Downloaded 39 times

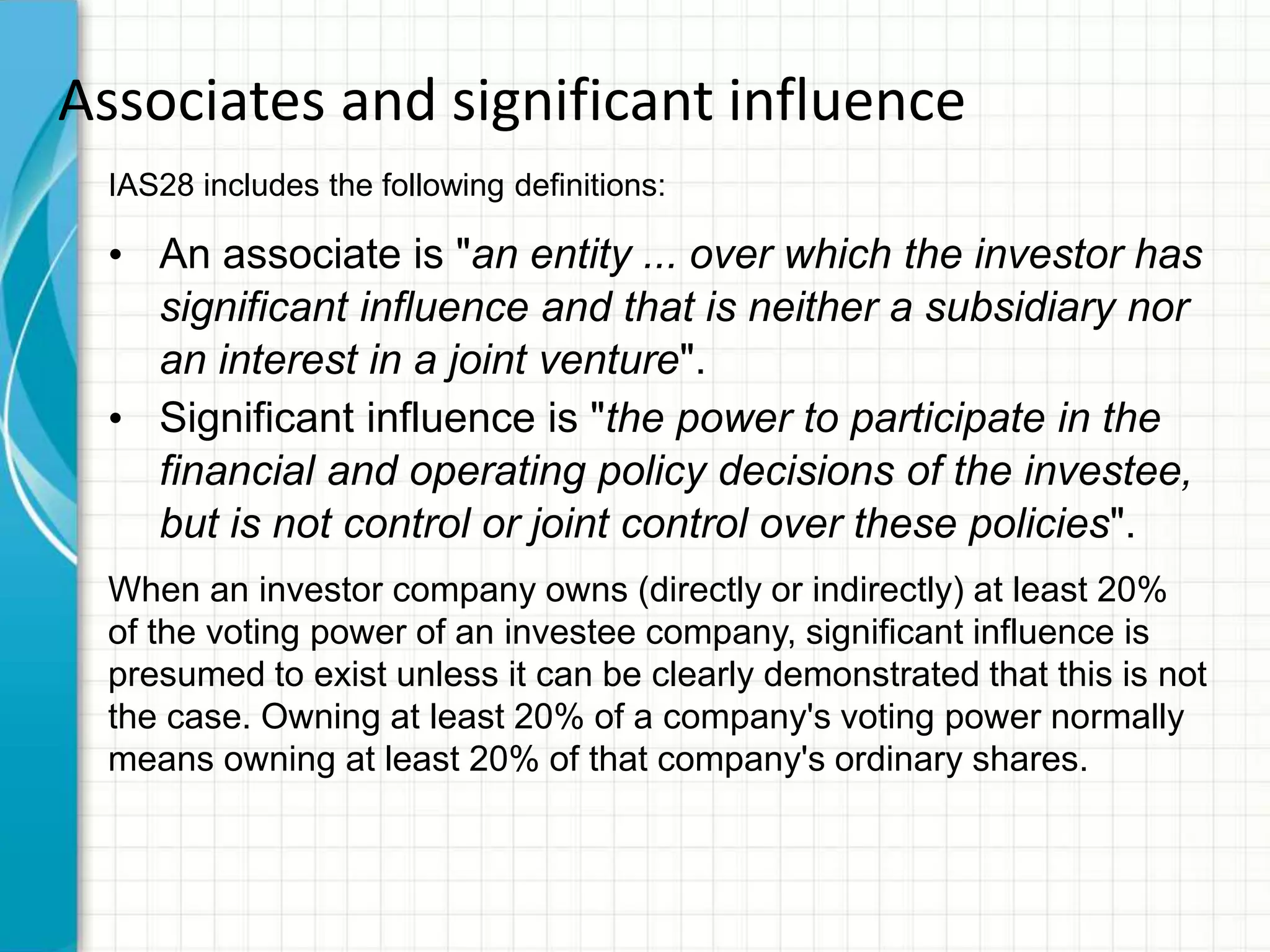

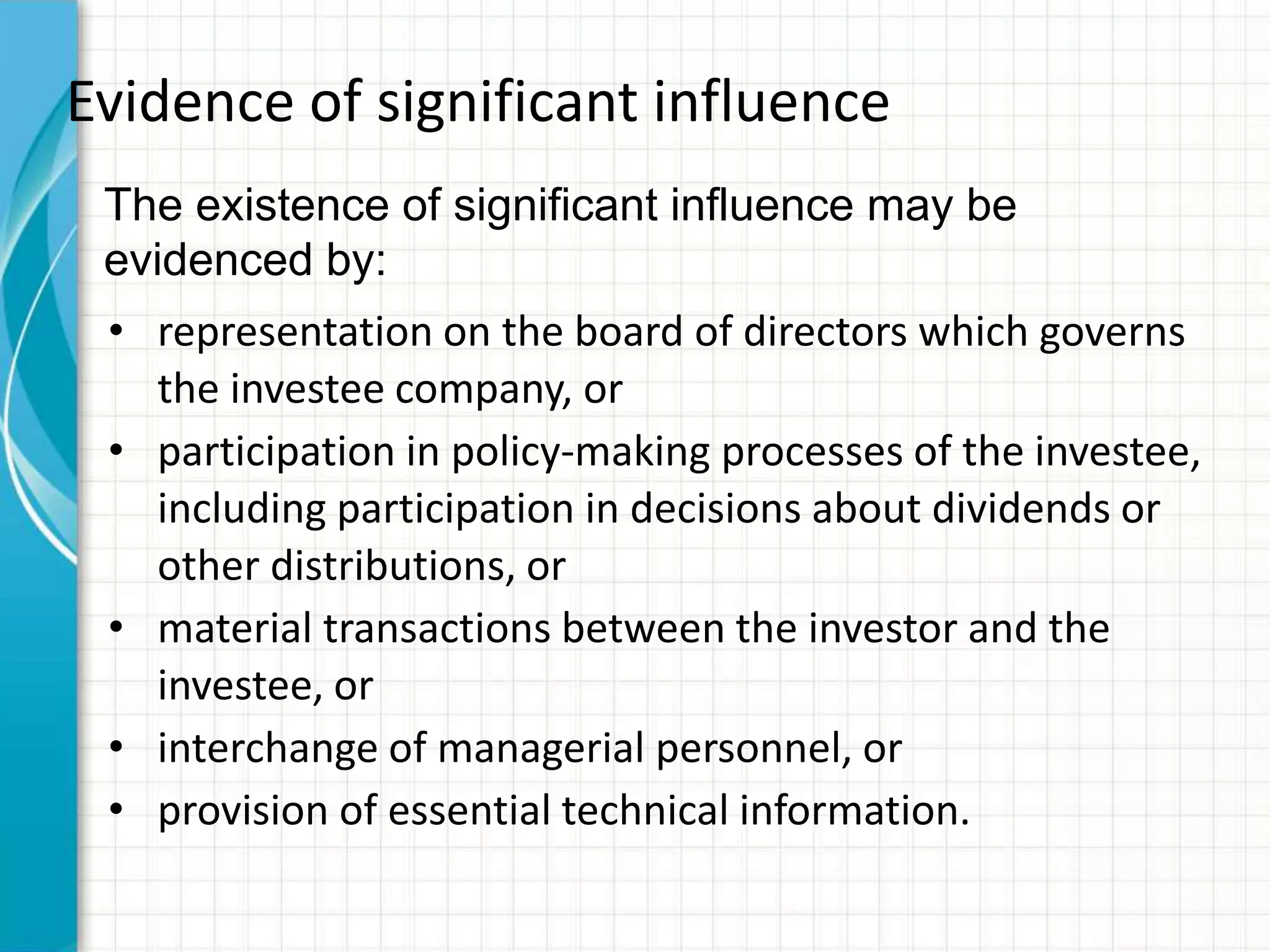

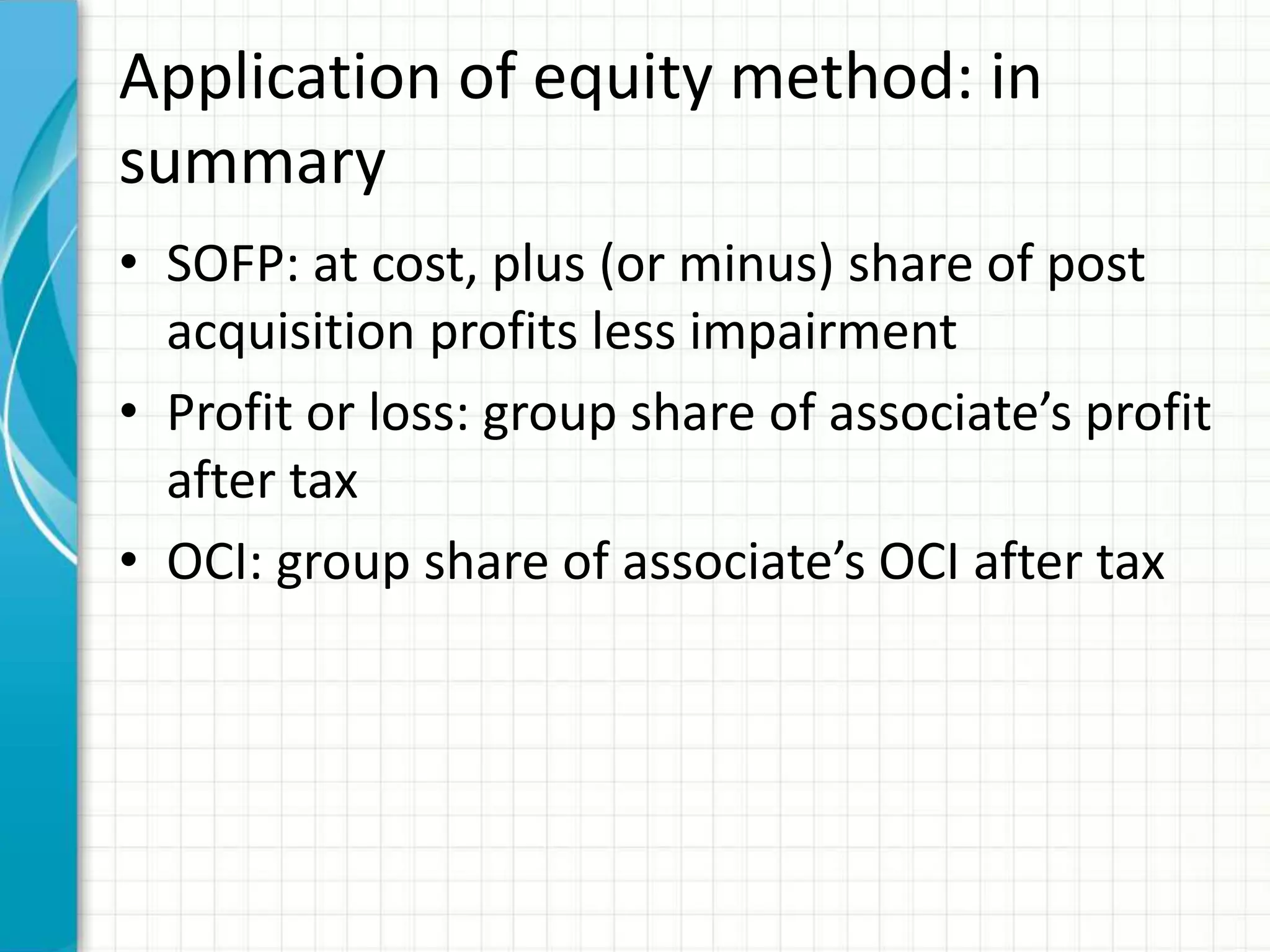

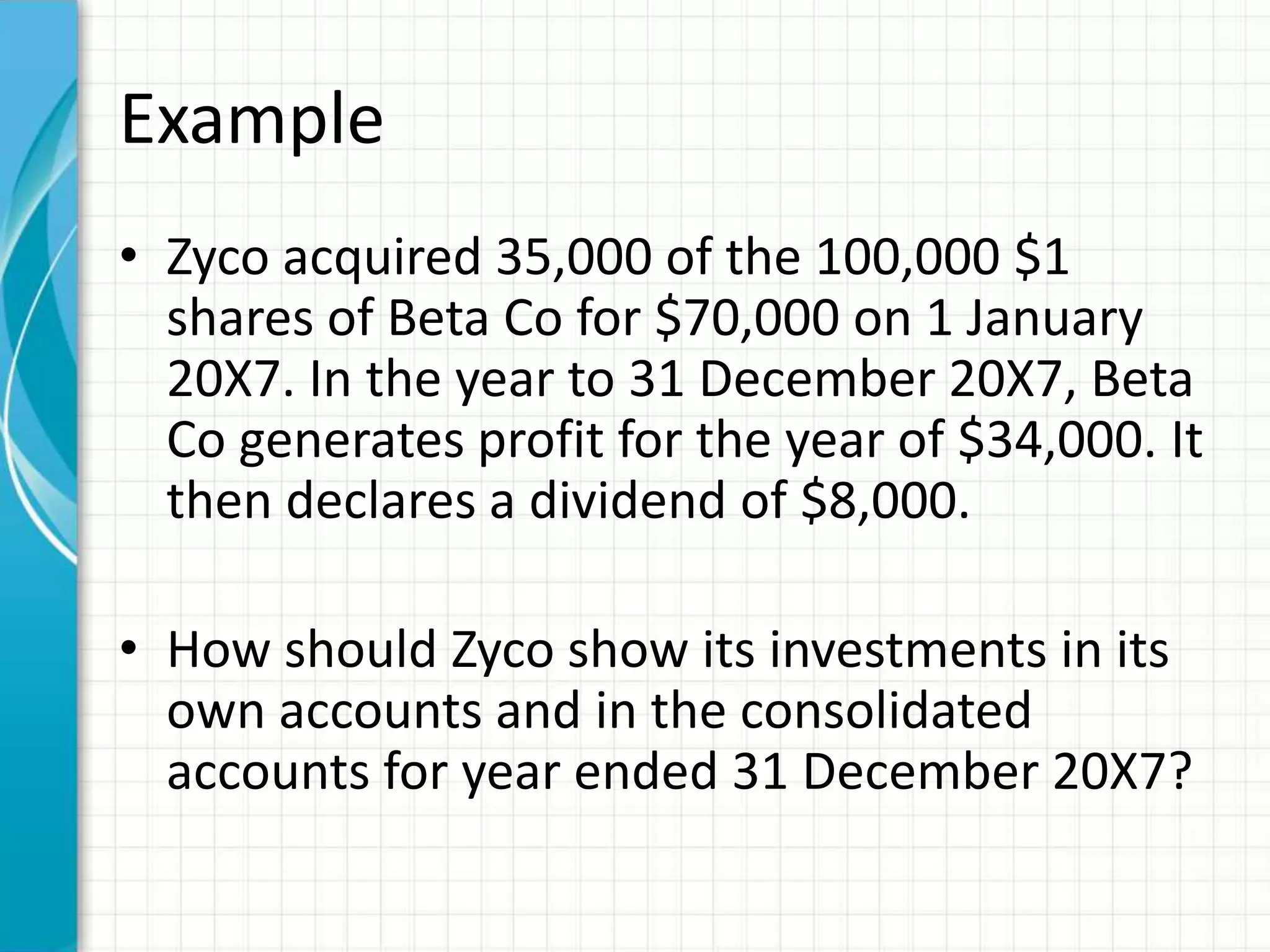

