Downloaded 80 times

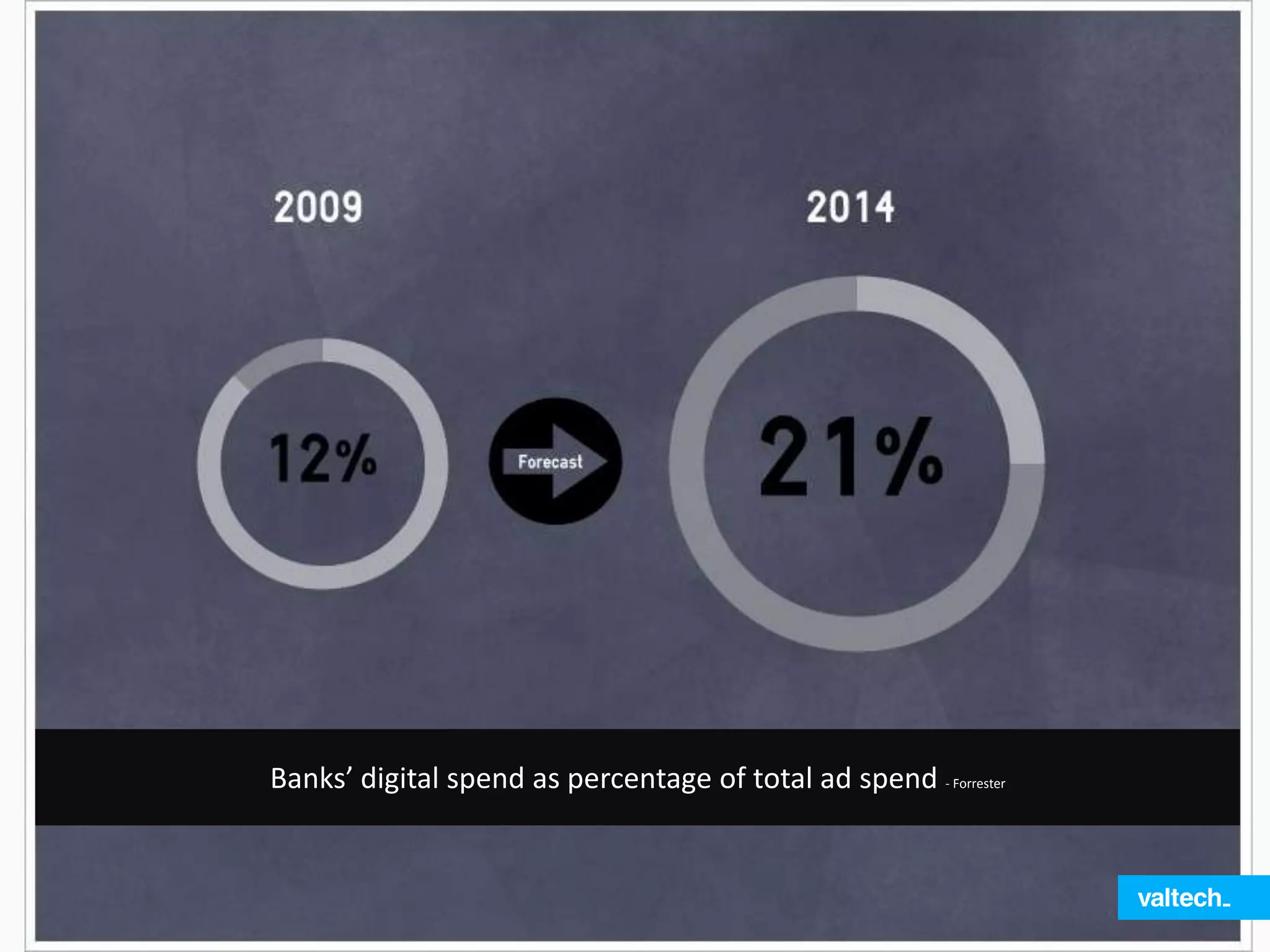

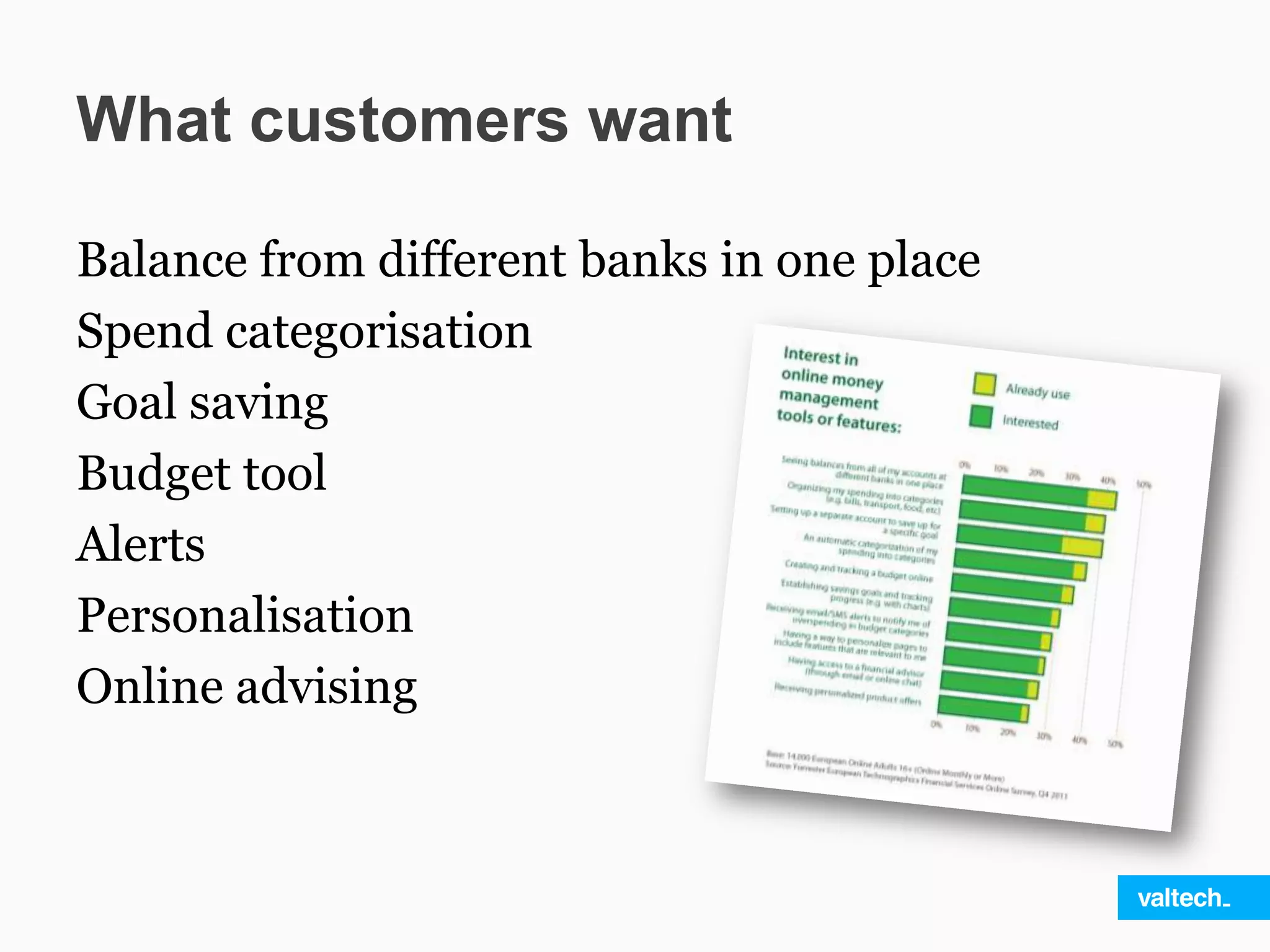

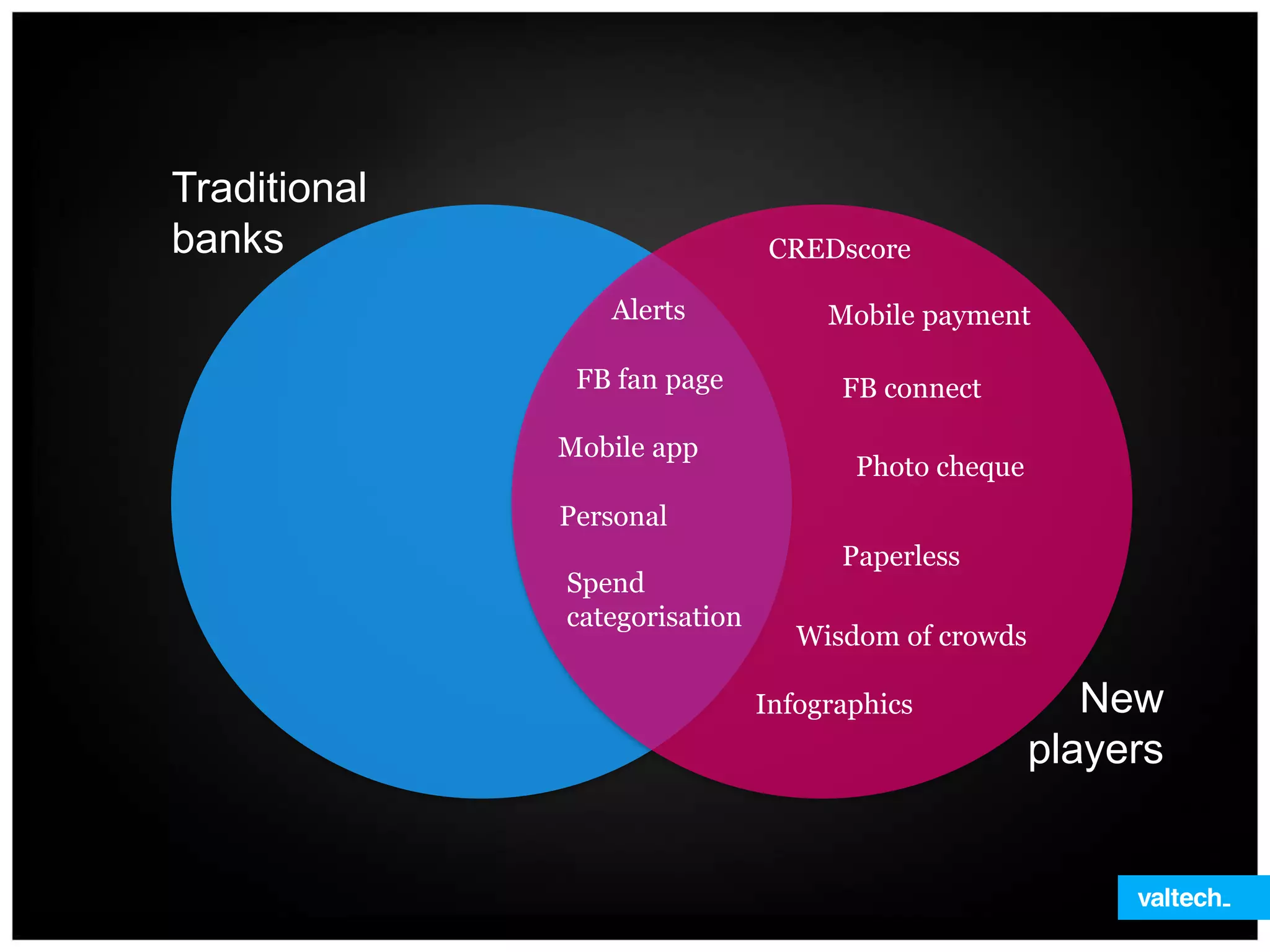

