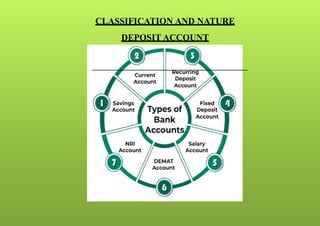

The document discusses the various relationships between bankers and customers, primarily categorizing them as creditor-debtor, trustee-beneficiary, and agent-principal, among others. It highlights the special relationships involving different types of customers, such as minors, married women, and institutions, detailing the unique considerations needed for each. Additionally, it outlines different types of deposit accounts, including savings, current, and fixed deposit accounts, specifying their features, limitations, and the process for opening such accounts.