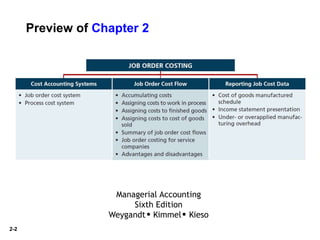

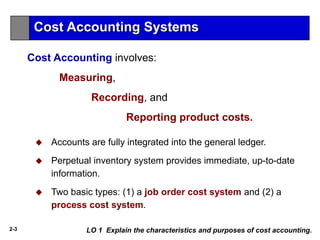

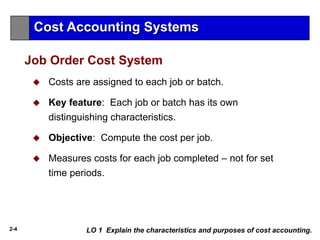

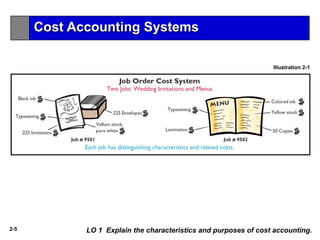

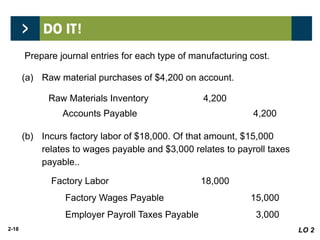

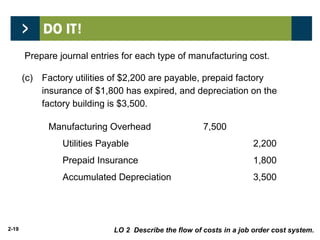

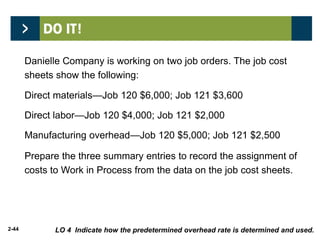

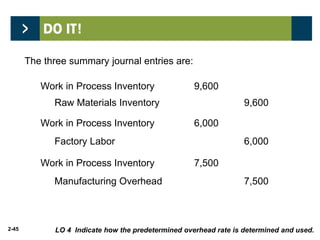

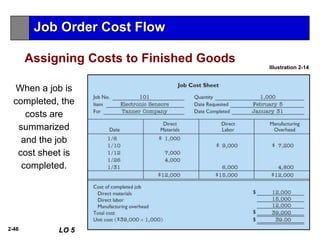

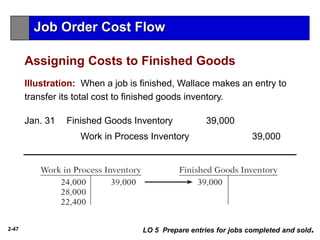

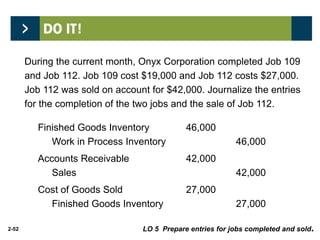

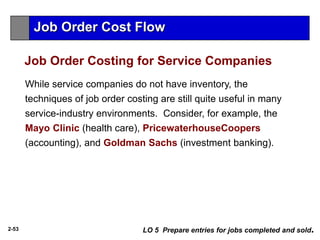

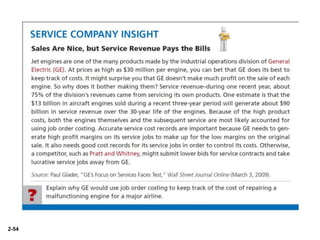

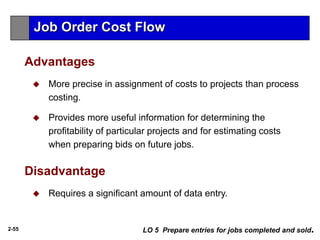

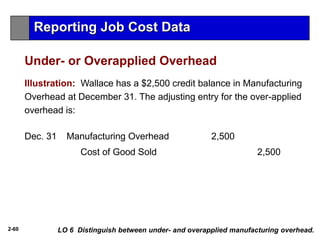

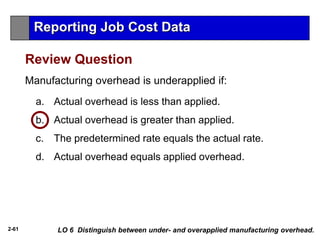

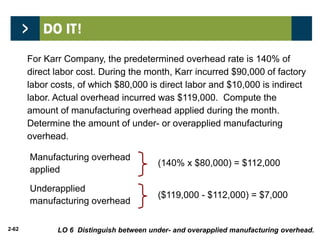

The document outlines job order costing in managerial accounting, highlighting objective characteristics and purposes, the flow of costs, and the job cost sheet's importance. It explains cost accumulation for specific jobs, the determination and application of predetermined