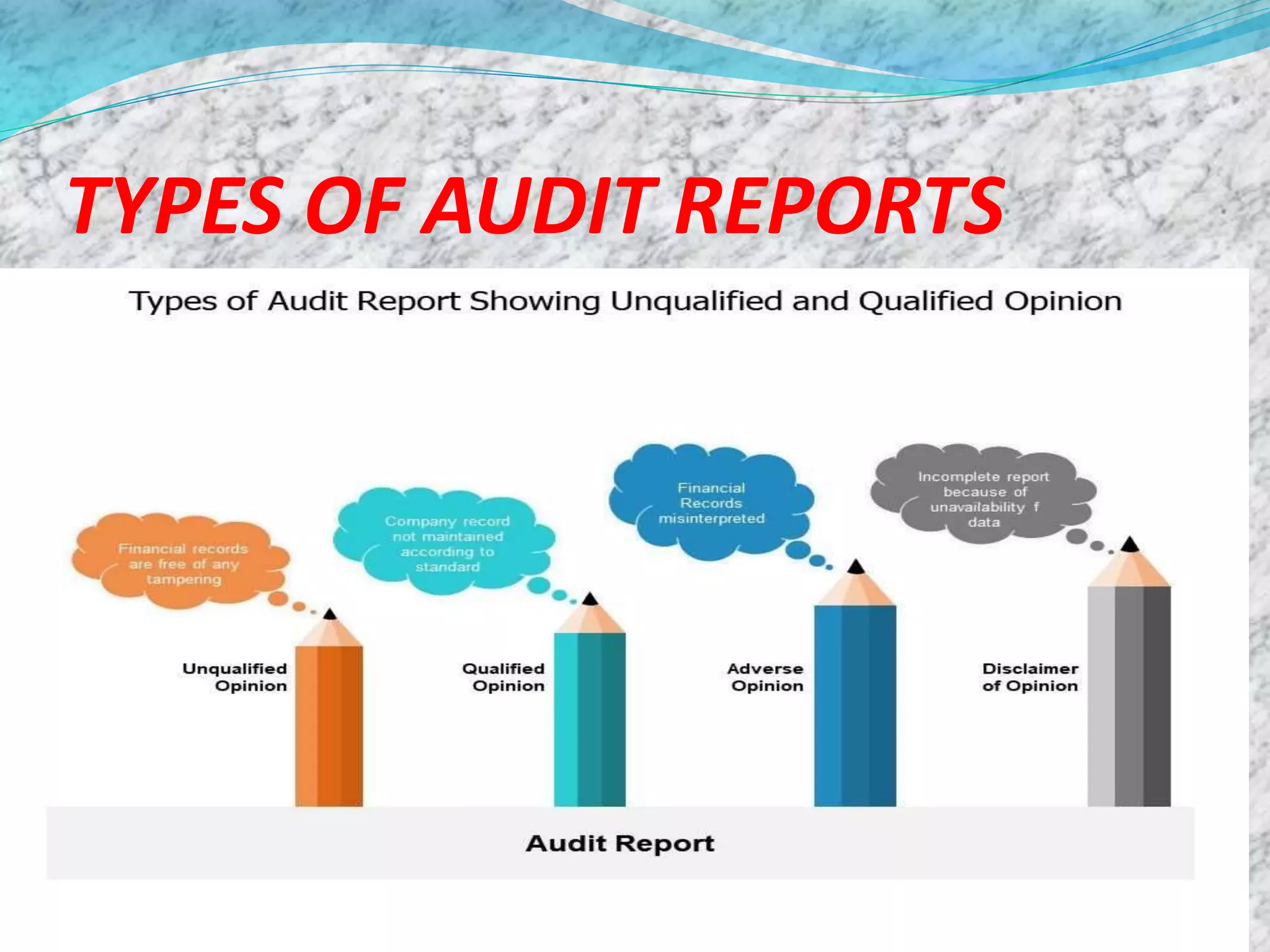

The document discusses audit committees and audit reports. It states that all listed companies and public companies meeting certain criteria regarding paid up capital, turnover, or outstanding loans must constitute an audit committee. The audit committee must have at least 3 directors, the majority of which must be independent directors. It must meet at least 4 times per year with gaps between meetings not exceeding 4 months. An audit report is a written opinion from an auditor on an entity's financial statements. Audit reports can include emphasis of matter paragraphs to draw attention to important matters.