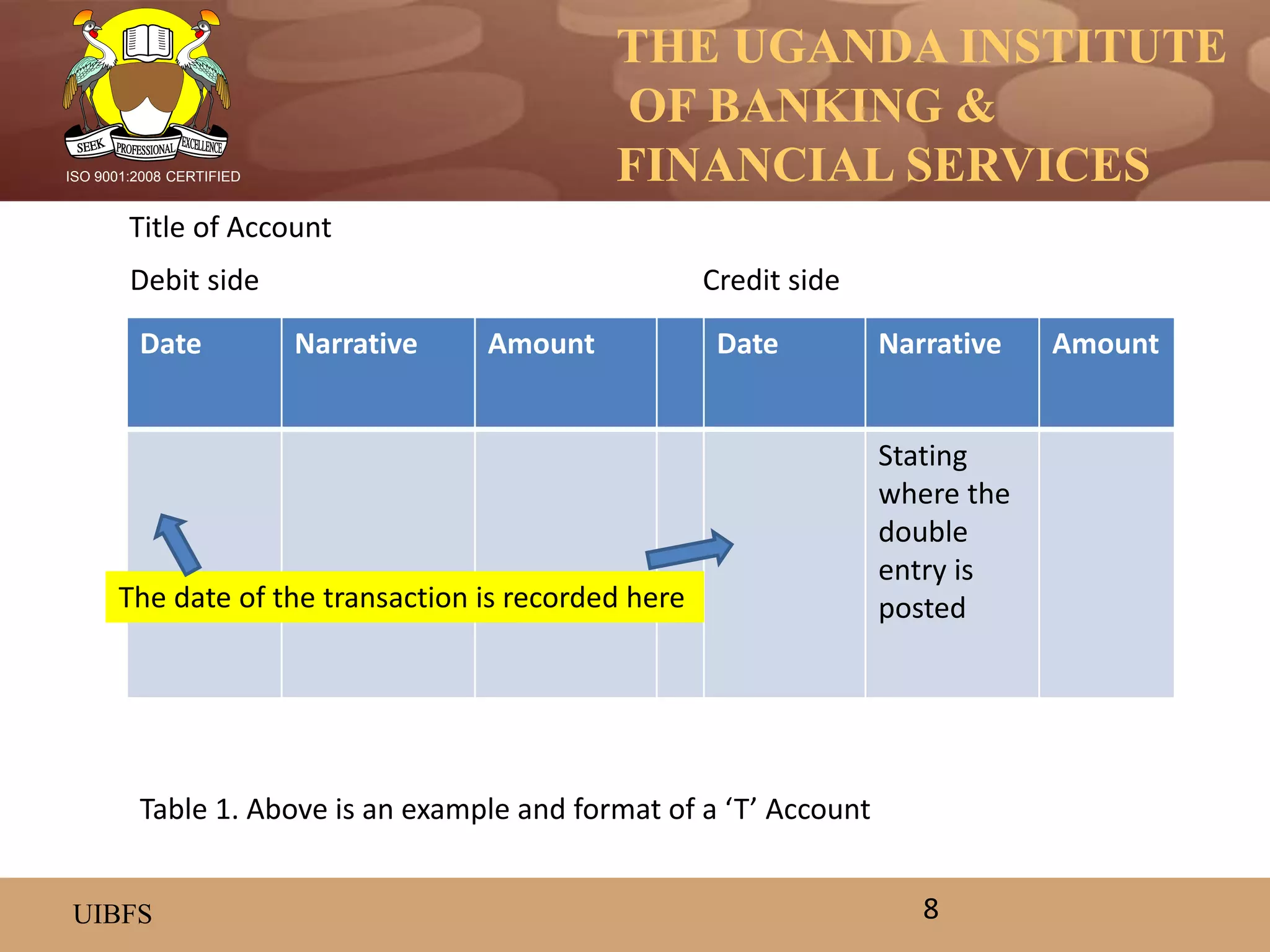

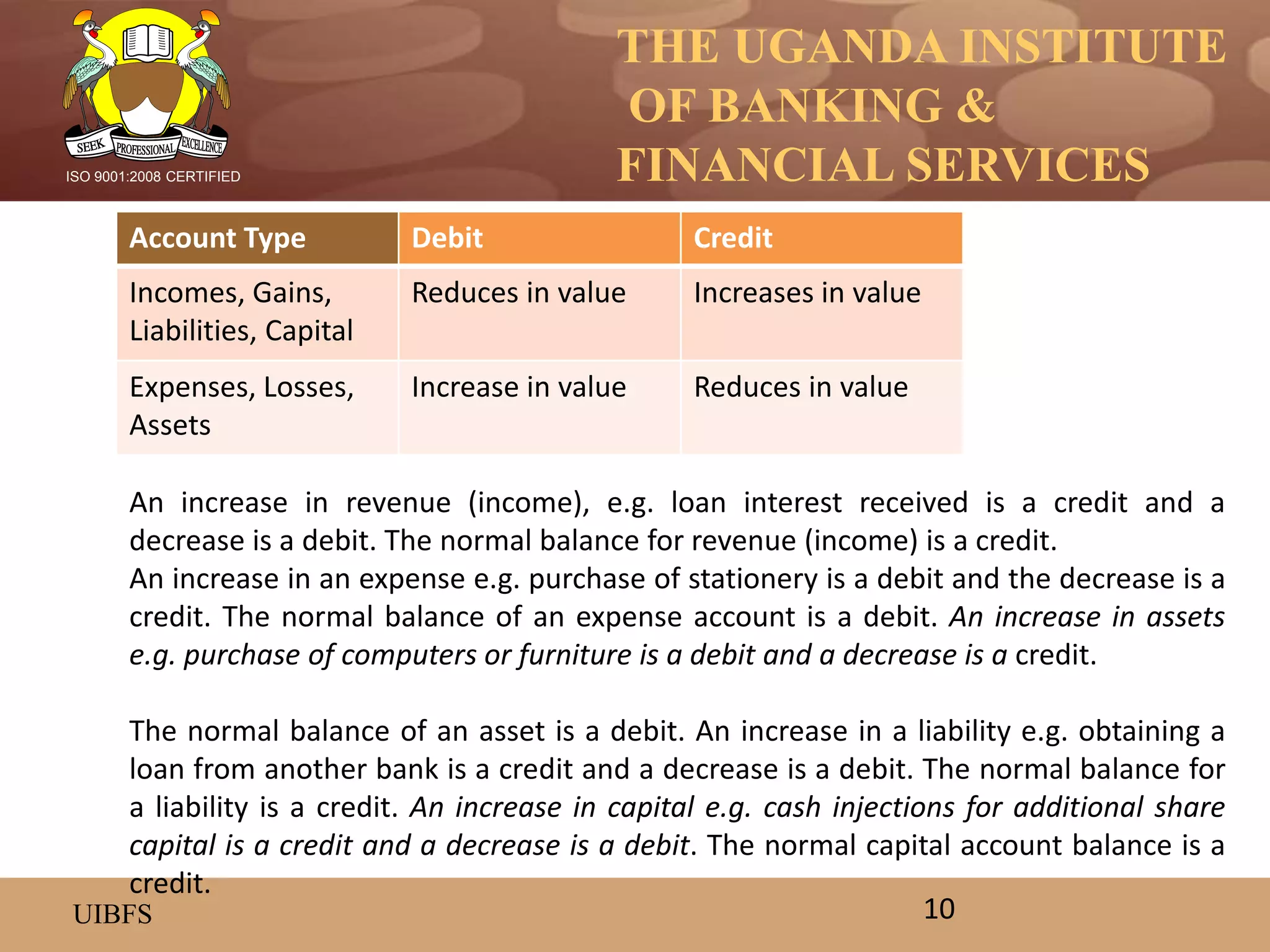

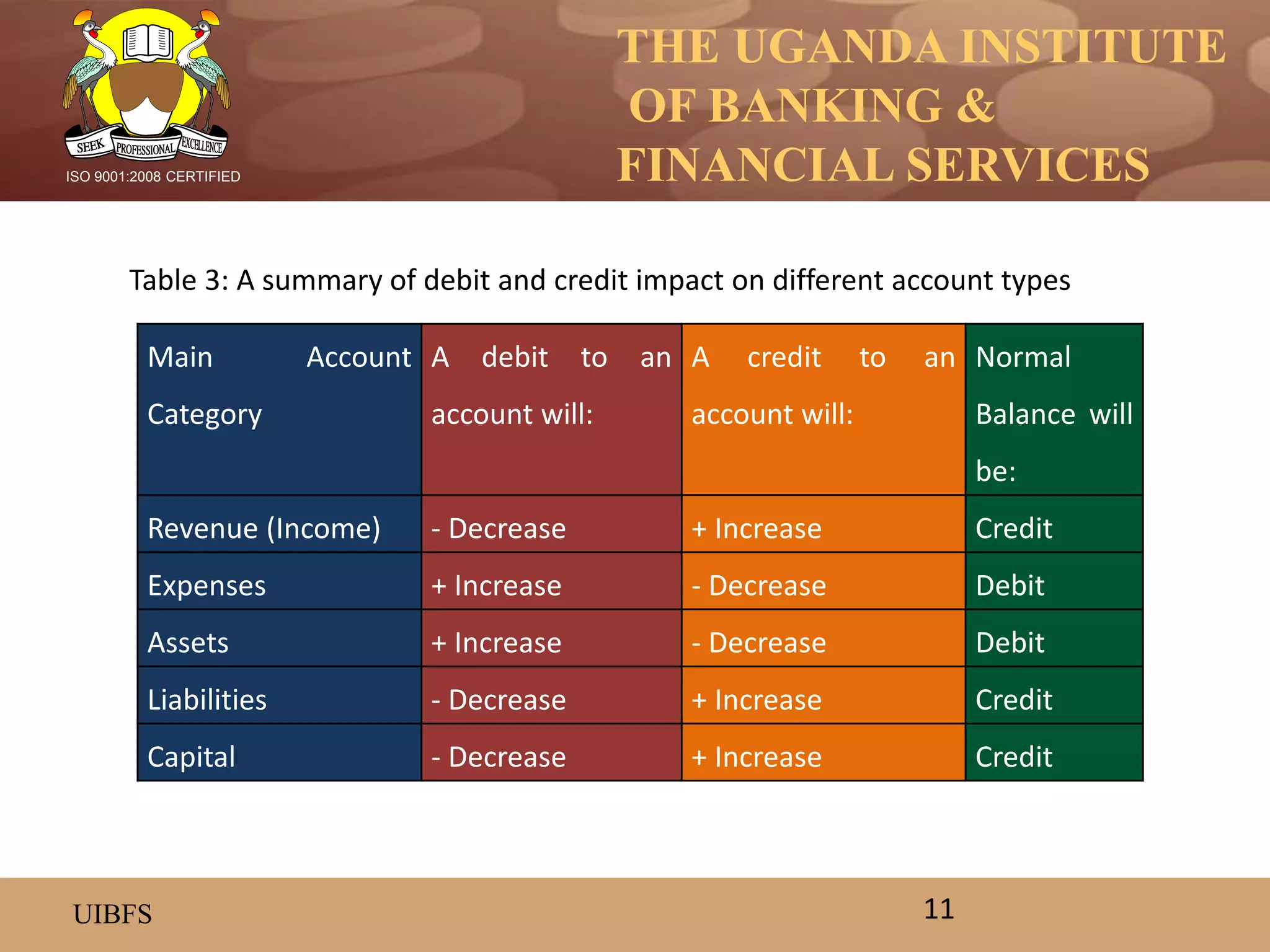

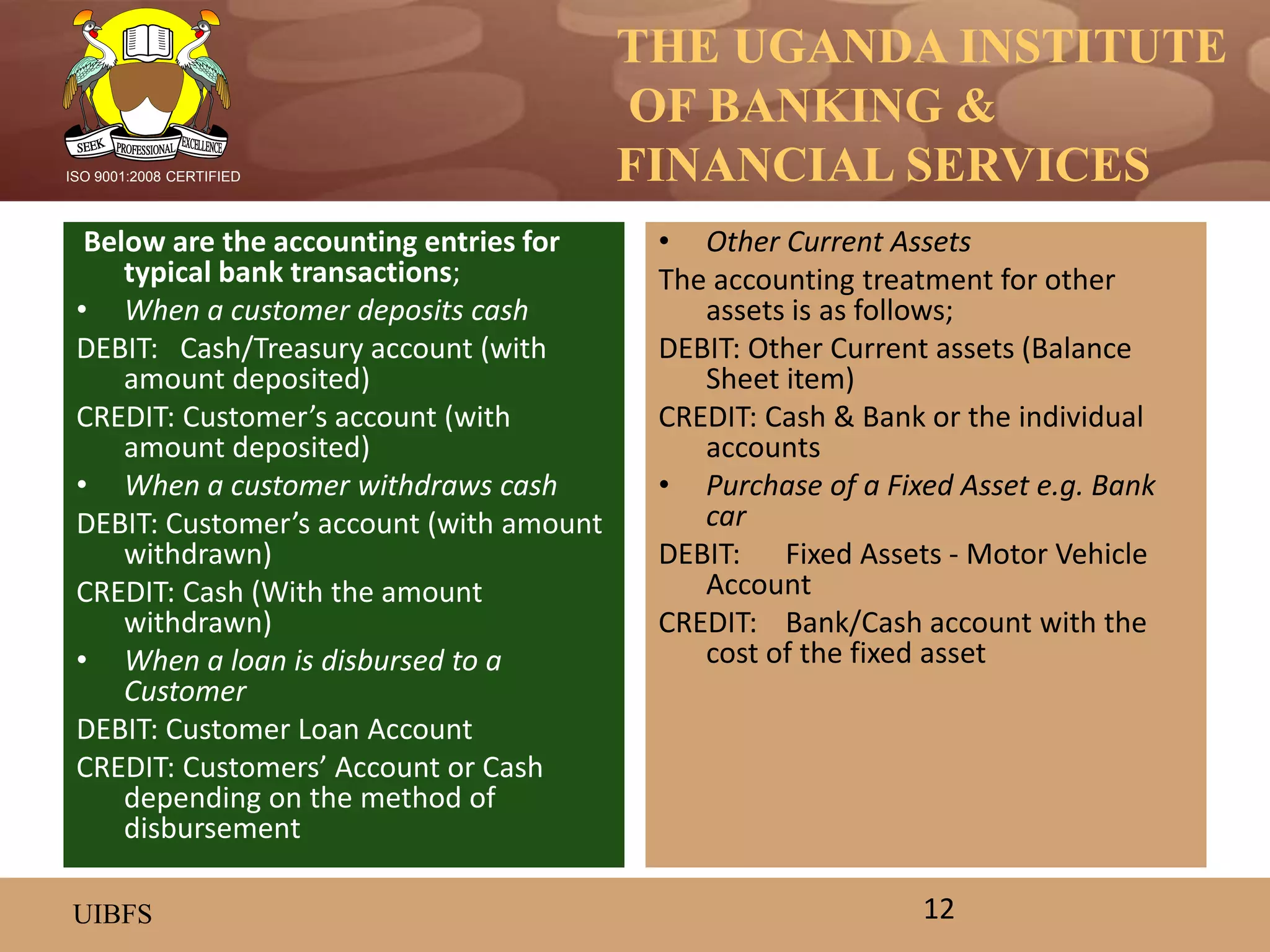

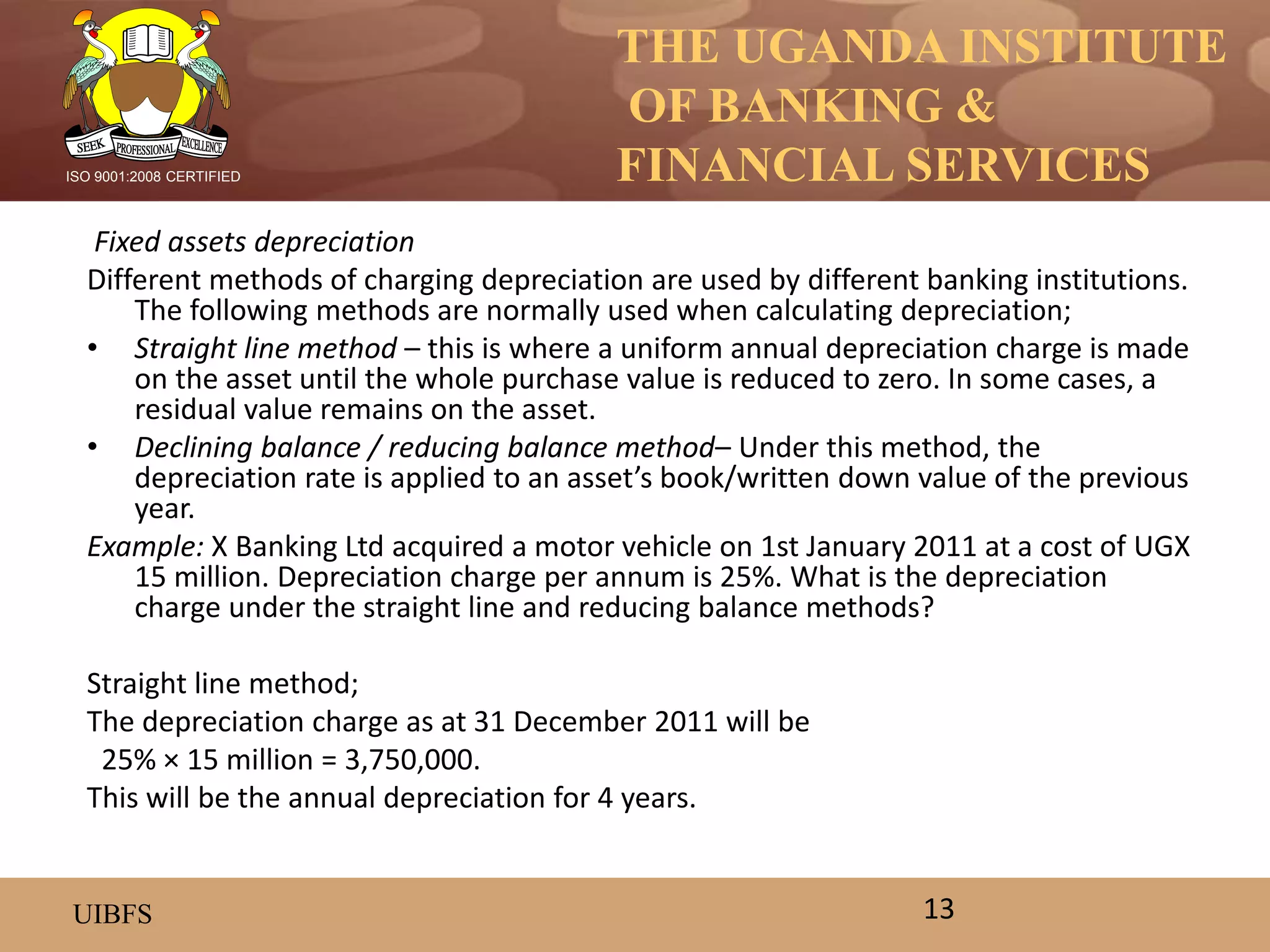

