Non performing asset

•

14 likes•2,970 views

A powerful presentation on non performing assets which very much influencial when presented before others. Being a law student, I myself created the presentation and presented before the elite authorities which impressed them to a larger extent.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Non performing asset

Similar to Non performing asset (20)

Recently uploaded

Recently uploaded (20)

Non performing asset

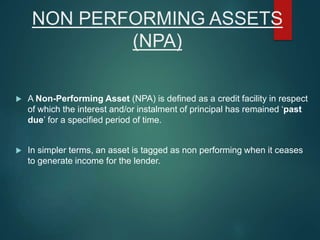

- 1. NON PERFORMING ASSETS (NPA) A Non-Performing Asset (NPA) is defined as a credit facility in respect of which the interest and/or instalment of principal has remained ‘past due’ for a specified period of time. In simpler terms, an asset is tagged as non performing when it ceases to generate income for the lender.

- 2. How can a asset be declared as an NPA ? A Non-Performing Asset (NPA) is defined as a credit facility in which the interest and/or instalment of Bond finance principal has remained ‘past due’ for a specified period of time. Once the borrower has failed to make interest or principle payments for 90 days the loan is considered to be a non-performing asset. The authorities decided to adopt the ‘90 days’ overdue’ norm for identification of NPA, from the year ending March 31, 2004. Accordingly, with effect from March 31, 2004, a non-performing asset (NPA)is a loan or an advance where;

- 3. Interest and/or installment of principal remain overdue for a period of more than 91 days in respect of a term loan, The account remains ‘out of order’ for a period of more than 90 days, in respect of an Overdraft/Cash Credit (OD/CC), Any amount to be received remains overdue for a period of more than 90 days in respect of other accounts, Non submission of Stock Statements for 3 Continuous Quarters in case of Cash Credit Facility, No active transactions in the account (Cash Credit/Over Draft/EPC/PCFC) for more than 91days.

- 4. Provisioning norms for NPA 3 Major types of NPA : Substandard Assets : The account holder comes in this category when they do not pay three installments continue for 90 days and upto 1 year. For this category, bank has made 10% provision of funds out of their profit to meet the losses generated from NPA.

- 5. Doubtful NPA : Under doubtful NPA, three sub – categories falls as under : 1. D1 : i.e. up to 1 year : 20% provision is made by the banks, 2. D2 : i.e. 1 to 3 year : 30% provision is made by the banks and, 3. D3 : i.e. More than 3 year : 100% provision is made by the banks. Loss Assets : under this, 100% provision is made. When account holder comes in this category their account can be written off by the banks. After this the assets are handed over to recovery agents for sale.

- 7. What do you think are the reasons behind NPA ? Lack of proper pre-enquiry by the bank for sanctioning a loan to a customer. Non performance of the business or the purpose for which the customer has taken the loan. Loans sanctioned for agriculture purposes. Willful defaults, fraud, disputes, misappropriation of funds etc. Inability of the corporate to raise capital through the issue of equity or other debt instrument from capital markets.

- 8. Diversion of funds for expansion/modernization/setting up new projects. Other due and beyond control reason such as, shortage of raw material, raw materialinput price escalation, power shortage, industrial recession, excess capacity, natural calamities like floods, accidents etc. Improper SWOT Analysis and poor appraisal system by the financial institutions contributes a huge in the NPA.

- 9. Types of NPA Gross NPA : Gross NPAs are the sum total of all loan assets that are classified as NPAs as per RBI guidelines as on Balance Sheet date. Gross NPA reflects the quality of the loans made by banks. It consists of all the non standard assets like as sub-standard, doubtful, and loss assets.

- 10. Net NPA : Net NPAs are those type of NPAs in which the bank has deducted the provision regarding NPAs. Net NPA shows the actual burden of banks. Net NPA = Gross NPA – Provision for BDDR

- 11. How Gradually The NPA Rise

- 14. Legal measure for the problem of NPA The problems of NPA have been receiving greater attention since 1991 in India. The Narasimham Committee recommended a number of steps to reduce NPA. Major steps taken to solve the problems of Non-Performing Assets in India :- Debt Recovery Tribunals (DRTs) Debt Recovery Tribunals (DRTs) were established. There are 22 DRTs and 5 Debt Recovery Appellate Tribunals. This is insufficient to solve the problem all over the country (India). Where a bank or financial institution has to recover any debt from any person, it makes an application called Original Application (OA) to the Tribunal against such person.

- 15. The provisions of the Recovery of Debts Due to Banks and Financial Institutions Act, 1993 shall not apply where the amount of debt due to bank or financial institution or to a consortium of banks or financial institutions is less than 10 lakhs rupees or such other amount, being not less than 1 lakh rupees, as the Central Government may, by notification, specify. Securitisation Act 2002 This act enables the banks to issue notices to defaulters who have to pay the debts within 60 days. The Securitisation Act further empowers the banks to take over the possession of the assets and management of the company. The lenders can recover the dues by selling the assets or changing the management of the firm. This act applies only to the loans amounted more than 10 lakhs. This act consists a huge number of wide aspects.

- 17. Lok Adalats Lok Adalats have been found suitable for the recovery of small loans. The Honourable Supreme Court also observed that loans, personal loans, credit card loans and housing loans with less than Rs.10 lakhs can be referred to Lok Adalats. According to RBI guidelines issued in 2004-05. They cover NPA up to Rs. 5 lakhs, both suit filed and non- suit filed are covered. Lok Adalats avoid the legal process. Compromise Settlement Compromise Settlement Scheme provides a simple mechanism for recovery of NPA. Compromise Settlement Scheme is applied to advances below Rs. 10 Crores. It covers suit filed cases and cases pending with courts and DRTs (Debt Recovery Tribunals). Cases of Willful default and fraud were excluded.

