Downloaded 91 times

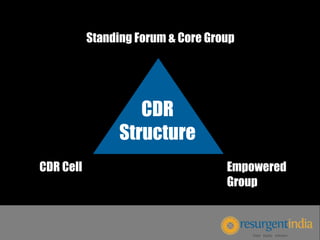

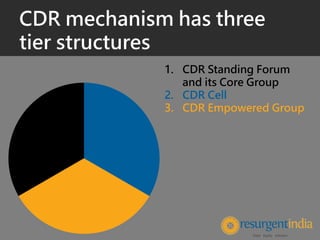

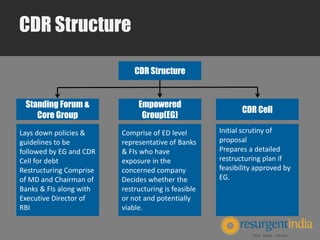

The Corporate Debt Restructuring (CDR) mechanism in India has a three-tier structure to help restructure corporate debt for viable companies facing financial problems. The CDR Standing Forum and its Core Group lay down policies, while the CDR Empowered Group, consisting of executives from participating financial institutions, considers restructuring proposals from the CDR Cell. If a proposal is deemed feasible, the CDR Cell then works with lenders to develop a detailed restructuring plan within set timeframes for approval by the Empowered Group. The goal of CDR is to provide a timely, transparent process to restructure debt outside of legal proceedings for the benefit of all parties involved.