To understand following features:

OPM Inventory conversion.

Material traceability: Enhanced material control

Dual UOM functionality.

Material Status control.

Advanced Lot control.

Lot indivisibility functionality.

Material aging workflow.

To understand following features:

OPM Inventory conversion.

Material traceability: Enhanced material control

Dual UOM functionality.

Material Status control.

Advanced Lot control.

Lot indivisibility functionality.

Material aging workflow.

Each ERP implementation has a set of main objectives, and one of them is to obtain Cost Accounting or Managerial Report for specific line of business.

As SAP, PeopleSoft or JD Edwards have such Cost Accounting module, we developed and offer a specialized module for Oracle Applications.

How to remove disable and cancel shipment functionality in enter purchase or...Ahmed Elshayeb

How To Remove Disable Cancel Shipment Functionality In Enter Purchase Order and Purchase Order Summary Forms

منع المستخدم من إستخدام إمكانية إلغاء شحنة علي أمر توريد تم الإستلام عليها من علي شاشة ملخص أوامر الشراء ومن شاشة إدخال أوامر التوريد

In the dating game of the web, you need more than just a pretty (inter)face and a winning smile. You need to woo your users in a complex ritual of seduction and delight. Only then will you win their hearts, minds and registration details. Sadly, too many sites focus purely on the chase, adding each new conquest into their little black book of registered users (moleskines presumably) before moving on to their next victim.

While one-night log-ins can be exciting, they aren't particularly satisfying. It's the quality rather than quantity of your relationships that count. A truly meaningful relationship takes time, understanding and sacrifice. The best relationships are born from a sense of shared ideals; they are supportive, caring and fun.

Using examples from the real world, this session will look at the various tips, tricks and techniques you can use to make your users fall in love with your product or service. So dim the lights, put Barry White on the stereo and get ready for a lesson in the fine art of user seduction.

Different techniques of costing in strategic management accounting discussed.

Marginal costing,budgetary control, standard costing,Activity based costing,responsibility costing.

In today's manufacturing environment, which makes sense, standard or actual costing?

https://benjaminwann.com/blog

Order the book here:

https://www.amazon.com/dp/B093QF4DD4

Check out my BPI- Business Process course on Udemy!

https://www.udemy.com/course/business-process-improvement-and-process-mapping/?referralCode=9A549649145AD26A9D06

LearningObjectivesAfter studying Chapter 8, you will be a.docxcroysierkathey

LearningObjectives

After studying Chapter 8, you will be able to:

Explain the signi�icance of pro�it analysis for an organization.

Describe the major characteristics and conditions of a standard cost system.

Understand the information contained in a standard cost sheet.

Compute materials price and usage variances, and identify potential causes of such variances.

Compute labor rate and ef�iciency variances, and identify potential causes of such variances.

Explain the major considerations that are the basis of standard costs for overhead and compute

budget variances and capacity variances for overhead.

Explain why the capacity variance is related only to �ixed overhead costs.

Understand issues relating to variance investigation and disposal of variances.

8 Cost Control Through Standard Costs

nd3000/iStock/Thinkstock

Explain how standard costs can be used in various different settings.

Describe ethical considerations relating to standards and variances.

WhereDoIStartWithStandardCosts?

Jean-Claude Recca, President of Rue de Lorraine, a chain of fast-food restaurants in central France, just

returned from a reunion of his INSEAD graduating class. During the day of activities in the Riviera, he talked

with several of his classmates who have become extremely successful in various businesses. One of those

classmates suggested to Jean-Claude that adoption of a standard cost system eliminated most of her �irm’s

unacceptable scrap and spoilage, caused an examination of nonvalue-added activities, and substantially

reduced several inef�icient operations.

Jean-Claude did not know whether his restaurant chain would really bene�it from a standard cost system. He

wondered: If he makes the change, which costs should be put on standards? How does he set up standards?

When do variances mean something? Isn’t a standard cost system expensive to use? Isn’t it a pain in the

derriere? Wouldn’t a tight budget do the same thing?

These questions were more than Jean-Claude could consider. He decided to bounce the idea of standard

costs off his controller.

In measuring success in any undertaking, a comparison is usually made between actual performance and expected

performance. Any difference is a variance. A manager is then left with the responsibility to explain the what, why,

and how of the variance. In doing so, the manager must understand the in�luence of key variables on the actual

results, focus on areas that deserve more detailed investigation, and determine changes that must be made in future

planning and control. This chapter introduces the concept of pro�it analysis and then concentrates on variances

associated with a standard cost system for direct materials, direct labor, and factory overhead.

8.1Pro�itAnalysis

Pro�it is an overall measure of how well an organization is doing. A pro�it variance then is the difference between

the actual net income and the planned net income for the same period. The causes of such a variance are related to

...

