Learning Objectives

At thecompletion of this chapter, you would be able to:

Describe the objectives, scope and principles prescribed by IFRS 11

Differentiate Joint Control from other forms of interest in investee

companies

Classify Joint Arrangement in to Joint Operation and Joint Ventures

Explain the accounting treatment required for joint operations

Apply the Equity method of accounting as prescribed in IAS 28

Explain the nature of Public Enterprises as provided in Proc.

#25/1992

Explain the need for having Public Enterprises in the country

2

Introduction

• IFRS 11,Joint Arrangements:

Establishes principles for Financial

reporting by parties to a joint

arrangement.

• The standard must be applied by all

entities who are party to a joint

arrangement.

4

5.

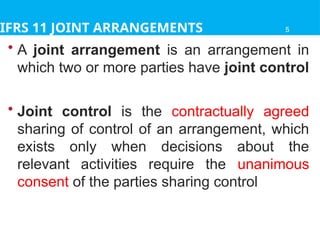

IFRS 11 JOINTARRANGEMENTS

• A joint arrangement is an arrangement in

which two or more parties have joint control

• Joint control is the contractually agreed

sharing of control of an arrangement, which

exists only when decisions about the

relevant activities require the unanimous

consent of the parties sharing control

5

6.

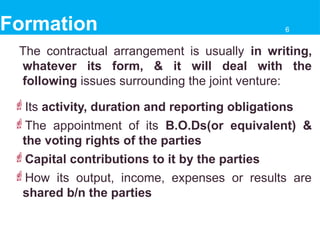

Formation

The contractual arrangementis usually in writing,

whatever its form, & it will deal with the

following issues surrounding the joint venture:

Its activity, duration and reporting obligations

The appointment of its B.O.Ds(or equivalent) &

the voting rights of the parties

Capital contributions to it by the parties

How its output, income, expenses or results are

shared b/n the parties

6

7.

Need for JointArrangement

• Reasons for Joint arrangements:

opportunity to gain new capacity and

expertise

enter related businesses or new geographic

markets or gain new technological

knowledge

gives access to greater resources, including

specialized staff and technology

shares risks

can be flexible

7

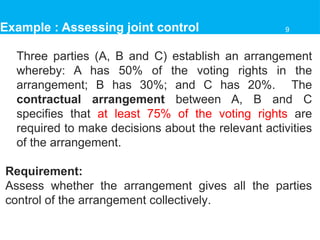

Example : Assessingjoint control

Three parties (A, B and C) establish an arrangement

whereby: A has 50% of the voting rights in the

arrangement; B has 30%; and C has 20%. The

contractual arrangement between A, B and C

specifies that at least 75% of the voting rights are

required to make decisions about the relevant activities

of the arrangement.

Requirement:

Assess whether the arrangement gives all the parties

control of the arrangement collectively.

9

10.

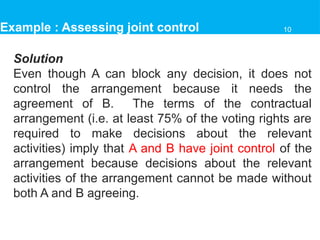

Solution

Even though Acan block any decision, it does not

control the arrangement because it needs the

agreement of B. The terms of the contractual

arrangement (i.e. at least 75% of the voting rights are

required to make decisions about the relevant

activities) imply that A and B have joint control of the

arrangement because decisions about the relevant

activities of the arrangement cannot be made without

both A and B agreeing.

Example : Assessing joint control 10

11.

Example: Assessing jointcontrol

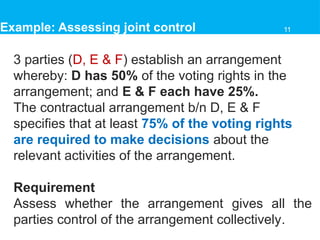

3 parties (D, E & F) establish an arrangement

whereby: D has 50% of the voting rights in the

arrangement; and E & F each have 25%.

The contractual arrangement b/n D, E & F

specifies that at least 75% of the voting rights

are required to make decisions about the

relevant activities of the arrangement.

Requirement

Assess whether the arrangement gives all the

parties control of the arrangement collectively.

11

12.

