Downloaded 19 times

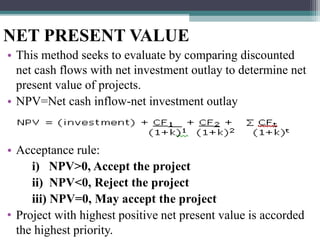

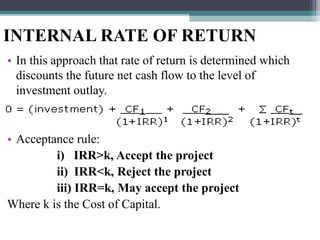

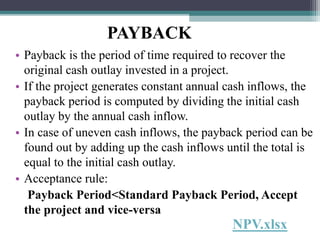

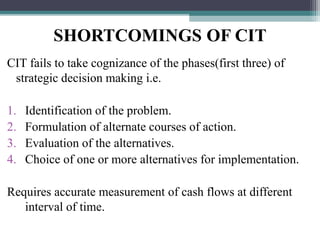

This document discusses capital investment theory (CIT), which is a method for evaluating investment proposals based on their costs and benefits. It describes three stages of CIT: determining net investment outlay, determining net cash flows, and evaluating cash flows based on time value. Major CIT techniques include net present value (NPV), internal rate of return (IRR), and payback period. NPV compares discounted cash flows to investment outlay, with projects having the highest positive NPV prioritized. IRR determines the discount rate that makes the net present value equal to zero. Payback period is the time needed to recover the initial cash outlay. The document also notes some limitations of CIT.

![5) capital_budgeting_(1)_-(2)[1].ppt.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/5capitalbudgeting121-250323135834-146732f6-thumbnail.jpg?width=640&height=640&fit=bounds)