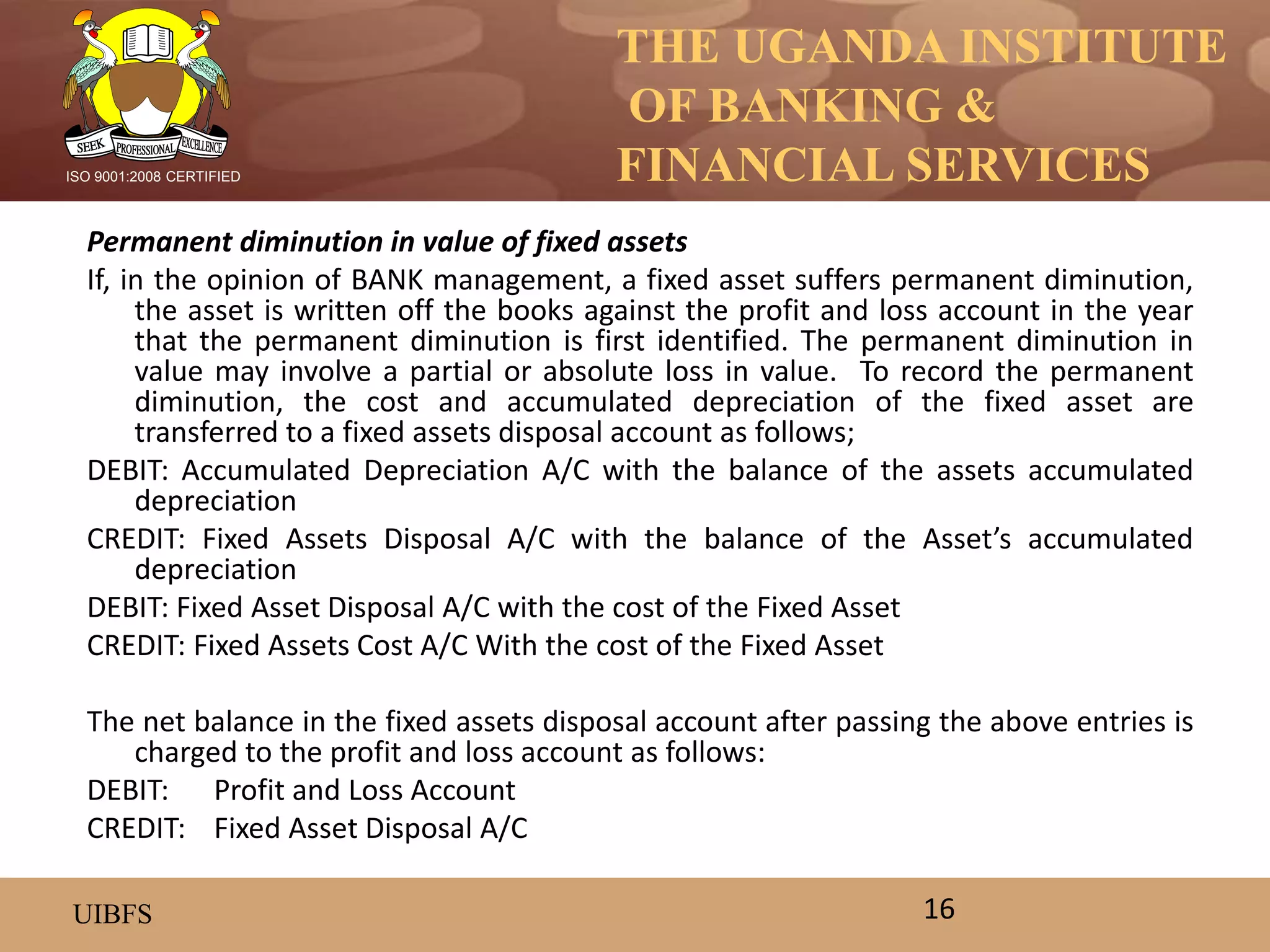

This document provides an overview of the eight key steps in the accounting cycle for processing transactions: 1) Identifying transactions, 2) Classifying transactions, 3) Journalizing transactions, 4) Posting to ledgers, 5) Making adjusting entries, 6) Making closing entries, 7) Preparing a trial balance, and 8) Presenting final financial statements. It describes each step in the process, highlighting concepts like double-entry bookkeeping, debit and credit rules for different types of accounts, and examples of accounting entries for common bank transactions.

![THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

• Reducing-balance method;

Value of Motor vehicle as at 1 January 2011 15,000,000

Less: Depreciation charge for first year (25%) 3,750,000

Book value as at 31 December 2011 11,250,000

Depreciation charge as at 31 December 2012 2,812,500 [25% x11,250,000]

To record depreciation expenses, the following entries are made;

