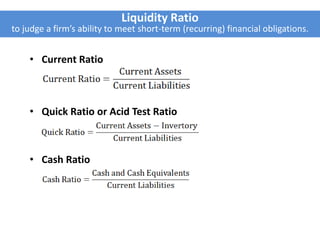

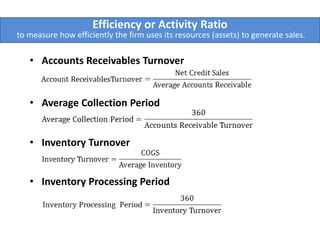

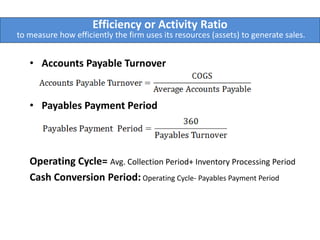

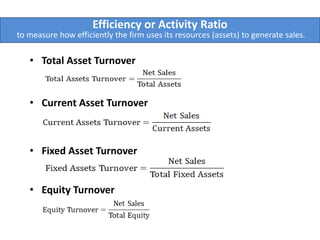

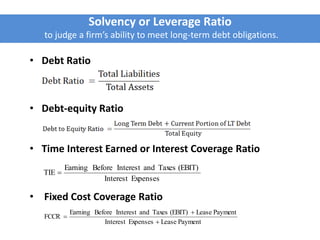

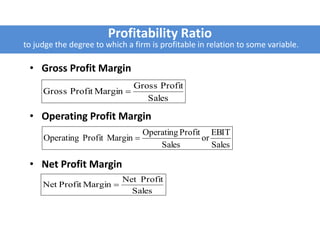

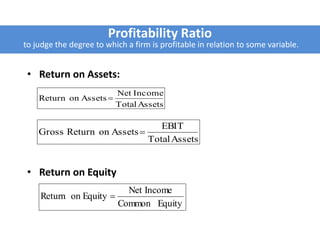

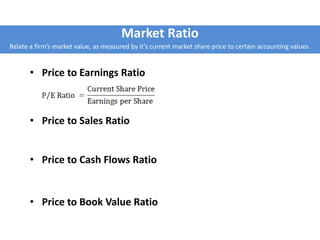

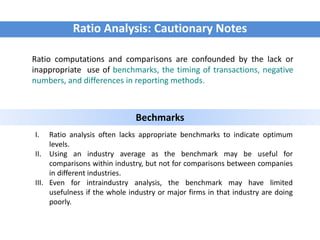

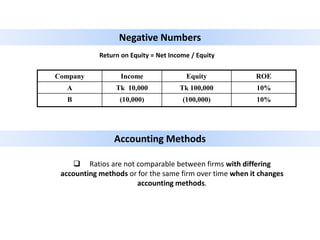

The document discusses various methods for analyzing the financial performance of a company through its financial statements, including ratio analysis, common size analysis, trend analysis, DuPont analysis, and other types of analyses. It provides examples of different types of ratios that can be used, such as liquidity ratios, activity ratios, leverage ratios, and profitability ratios. It also discusses how to interpret ratios and cautions that ratios must be compared to benchmarks and should account for differences in accounting methods.