overhead rates, and entries for completed and sold jobs. Additionally, it addresses the advantages and disadvantages associated with job order costing in both manufacturing and service industries.

![2-1

Job Order Costing

Learning Objectives

After studying this chapter, you should be able to:

[1] Explain the characteristics and purposes of cost accounting.

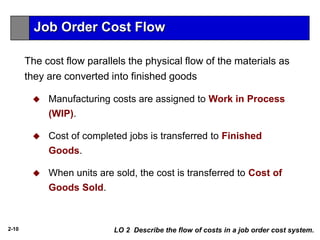

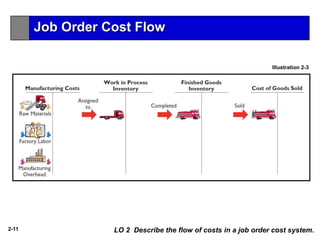

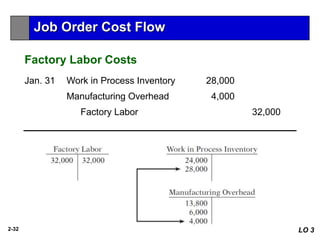

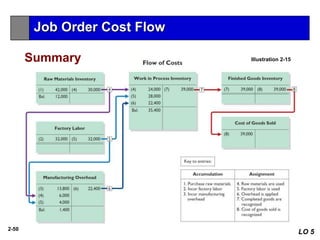

[2] Describe the flow of costs in a job order cost system.

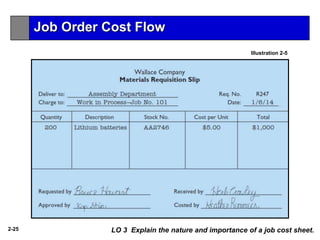

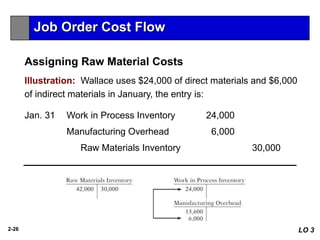

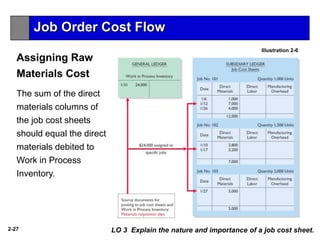

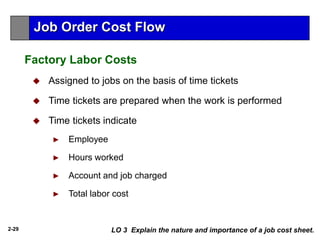

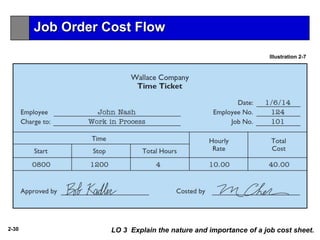

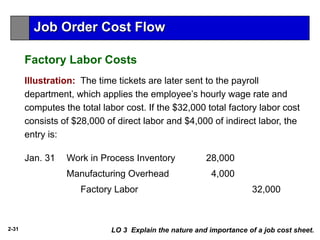

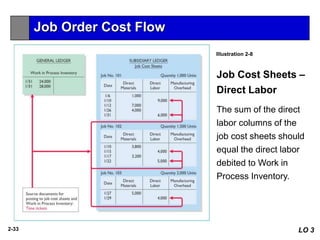

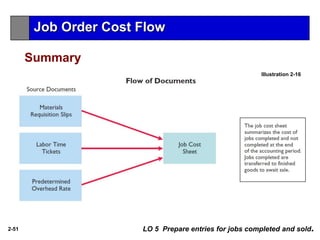

[3] Explain the nature and importance of a job cost sheet.

