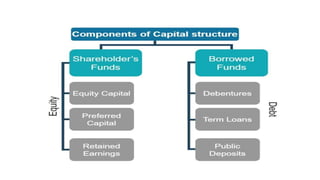

The paper analyzes the determinants of capital structure of listed Indian firms. It uses ten independent variables and the capital structure as the dependent variable. The study finds that factors like profitability, growth, asset tangibility, size, cost of debt, tax rate, and debt serving capacity significantly impact the capital structure chosen by Indian firms. Some key determinants of capital structure discussed are cost of capital, flexibility, market conditions, inflation, firm size and nature, investor requirements, cash flow, flotation costs, and risk. The conclusion is that the capital structure decision is crucial and depends on various firm-specific and market factors.