Recommended

More Related Content

Similar to 031.ppt

Similar to 031.ppt (20)

Recently uploaded

Recently uploaded (20)

031.ppt

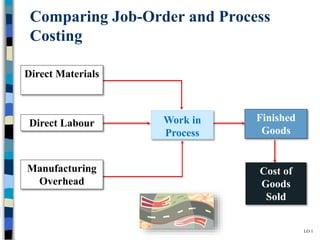

- 1. Comparing Job-Order and Process Costing Finished Goods Cost of Goods Sold Work in Process Direct Materials Direct Labour Manufacturing Overhead LO 1

- 2. Comparing Job-Order and Process Costing Finished Goods Cost of Goods Sold Direct Labour Manufacturing Overhead Jobs Costs are traced and applied to individual jobs in a job-order cost system. Direct Materials LO 1

- 3. Comparing Job-Order and Process Costing Finished Goods Cost of Goods Sold Direct Labour Manufacturing Overhead Processing Department Costs are traced and applied to departments in a process cost system. Direct Materials LO 1

- 4. Basics of Job-Order Costing Process Costing Job-Order Costing Many different products are produced each period. Products are manufactured to order. Costs are traced or allocated to jobs. Cost records must be maintained for each distinct product or job. Next Page Click Here

- 5. Applications of Job-Order Costing Typical job order cost applications: Special-order printing Building construction Also used in the service industry Hospitals Law firms Job-Order Costing Next Page Click Here

- 6. Job No. 1 Job No. 2 Job No. 3 Charge direct material and direct labor costs to each job as work is performed Sequence of Events in a Job-Order Costing System Direct Materials Direct Labor Next Page Click Here

- 7. Apply overhead to each job using the predetermined rate (covered separately). Sequence of Events in a Job-Order Costing System Direct Materials Direct Labor Job No. 1 Job No. 2 Job No. 3 Factory Overhead Next Page Click Here

- 8. Materials Requisition Form Will E. Delite Production managers use materials requisition forms to request materials for manufacturing. This source document is used to assign materials costs to specific jobs (or to overhead). Total cost is transferred to job cost sheet for job A-143 Type, quantity, and total cost of material charged to job A-143. Next Page Click Here

- 9. Employee Time Ticket A worker uses a time ticket to record the time spent on each job (or overhead activity). This source document determines the amount of direct labor that is charged to a job (or the amount of indirect labor that is charged to overhead). Information is transferred to job cost sheet for job A-143 Next Page Click Here

- 10. Job Cost Sheet – Recording Materials and Labor From the materials requisition form The primary document for tracking the costs associated with a given job is the job order cost sheet. From the time ticket Next Page Click Here

- 11. Assume that the company applies (or allocates) overhead to jobs using a predetermined overhead rate of $4 per direct labor hour. Job Cost Sheet – Recording Overhead Next Page Click Here

- 12. Job-Order Costing – Flow of Materials Costs Materials Requisition Record in Manufacturing Overhead Account Direct materials Indirect materials Materials used may be either direct or indirect. Record on each Job Order Cost Sheet and add to Work in Process Account Next Page Click Here

- 13. Job-Order Costing Flow of Labor Costs Employee Time Ticket Record in Manufacturing Overhead Account Direct Labor Indirect Labor An employee’s time may be either direct or indirect. Next Page Click Here Record on each Job Order Cost Sheet and add to Work in Process Account

- 14. Job-Order Costing Document Flow Summary Record in Manufacturing Overhead Account Other Actual Overhead Charges Applied (or allocated) Overhead Materials Requisition Indirect Material Employee Time Ticket Indirect Labor Record on each Job Order Cost Sheet and add to Work in Process Account Next Page Click Here

- 15. Entry to Record Cost Flows – Material Purchases Raw materials purchased are recorded in an inventory account. Next Page Click Here

- 16. Direct materials issued to a job increase the Work in Process account and decrease the Raw Materials account. Indirect materials that are used in the factory increase the Manufacturing Overhead account and decrease the Raw Materials account. Entry to Record Cost Flows – Use of Materials Next Page Click Here

- 17. Entry to Record Cost Flows – Labor The cost of direct labor incurred increases the Work in Process account and decreases the Salaries and Wages Payable account. The cost of indirect labor incurred increases the Manufacturing Overhead account and decreases the Salaries and Wages Payable account. Next Page Click Here

- 18. Entry to Record Cost Flows – Application of Overhead The Work in Process account is increased and the Manufacturing Overhead account is decreased when overhead is applied (or allocated) to jobs. Next Page Click Here

- 19. Entry to Record Cost Flows – Transfer to Finished Goods As a job is completed, the cost of goods that were completed for that job is transferred from the Work in Process account to the Finished Goods account. Next Page Click Here

- 20. Entry to Record Cost Flows – Sale of Job to Customer When a job is sold to a customer on account: (1) the sale is recorded; and (2) the cost of the job is transferred from the Finished Goods account to the Cost of Goods Sold account. Next Page Click Here

Editor's Notes

- The flow of costs through the manufacturing accounts is basically the same for process and job-order costing. Direct materials, direct labour, and manufacturing overhead are added to Work in Process. When work in process is completed, the costs are transferred to Finished Goods. When finished goods are sold, the costs are transferred to Cost of Goods Sold.

- There is a key fundamental difference between process and job-order costing systems. Job-order costing systems trace and apply manufacturing costs to jobs. One Work in Process account is often used to accumulate costs for all jobs. The individual job cost sheets serve as a subsidiary ledger.

- In a process costing systems, costs are traced to departments that process the goods. In some companies there may be several processing departments that goods must pass through to become finished goods. A separate Work in Process account is maintained for each processing department. Material, labour, and overhead costs transferred from one department’s Work in Process account to another department’s Work in Process account are called transferred-in costs.