SRM INSTITUTE OFSCIENCE AND TECHNOLOGY

RAMAPURAM- CHENNAI-89.

STAFF NAME: Dr.S.Mani

COURSE & SECTION: B.Com General – “F” & “K”

COURSE NAME: CORPORATE ACCOUNTING -1I

COURSE CODE: UCM23401J

UNIT – III

2.

ACCOUNTS OF HOLDINGCOMPANY

Meaning of holding company:

A holding company is a company which holds the shares of another

company while the first is called holding company, the company which is so

controlled in termed as ‘subsidiary company’. The main advantage of getting a

control over another company is elimination of competition to enjoy economics

of large scale production and to get a assured market for the production of the

company.

Sec. 4 of the Indian Companies Act, 1956 provides that a holding company is

one of it:

Control the board of directors of another company; or Holds more than half of

the nominal value of equity share capital of another company; or Controls a

holding company which in turn controls another subsidiary company. In practice,

acquisition of 50% or more shares in another company makes a company as a

holding company.

3.

What do youmean by subsidiary company?

Meaning of Subsidiary company:

From Sec.4 it is clear that a company is a subsidiary of a holding

company in any of the following three cases:

When the holding company controls the compositions of the board of

directors of the subsidiary company i.e., the holding company is able to

appoint or dismiss the majority of directors of the subsidiary company.

Where the holding company holds more than 50% in nominal value of

the equity share capital of the subsidiary company i.e., the holding

company holds the majority of voting power in the subsidiary company.

When a subsidiary company is a holding company of another subsidiary

company the original holding company is also a holding company of that

other subsidiary company.

4.

Minority interest

The holdingcompany usually acquires the majority of

the shares of the subsidiary company. The remaining

portion as acquired by the outsiders. The outsides are

collectively called minority shareholders. While

preparing the consolidated balance sheet, the interest of

minority shareholders should be shown in the balance

sheet on the liabilities side under the heading ‘minority

interest’.

5.

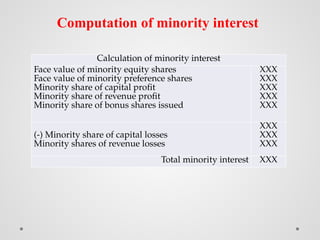

Computation of minorityinterest

Calculation of minority interest

Face value of minority equity shares

Face value of minority preference shares

Minority share of capital profit

Minority share of revenue profit

Minority share of bonus shares issued

XXX

XXX

XXX

XXX

XXX

(-) Minority share of capital losses

Minority shares of revenue losses

XXX

XXX

XXX

Total minority interest XXX

6.

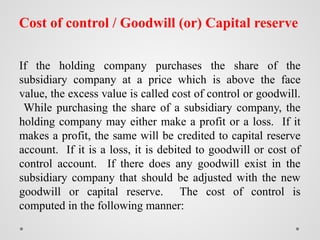

Cost of control/ Goodwill (or) Capital reserve

If the holding company purchases the share of the

subsidiary company at a price which is above the face

value, the excess value is called cost of control or goodwill.

While purchasing the share of a subsidiary company, the

holding company may either make a profit or a loss. If it

makes a profit, the same will be credited to capital reserve

account. If it is a loss, it is debited to goodwill or cost of

control account. If there does any goodwill exist in the

subsidiary company that should be adjusted with the new

goodwill or capital reserve. The cost of control is

computed in the following manner:

7.

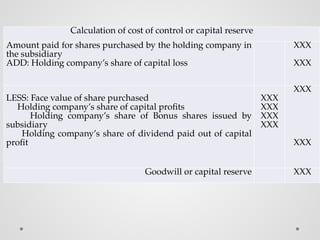

Calculation of costof control or capital reserve

Amount paid for shares purchased by the holding company in

the subsidiary

ADD: Holding company’s share of capital loss

XXX

XXX

LESS: Face value of share purchased

Holding company’s share of capital profits

Holding company’s share of Bonus shares issued by

subsidiary

Holding company’s share of dividend paid out of capital

profit

XXX

XXX

XXX

XXX

XXX

XXX

Goodwill or capital reserve XXX

8.

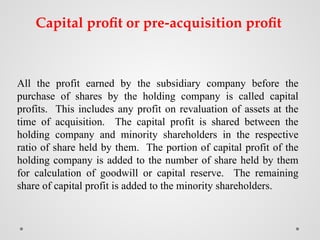

All the profitearned by the subsidiary company before the

purchase of shares by the holding company is called capital

profits. This includes any profit on revaluation of assets at the

time of acquisition. The capital profit is shared between the

holding company and minority shareholders in the respective

ratio of share held by them. The portion of capital profit of the

holding company is added to the number of share held by them

for calculation of goodwill or capital reserve. The remaining

share of capital profit is added to the minority shareholders.

Capital profit or pre-acquisition profit

9.

