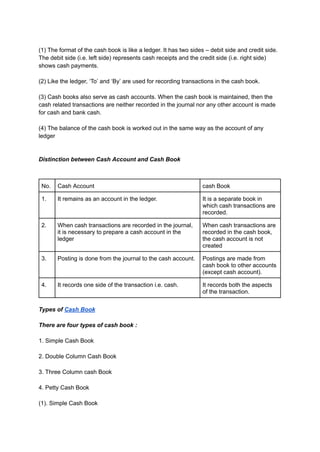

The document discusses the cash book in accountancy for Class 11, highlighting its purpose as a record for all cash receipts and payments, and its dual function as both a journal and a ledger. It details types of cash books, including simple, double column, three column, and petty cash books, along with their features, objectives, and the distinctions between cash accounts and cash books. The text emphasizes the importance of cash books in maintaining accurate financial records and managing cash flow in a business.