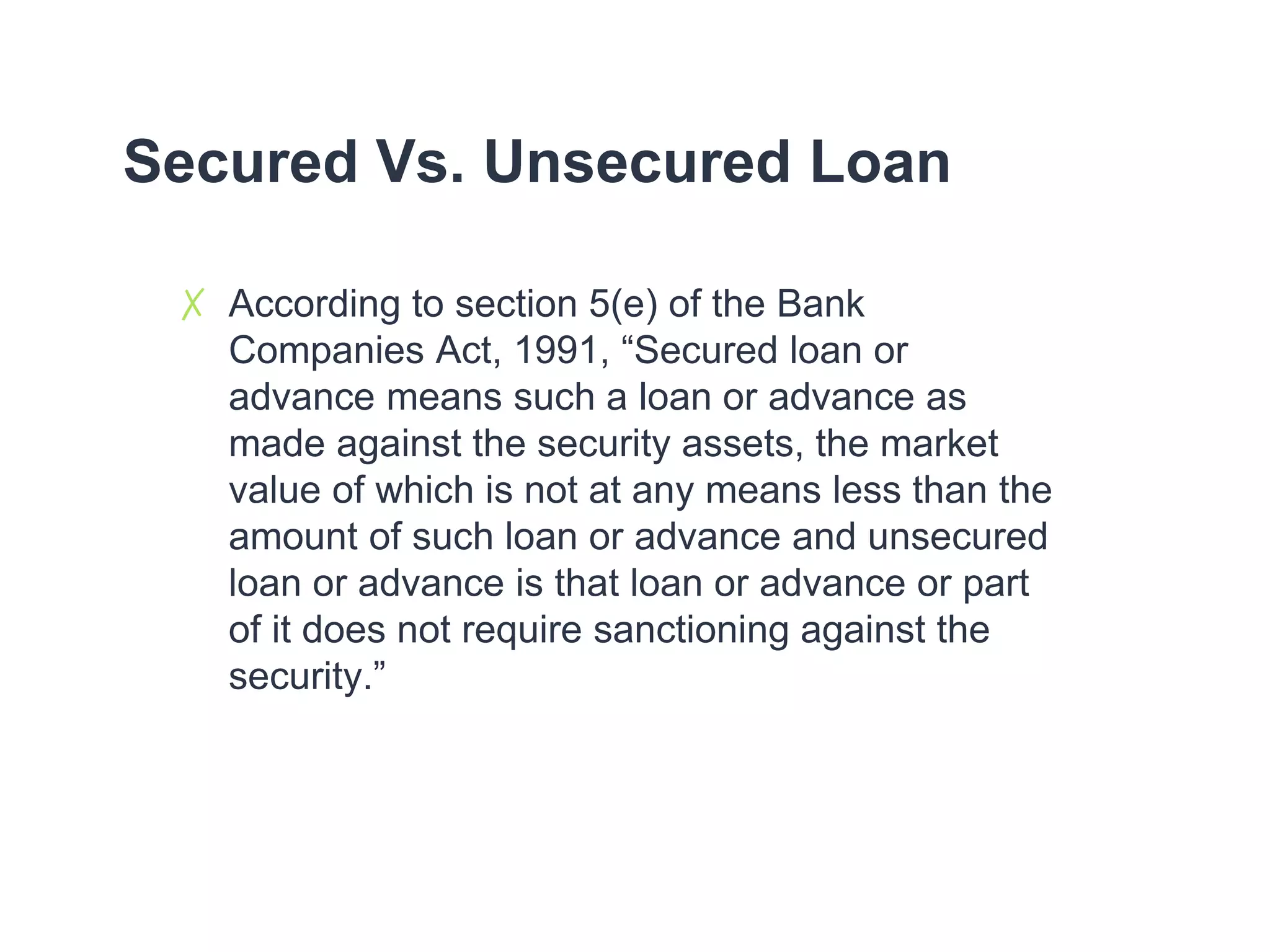

This document discusses various forms of advances in banking, including cash credits, overdrafts, loans, secured vs. unsecured loans, participation loans, and purchasing and discounting bills. It provides details on each type of advance, such as how cash credits and overdrafts work, the differences between demand loans and term loans, what constitutes a secured vs. unsecured loan, how participation or consortium loans are loans granted by multiple financing agencies, and how banks provide advances through discounting or purchasing bills of exchange.