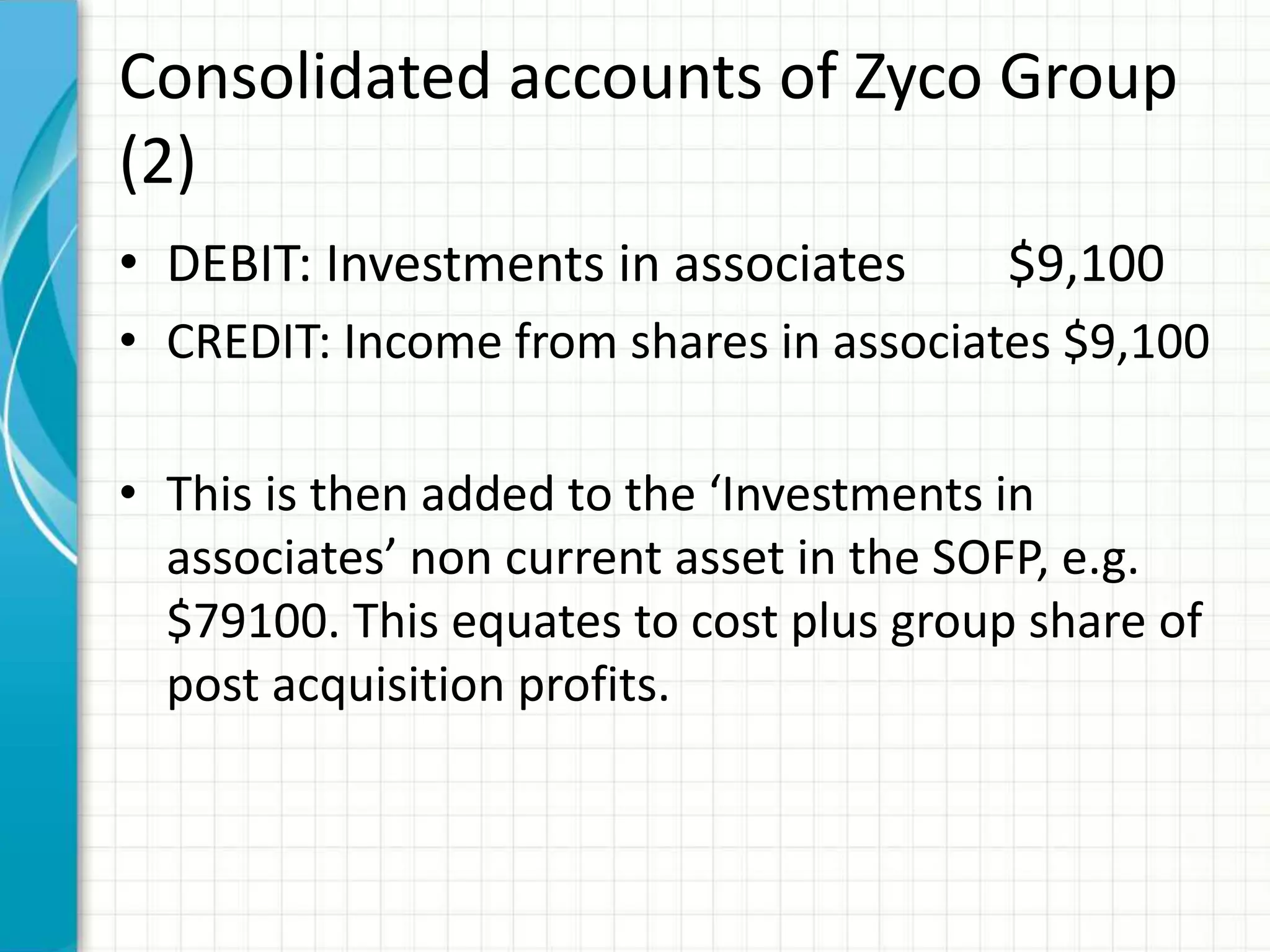

The document discusses accounting standards for associates and joint ventures. It defines associates as entities over which an investor has significant influence, but not control. Joint arrangements are either joint operations or joint ventures depending on parties' rights and obligations. The equity method is used to account for investments in associates and joint ventures, recording the investment at cost initially and adjusting it over time for the investor's share of post-acquisition profits or losses. Transactions between investors and their associates or joint ventures require elimination of unrealized profits.