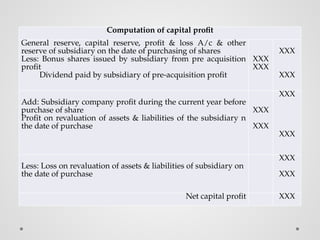

Computation of capitalprofit

General reserve, capital reserve, profit & loss A/c & other

reserve of subsidiary on the date of purchasing of shares

Less: Bonus shares issued by subsidiary from pre acquisition

profit

Dividend paid by subsidiary of pre-acquisition profit

XXX

XXX

XXX

XXX

Add: Subsidiary company profit during the current year before

purchase of share

Profit on revaluation of assets & liabilities of the subsidiary n

the date of purchase

XXX

XXX

XXX

XXX

Less: Loss on revaluation of assets & liabilities of subsidiary on

the date of purchase

XXX

XXX

Net capital profit XXX

10.

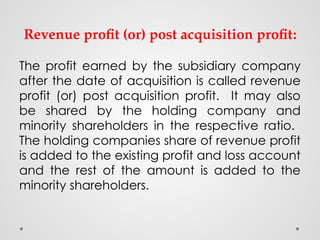

Revenue profit (or)post acquisition profit:

The profit earned by the subsidiary company

after the date of acquisition is called revenue

profit (or) post acquisition profit. It may also

be shared by the holding company and

minority shareholders in the respective ratio.

The holding companies share of revenue profit

is added to the existing profit and loss account

and the rest of the amount is added to the

minority shareholders.

11.

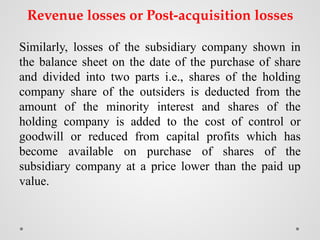

Revenue losses orPost-acquisition losses

Similarly, losses of the subsidiary company shown in

the balance sheet on the date of the purchase of share

and divided into two parts i.e., shares of the holding

company share of the outsiders is deducted from the

amount of the minority interest and shares of the

holding company is added to the cost of control or

goodwill or reduced from capital profits which has

become available on purchase of shares of the

subsidiary company at a price lower than the paid up

value.

12.

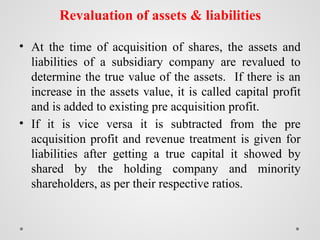

Revaluation of assets& liabilities

• At the time of acquisition of shares, the assets and

liabilities of a subsidiary company are revalued to

determine the true value of the assets. If there is an

increase in the assets value, it is called capital profit

and is added to existing pre acquisition profit.

• If it is vice versa it is subtracted from the pre

acquisition profit and revenue treatment is given for

liabilities after getting a true capital it showed by

shared by the holding company and minority

shareholders, as per their respective ratios.

13.

Bonus shares

Generally bonusshares are issued out of pre acquisition profit or

post acquisition profit. In case of pre acquisition profit, there

will be no effect on the consolidated balance sheet because while

ascertaining the cost of control, the holding companies shares in

the pre acquisition profit are reduced, and the paid up value of

the shares increase. Therefore the goodwill remains the same as

it was before the issue of bonus shares of the company.

In case of post acquisition profits, the issue of bonus share will

have the effect of reducing the holding companies shares in the

revenue profit and increase the paid up value of shares held by

the holding company.

•

14.

Unrealized profit

An unrealizedprofit exists when a companies stock is at

a selling price i.e., at a profit. It is agreed that this

should be treated as an unrealized profit and it should be

eliminated from stock as well as from profit and loss

account. Towards this, a separate reserve called stock

reserve is normally created. It is considered by a

minority that the whole of such unrealized profit should

be eliminated by creating a stock reserve. Others are of

an opinion that shares of profit of the holding company

alone should be eliminated from the balance sheet of

both the sides.

15.

Dividend

When dividend hasbeen declared by the subsidiary company and the

holding company received it, the treatment of dividend will be as

follows:

Dividend received by the holding company from the capital profit of the

subsidiary company are created to invest in share of the subsidiary

account thereby reducing the cost of control or increasing capital

reserve.

If the dividends received out of the revenue profits are treated as income

and credited to profit & loss account by the holding company.

If dividend declared party out of the capital profits and partly out of

revenue profits, the dividend received is dividend into two parts in

proportion to its declaration out of capital profit and revenue profits.

If the dividend has simply been proposed by the subsidiary. The

holding companies share of it is added to its profit and shown as profit

and loss balance. The share due to minority shareholders may be either

shown as proposed dividend in the balance sheet or added to the

minority interest.

16.

POSSIBLE QUESTIONS

1. Whatdo you mean by holding company?

2. What do you mean by subsidiary company?

3. What is minority interest?

4. How would you ascertain the amount of minority interest?

5. What is cost of control (or) Goodwill (or) Capital Reserve?

6. How would you ascertain the amount of goodwill?

7. What do you understand by ‘Capital profit’ (or) Pre-acquisition profit?

8. what do you understand ‘Revenue profit’ (or) Post-acquisition profit.

9. What do you understand by ‘Revenue losses’ or ‘Post-acquisition losses’?

10. What do you mean by revaluation of assets and liabilities?

11. What is a bonus share issued by subsidiary company?

12. What do you mean by unrealized profit and dividends?

13. How they treat in holding company accounts?