Meaning & Definition

Objectives of Cost Accounting

Advantages of Cost Accounting

Difference between Cost Accounting and Financial Accounting

Cost concepts and classifications

Elements of cost

This insightful PowerPoint presentation provides a comprehensive overview of Chapter 10 from the field of Managerial Accounting, focusing on the important concepts of Standard costs and variances.Through visually engaging slides and concise explanations, this presentation covers the fundamental principles of costs and variances demonstrating their significance in assessing organizational performance. Gain insights into the process of developing flexible budgets, including variance analysis and the assessment of cost and variance behavior patterns. Gain a comprehensive understanding of how Standard costing and variances can be utilized as a strategic tool for driving organizational success.

Required ResourceTextSchneider, A. (2017). Managerial Accounti.docxaudeleypearl

Required Resource

Text

Schneider, A. (2017). Managerial Accounting: Decision making for the service and manufacturing sectors (2nd ed.) [Electronic version]. Retrieved from https://content.ashford.edu/

· Chapter 5: Joint Cost Allocation and Variable Costing

· Chapter 8: Cost Control Through Standard Costs

Recommended Resource

Multimedia

Crosson, S. (2007). PVA ABC JIT – 4 ABC example (Links to an external site.) [Video File]. Retrieved from http://www.youtube.com/watch?v=eyH4l3VvOCU

Discussion 1 Allocating Joint Costs

Describe the three methods used to allocate joint costs. What are the advantages/disadvantages of each allocation method? Which method would you recommend? Why? Support your position with evidence from the text or external sources. Your initial post should be 200-250 words.

Guided Response: Review several of your classmates’ postings. Respond to at least two of your classmates by asking a question to challenge their recommended allocation method. Support your question and/or comments with evidence from the text or external sources.

Discussion 2 Variable/Absorption Costing

As you read in Chapter 8, there are arguments (for and against) variable costing and absorption costing. Select one of these costing methods and explore the various arguments. Determine whether you are “for” or “against” this selected method. Provide evidence from the text to support your position. Your initial post should be 200-250 words.

Guided Response: Review several of your classmates’ postings. Respond to at least two of your classmates who explored a different costing method than your own by stating whether you agree or disagree with their position. Be sure to include cited support/examples to clarify your point of view.

LearningObjectives

After studying Chapter 8, you will be able to:

Explain the signi�icance of pro�it analysis for an organization.

Describe the major characteristics and conditions of a standard cost system.

Understand the information contained in a standard cost sheet.

Compute materials price and usage variances, and identify potential causes of such variances.

Compute labor rate and ef�iciency variances, and identify potential causes of such variances.

Explain the major considerations that are the basis of standard costs for overhead and compute

budget variances and capacity variances for overhead.

Explain why the capacity variance is related only to �ixed overhead costs.

Understand issues relating to variance investigation and disposal of variances.

8 Cost Control Through Standard Costs

nd3000/iStock/Thinkstock

Explain how standard costs can be used in various different settings.

Describe ethical considerations relating to standards and variances.

WhereDoIStartWithStandardCosts?

Jean-Claude Recca, President of Rue de Lorraine, a chain of fast-food restaurants in central France, just

returned from a reunion of his INSEAD graduating class. During the day of activities in the Riviera, he talked

with several o ...

Introduction to AI for Nonprofits with Tapp NetworkTechSoup

Dive into the world of AI! Experts Jon Hill and Tareq Monaur will guide you through AI's role in enhancing nonprofit websites and basic marketing strategies, making it easy to understand and apply.

Unit 8 - Information and Communication Technology (Paper I).pdfThiyagu K

This slides describes the basic concepts of ICT, basics of Email, Emerging Technology and Digital Initiatives in Education. This presentations aligns with the UGC Paper I syllabus.

A Strategic Approach: GenAI in EducationPeter Windle

Artificial Intelligence (AI) technologies such as Generative AI, Image Generators and Large Language Models have had a dramatic impact on teaching, learning and assessment over the past 18 months. The most immediate threat AI posed was to Academic Integrity with Higher Education Institutes (HEIs) focusing their efforts on combating the use of GenAI in assessment. Guidelines were developed for staff and students, policies put in place too. Innovative educators have forged paths in the use of Generative AI for teaching, learning and assessments leading to pockets of transformation springing up across HEIs, often with little or no top-down guidance, support or direction.

This Gasta posits a strategic approach to integrating AI into HEIs to prepare staff, students and the curriculum for an evolving world and workplace. We will highlight the advantages of working with these technologies beyond the realm of teaching, learning and assessment by considering prompt engineering skills, industry impact, curriculum changes, and the need for staff upskilling. In contrast, not engaging strategically with Generative AI poses risks, including falling behind peers, missed opportunities and failing to ensure our graduates remain employable. The rapid evolution of AI technologies necessitates a proactive and strategic approach if we are to remain relevant.

