Download to read offline

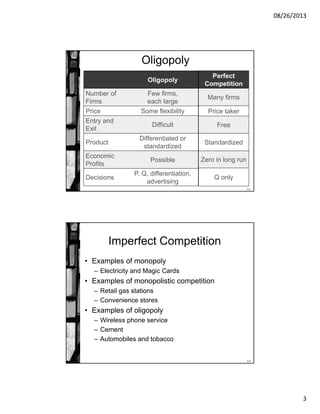

This document provides an overview of imperfect competition, including monopoly, oligopoly, and monopolistic competition. It discusses the key differences between imperfect and perfect competition. Specifically, it covers: 1) The three types of imperfect competition and how they differ from perfect competition in terms of number of firms, price flexibility, entry/exit, and potential for economic profits. 2) The five sources of monopoly power, with a focus on economies of scale as the most enduring source due to decreasing average costs. 3) How monopolists determine profit-maximizing output by setting marginal revenue equal to marginal cost, which results in a smaller output and higher price than the socially optimal level. 4) Examples are provided