DEBIT: Depreciation expense

CREDIT: Accumulated depreciation

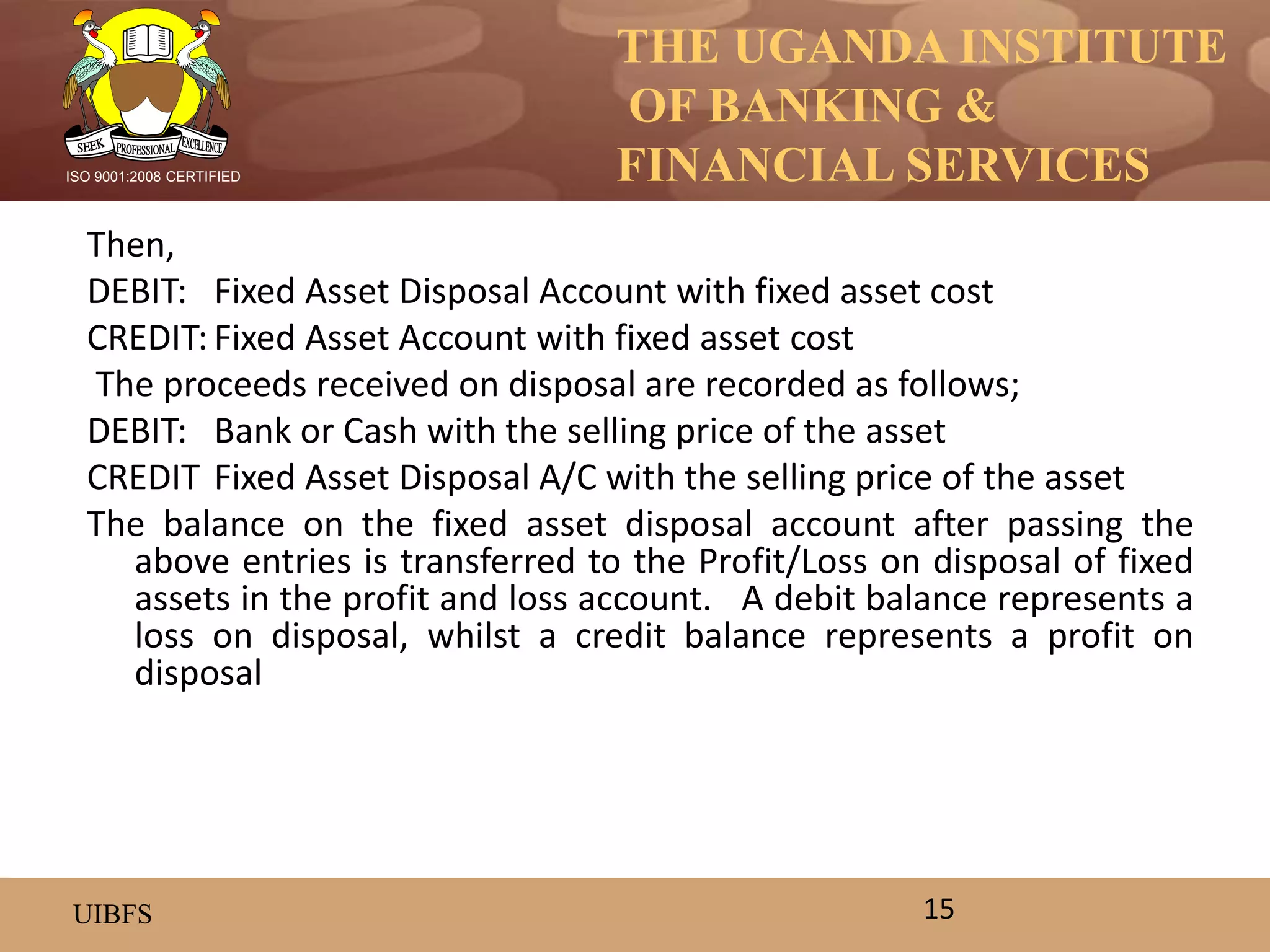

• Disposal of fixed assets

To record the sale or disposal of a fixed asset, the cost and accumulated depreciation

of the fixed asset are transferred to a Fixed Assets Disposal Account as follows:

DEBIT: Accumulated Depreciation with the balance on the Accumulated Depreciation

Account

CREDIT: Fixed asset disposal with the balance on the Accumulated Depreciation

Account

14](https://image.slidesharecdn.com/basicaccountingunit2-150428050135-conversion-gate01/75/Basic-accounting-unit2-14-2048.jpg)

![THE UGANDA INSTITUTE

OF BANKING &

FINANCIAL SERVICES

UIBFS

ISO 9001:2008 CERTIFIED

Example:

Suppose a bank acquires a vehicle on 1/1/2007 for UGX 15 million and depreciates it

over 4 years on a straight-line basis, with nil salvage value. On 1 January 2010 a

firm of professional valuers appointed by the bank re-values the asset at UGX 8

million. Bank management decides to recognize the revaluation in the accounting

records. At the time of the revaluation (1/1/2010), the net book value of the

vehicle was as follows;

UGX Cost: (1.1.2007) 15,000,000

Less: Accumulated depreciation 11,250,000 [3* 25%*UGX 15 million]

Net book value (31.12.2009) 3,750,000

The new valuation of the vehicle is UGX 8 million; therefore the revaluation surplus is

UGX 4,250,000 (8,000,000 – 3,750,000). The revaluation surplus would be

credited to the Revaluation Reserve Account and debited to the Motor Vehicle

Account.

The vehicle would still be depreciated over 4 years (until 31/12/2010). Any

additional depreciation (based on the revalued amount), would be reduced by an

equivalent transfer from the revaluation surplus account.

18](https://image.slidesharecdn.com/basicaccountingunit2-150428050135-conversion-gate01/75/Basic-accounting-unit2-18-2048.jpg)