June 3, 2024 Anti-Semitism Letter Sent to MIT President Kornbluth and MIT Cor...Levi Shapiro

Letter from the Congress of the United States regarding Anti-Semitism sent June 3rd to MIT President Sally Kornbluth, MIT Corp Chair, Mark Gorenberg

Dear Dr. Kornbluth and Mr. Gorenberg,

The US House of Representatives is deeply concerned by ongoing and pervasive acts of antisemitic

harassment and intimidation at the Massachusetts Institute of Technology (MIT). Failing to act decisively to ensure a safe learning environment for all students would be a grave dereliction of your responsibilities as President of MIT and Chair of the MIT Corporation.

This Congress will not stand idly by and allow an environment hostile to Jewish students to persist. The House believes that your institution is in violation of Title VI of the Civil Rights Act, and the inability or

unwillingness to rectify this violation through action requires accountability.

Postsecondary education is a unique opportunity for students to learn and have their ideas and beliefs challenged. However, universities receiving hundreds of millions of federal funds annually have denied

students that opportunity and have been hijacked to become venues for the promotion of terrorism, antisemitic harassment and intimidation, unlawful encampments, and in some cases, assaults and riots.

The House of Representatives will not countenance the use of federal funds to indoctrinate students into hateful, antisemitic, anti-American supporters of terrorism. Investigations into campus antisemitism by the Committee on Education and the Workforce and the Committee on Ways and Means have been expanded into a Congress-wide probe across all relevant jurisdictions to address this national crisis. The undersigned Committees will conduct oversight into the use of federal funds at MIT and its learning environment under authorities granted to each Committee.

• The Committee on Education and the Workforce has been investigating your institution since December 7, 2023. The Committee has broad jurisdiction over postsecondary education, including its compliance with Title VI of the Civil Rights Act, campus safety concerns over disruptions to the learning environment, and the awarding of federal student aid under the Higher Education Act.

• The Committee on Oversight and Accountability is investigating the sources of funding and other support flowing to groups espousing pro-Hamas propaganda and engaged in antisemitic harassment and intimidation of students. The Committee on Oversight and Accountability is the principal oversight committee of the US House of Representatives and has broad authority to investigate “any matter” at “any time” under House Rule X.

• The Committee on Ways and Means has been investigating several universities since November 15, 2023, when the Committee held a hearing entitled From Ivory Towers to Dark Corners: Investigating the Nexus Between Antisemitism, Tax-Exempt Universities, and Terror Financing. The Committee followed the hearing with letters to those institutions on January 10, 202

2024.06.01 Introducing a competency framework for languag learning materials ...Sandy Millin

http://sandymillin.wordpress.com/iateflwebinar2024

Published classroom materials form the basis of syllabuses, drive teacher professional development, and have a potentially huge influence on learners, teachers and education systems. All teachers also create their own materials, whether a few sentences on a blackboard, a highly-structured fully-realised online course, or anything in between. Despite this, the knowledge and skills needed to create effective language learning materials are rarely part of teacher training, and are mostly learnt by trial and error.

Knowledge and skills frameworks, generally called competency frameworks, for ELT teachers, trainers and managers have existed for a few years now. However, until I created one for my MA dissertation, there wasn’t one drawing together what we need to know and do to be able to effectively produce language learning materials.

This webinar will introduce you to my framework, highlighting the key competencies I identified from my research. It will also show how anybody involved in language teaching (any language, not just English!), teacher training, managing schools or developing language learning materials can benefit from using the framework.

Welcome to TechSoup New Member Orientation and Q&A (May 2024).pdfTechSoup

In this webinar you will learn how your organization can access TechSoup's wide variety of product discount and donation programs. From hardware to software, we'll give you a tour of the tools available to help your nonprofit with productivity, collaboration, financial management, donor tracking, security, and more.

1. www.Oraclemfgblog.wordpress.com

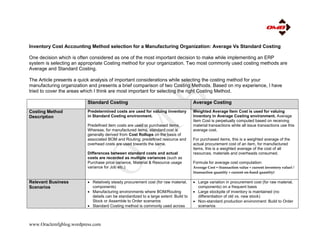

Inventory Cost Accounting Method selection for a Manufacturing Organization: Average Vs Standard Costing

One decision which is often considered as one of the most important decision to make while implementing an ERP

system is selecting an appropriate Costing method for your organization. Two most commonly used costing methods are

Average and Standard Costing.

The Article presents a quick analysis of important considerations while selecting the costing method for your

manufacturing organization and presents a brief comparison of two Costing Methods. Based on my experience, I have

tried to cover the areas which I think are most important for selecting the right Costing Method.