- 18. Credit Information Bureau A good information system is required to prevent loans from turning into a NPA. If a borrower is a defaulter to one bank, this information should be available to all banks so that they may avoid lending to him. A Credit Information Bureau can help by maintaining a data bank which can be assessed by all lending institutions. As per the Supreme Court (SC) – ”Liquidity of finances and flow of money is essential for any healthy and growth oriented economy. But certainly, what must be kept in mind is that the law should not be in derogation of the rights which are guaranteed to the people under the Constitution. The procedure should also be fair, reasonable and valid, though it may vary looking to the different situations needed to be tackled and object sought to be achieved.”

- 20. WHY IT MATTERS? Here is the impact of the NPAs: it will bring a scarcity of funds in the Indian security markets. Few banks will be willing to lend if they are not sure of the recovery of their money. The shareholders of the banks will lose a lot of money as banks themselves will find it tough to survive in the market. The price of loans, i.e. the interest rates will shoot up badly. Shooting of interest rates will directly impact the investors who wish to take loans for setting up infrastructural, industrial projects etc.

- 21. All of this will lead to a situation of low off take of funds from the security market. This will hurt the overall demand in the Indian economy. And, finally it will lead to lower growth rates and of course higher inflation because of the higher cost of capital. This trend may continue in a vicious circle and deepen the crisis. Total NPAs have touched figures close to the size of UP budget. Imagine if all the NPA was recovered, how well it can augur for the Indian economy.

- 25. DEBT RECOVERY MANAGEMENT IN BANKS A company or agency that is in the business of recovering money that is owed on delinquent accounts. Many debt collectors are hired by companies/Banks to which money is owed by debtors, operating for a fee or for a percentage of the total amount collected. Some debt collectors are debt buyers; these companies purchase debt at a fraction of its face value and then attempt to recover the full amount of the debt. The Bank may utilize the services of recovery agencies for collection of dues and repossession of securities. Recovery agencies will be appointed as per regulatory guidelines issued in this regard.

- 26. The name and address of all Recovery Agencies on the Bank’s approved panel will be placed on the Bank’s website for information. Only recovery agencies from the approved panels will be engaged by the Bank. Employees of the recovery agencies, after completing the mandatory Debt Recovery Agent (DRA) training, will be issued valid ID cards authorising them to collect dues from the Bank's customers. In case the Bank engages service of such recovery/enforcement/ seizure agencies for any recovery case, the identity of the agency will be disclosed to the borrower. The recovery agents engaged by the Bank will be required to follow a code of conduct governing their dealings with customers Examples: •ARCIL (India’s first and largest asset reconstruction company (ARC)) • Reliance Asset Reconstruction Company Limited

- 28. Debt Recovery Procedure by The Agents Contact with a friendly payment reminder Contact with an overdue payment reminder Contact your customer with a final notice Send a formal letter of demand Repossession of Security Valuation & Sale of Property

- 29. Recent Facts and Figures on NPA

- 30. Gross NPAs OF Public and Private Sector Banks During June 30, 2016 Source:RBI;ParliamentQuestions.

- 31. As of June 2016, the total amount of Gross Non-Performing Assets (NPAs) for public and private sector banks is around Rs. 6 lakh crore. The amount of top twenty NPA accounts of Public Sector Banks stands at Rs. 1.54 lakh crore. The ratio of NPAs to total advances given by a bank is a commonly used indicator reflecting the health of the banking system. According to the latest information collated by the government, stressed assets which includes both non-performing assets as well as restructured loans of banks stood at Rs 9.64 lakh crore as on December 31, 2016. Since its inception, ARCIL has resolved over Rs.780 billion worth of Non- Performing Assets (NPAs) acquired from Indian banks and Financial Institutions.

- 32. The SARFAESI Act allows banks and other financial institutions to auction residential and commercial properties when borrowers default on their payments. This helps the banks to reduce their NPA by recovery and reconstruction. Under this Act, 64,519 properties were seized or taken possession off by the banks in 2015-16. In the current financial year, as of June, the number stands at 33,928. In absolute terms, State Bank of India has the highest value of Gross NPA around Rs. 93,000 crores. Punjab National Bank (Rs. 55,000 crores) and Bank of India (Rs. 44,000 crores) comes next. Basic Metal and Metal Products sector is the worst performing in terms of NPA ratio. As of June 2016, govt data show that a third of all outstanding advances (Rs. 4.33 lakh crore) given to the sector turned to NPA (Rs. 1.49 lakh crore).

- 33. Despite the Reserve Bank of India (RBI) announcing numerous restructuring schemes, the bad loans have risen up from Rs 261,843 crore by 135 per cent in last two years. RBI has came up with a notification titled “Revised Prompt Corrective Action (PCA) framework for banks.” The revised framework would apply to all banks operating in India including small and foreign banks. The new set of provisions had been came into effect from April 1 based on the financials of banks as of March 2017. The revised framework will override the existing PCA framework. The revised framework will be again reviewed after three years.

- 34. THANK YOU ! info@lawsolindia.com +91-9860312403 www.lawsolindia.com

Editor's Notes

- YGYGUYGUYG