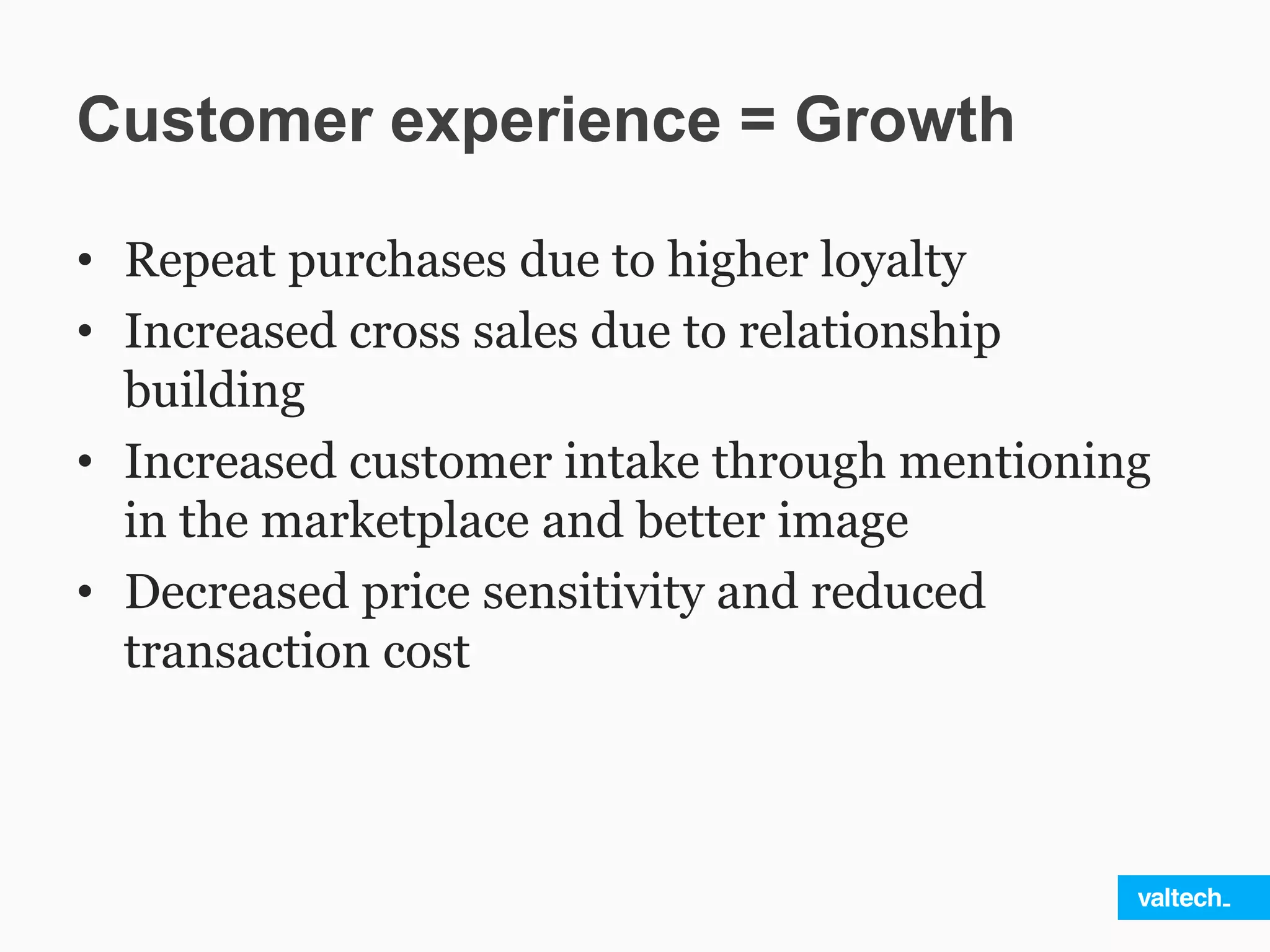

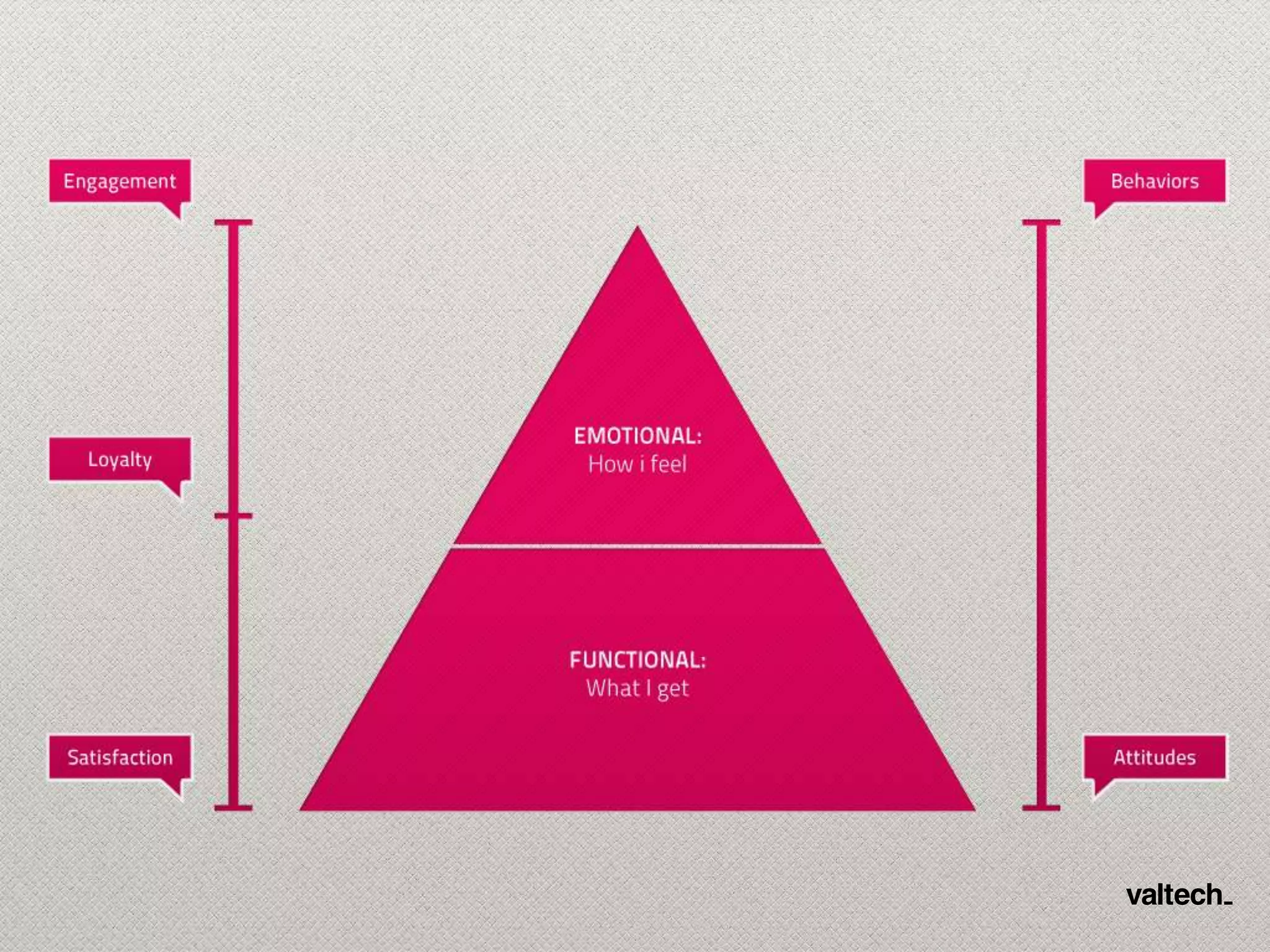

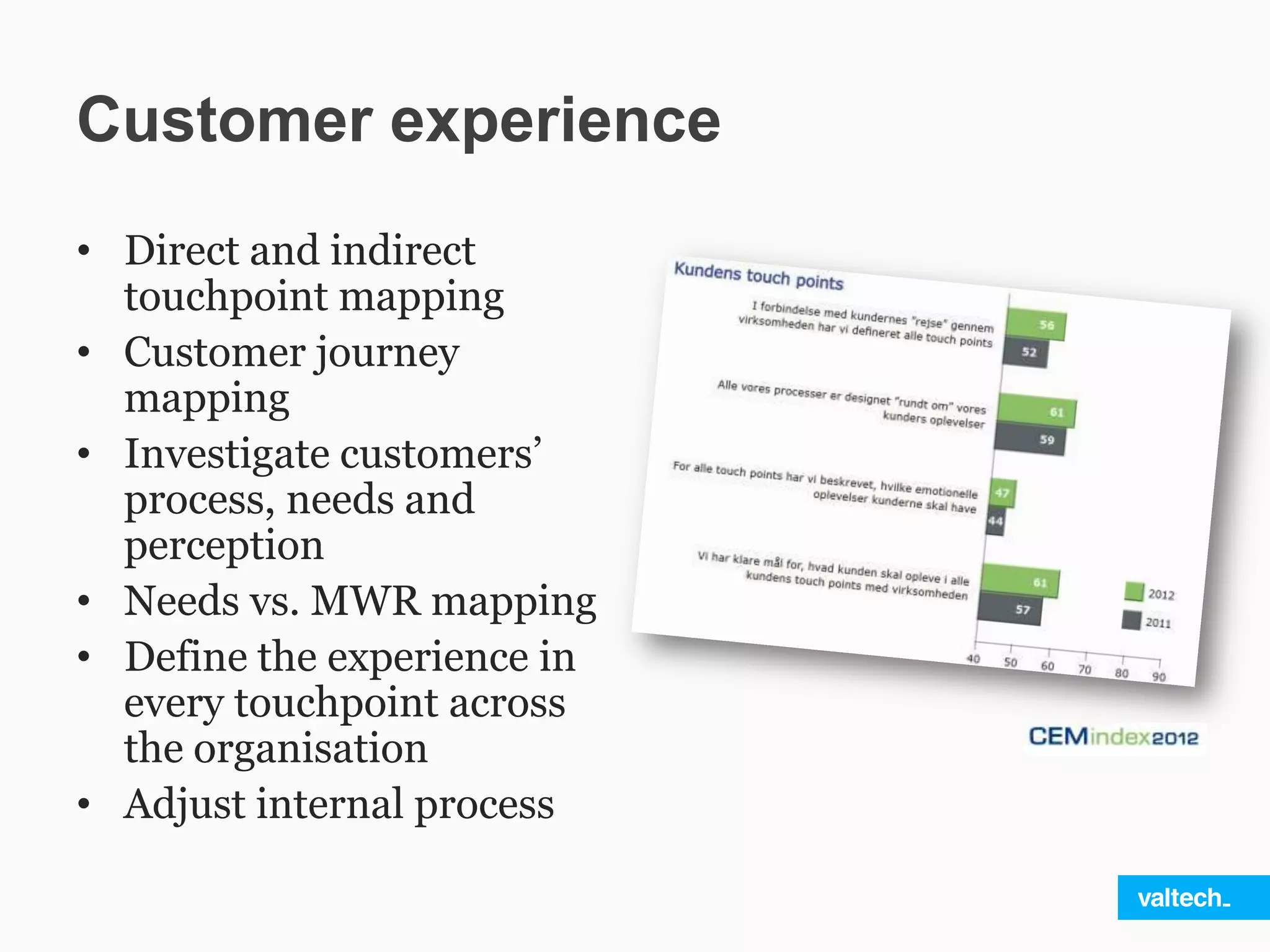

The document discusses the rising trend in banking service innovation, highlighting increased digital spending by banks and customer demands for features like personalization and data-driven tools. It emphasizes the competition from new players and the importance of customer experience as a driver for bank loyalty and growth. Additionally, it suggests a comprehensive approach to mapping and improving customer interactions across all touchpoints to enhance the overall experience.

![[ Overit Webinar ] Grow Your Business: Growth Marketing and Why You Need It](https://cdn.slidesharecdn.com/ss_thumbnails/growthmarketing-220401160802-thumbnail.jpg?width=640&height=640&fit=bounds)