Standard Costing Average Costing

Costing Method

Description

Predetermined costs are used for valuing inventory

in Standard Costing environment.

Predefined item costs are used or purchased items.

Whereas, for manufactured items, standard cost is

generally derived from Cost Rollups on the basis of

associated BOM and Routing; predefined resource and

overhead costs are used towards the same.

Differences between standard costs and actual

costs are recorded as multiple variances (such as

Purchase price variance, Material & Resource usage

variance for Job etc.)

Weighted Average Item Cost is used for valuing

inventory in Average Costing environment. Average

Item Cost is perpetually computed based on receiving

material transactions while all issue transactions use this

average cost.

For purchased items, this is a weighted average of the

actual procurement cost of an item, for manufactured

items, this is a weighted average of the cost of all

resources, materials and overheads consumed.

Formula for average cost computation:

Average Cost = (transaction value + current inventory value) /

(transaction quantity + current on-hand quantity)

Relevant Business

Scenarios

Relatively steady procurement cost (for raw material,

components)

Manufacturing environments where BOM/Routing

details can be standardized to a large extent: Build to

Stock or Assemble to Order scenarios

Standard Costing method is commonly used across

Large variation in procurement cost (for raw material,

components) on a frequent basis

Large stockpile of inventory is maintained (no

differentiation of old vs. new stock)

Non-standard production environment: Build to Order

scenarios

2. www.Oraclemfgblog.wordpress.com

several Manufacturing industries spanning across

Automotive, Electronic goods, FMCG, Food and

Dairy Products, Pharmaceuticals industries

These scenarios are typically present in industries

such as Oil & Petro Chemicals, Agriculture, Heavy

Industry and Industrial Manufacturing involving large

commodities

Cost Control & Variance

Tracking

Standard Costing provides a very good control over

costs as inventory is valued based on predefined item

costs. It also provides robust performance measurement

as multiple variances are recorded based on the

differences between planned and actual costs.

Each of the variances can be monitored and analyzed to

identify the scope for efficiency improvements. Following

types of variances can be tracked:

Purchase Price and Invoice Price Variances

Material usage Variance

Resource, OSP & Overhead efficiency Variance

Standard Cost adjustment Variance

Average Costing perpetually updates the average cost

based on actual transactions and values the inventory

and Jobs based on actual transactions.

As compared to Standard Costing, there is a very limited

control on the Item Cost in Average Costing and very few

variances can be recoded. Invoice Price Variance can be

recorded.

Cost Administration Standard Costing needs active administration and

control. Following activities are typical towards

administering Standard Costing:

Revise Predefined Item Costs for each period

Perform Cost Rollups for make items in each period to

reflect revised cost for "Make" assemblies

Analyze cost variances and root cause analysis for the

recorded variances; take remedial actions to control

the variances in future periods

Perform standard cost adjustments whenever required

Average Costing requires less administration and

minimal intervention is required from business users.

Following activities may be required to administer

average costing:

Review Item Cost History time-to-time

Perform Average Cost adjustments if required

Product Pricing and

Profit Margin Calculation

Both pre-defined costs as well as recorded variances

need to be analyzed for validating Product Pricing and

estimating Product profitability accurately.

Since average costs are computed based on actual

transaction values, no variances are being recorded.

3. www.Oraclemfgblog.wordpress.com

Detailed root-cause analysis must be undertaken to

identify the exact reasons for recorded variances. Some

of them may be attributable to engineering design while

some may be due to operational inefficiencies. Doing

this analysis will help in deciding the Product pricing

realistically for the future.

Up-to-date Average Cost can be reviewed along-with the

cost history to validate Product pricing and estimate the

product profitability.

Benefits Good control over item cost and inventory valuation

Accurate tracking of variances

Good Performance Management tool: Easy to fix

responsibility for each kind of variance

Easy to identify required operational improvements

Automatically value inventory at moving average

item cost

No need to define any pre-defined costs

No need to track variances

Easily determine profit margin based on actual cost

Challenges Higher administration overhead

o Define item costs for each period

o Perform cost rollups for each period

o Variance analysis for each period

Product Profit Margin computation to include direct

costs (planned) as well as variances

Higher standardization required in engineering

phase in order to account for all operational issues.

Very limited control over item costs

No Variances are recorded and all operational

inefficiencies are included as part of actual costing

Difficult to assign responsibility for operational

inefficiencies

PS: I have not covered any system related information or setups in this article (I shall be writing another article to present

a solution to reap benefits of both costing methods in one organization based on Oracle Applications ERP platform).

Hope you will find this analysis interesting; your suggestions and feedback are most welcome!

Regards,

Manu Singhal