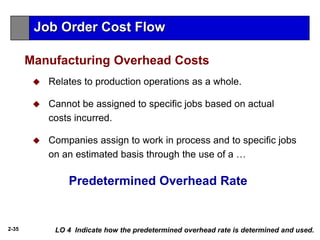

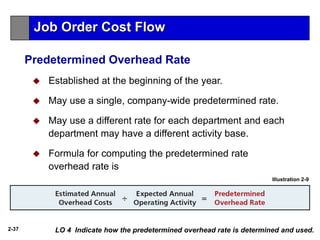

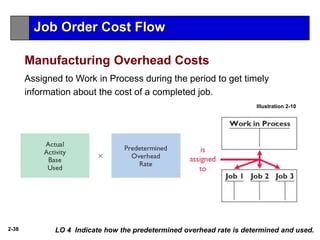

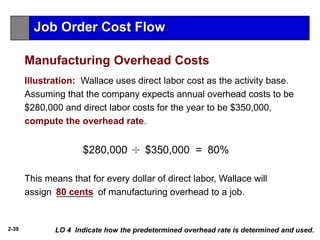

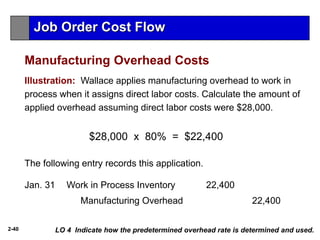

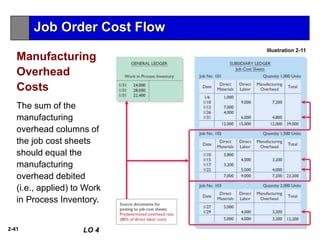

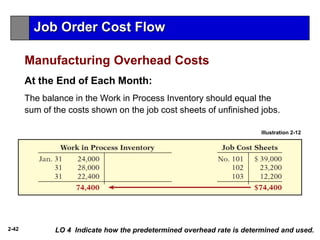

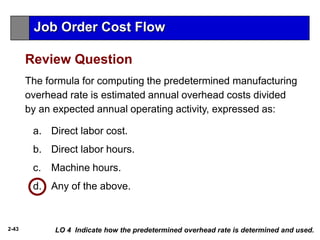

[4] Indicate how the predetermined overhead rate is determined and used.

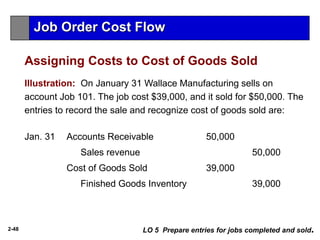

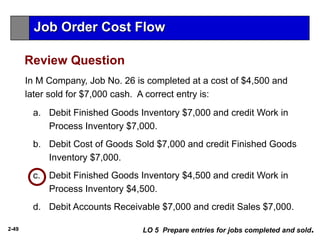

[5] Prepare entries for jobs completed and sold.

[6] Distinguish between under- and overapplied manufacturing overhead.](https://image.slidesharecdn.com/ch02managerial-240501164931-5201104d/85/chapter-02-managerial-accounting-job-order-1-320.jpg)

![2-1

Job Order Costing

Learning Objectives

After studying this chapter, you should be able to:

[1] Explain the characteristics and purposes of cost accounting.

[2] Describe the flow of costs in a job order cost system.

[3] Explain the nature and importance of a job cost sheet.

[4] Indicate how the predetermined overhead rate is determined and used.

[5] Prepare entries for jobs completed and sold.

[6] Distinguish between under- and overapplied manufacturing overhead.](https://image.slidesharecdn.com/ch02managerial-240501164931-5201104d/75/chapter-02-managerial-accounting-job-order-1-2048.jpg)