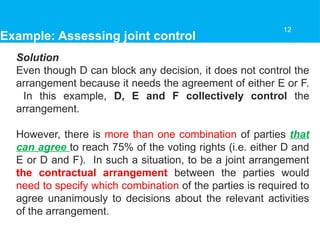

Solution

Even though Dcan block any decision, it does not control the

arrangement because it needs the agreement of either E or F.

In this example, D, E and F collectively control the

arrangement.

However, there is more than one combination of parties that

can agree to reach 75% of the voting rights (i.e. either D and

E or D and F). In such a situation, to be a joint arrangement

the contractual arrangement between the parties would

need to specify which combination of the parties is required to

agree unanimously to decisions about the relevant activities

of the arrangement.

Example: Assessing joint control

12

13.

Example: Assessing jointcontrol

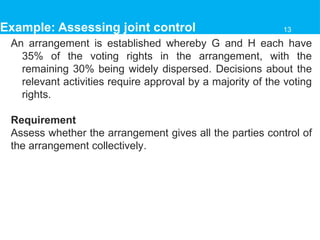

An arrangement is established whereby G and H each have

35% of the voting rights in the arrangement, with the

remaining 30% being widely dispersed. Decisions about the

relevant activities require approval by a majority of the voting

rights.

Requirement

Assess whether the arrangement gives all the parties control of

the arrangement collectively.

13

14.

Solution

G and Hhave joint control of the arrangement

only if the contractual arrangement specifies

that decisions about the relevant activities of the

arrangement require both G and H agreeing.

Example: Assessing joint control 14

15.

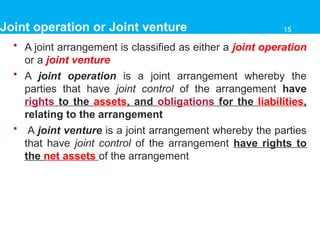

Joint operation orJoint venture

• A joint arrangement is classified as either a joint operation

or a joint venture

• A joint operation is a joint arrangement whereby the

parties that have joint control of the arrangement have

rights to the assets, and obligations for the liabilities,

relating to the arrangement

• A joint venture is a joint arrangement whereby the parties

that have joint control of the arrangement have rights to

the net assets of the arrangement

15

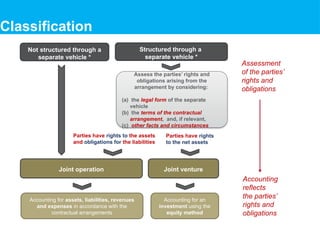

16.

Assess the parties’rights and

obligations arising from the

arrangement by considering:

(a) the legal form of the separate

vehicle

(b) the terms of the contractual

arrangement, and, if relevant,

(c) other facts and circumstances

Joint operation Joint venture

Assessment

of the parties’

rights and

obligations

Accounting for assets, liabilities, revenues

and expenses in accordance with the

contractual arrangements

Accounting for an

investment using the

equity method

Not structured through a

separate vehicle *

Structured through a

separate vehicle *

Parties have rights

to the net assets

Parties have rights to the assets

and obligations for the liabilities

Accounting

reflects

the parties’

rights and

obligations

16

Classification

17.

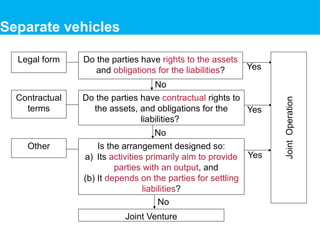

Separate vehicles

Contractual

terms

Other

Legal form

Yes

Yes

No

No

No

Yes

JointVenture

Joint

Operation

Do the parties have rights to the assets

and obligations for the liabilities?

Do the parties have contractual rights to

the assets, and obligations for the

liabilities?

Is the arrangement designed so:

a) Its activities primarily aim to provide

parties with an output, and

(b) It depends on the parties for settling

liabilities?

18.

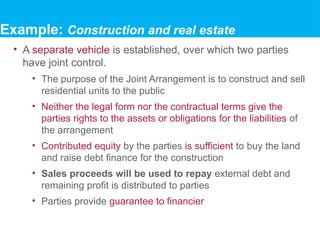

• A separatevehicle is established, over which two parties

have joint control.

• The purpose of the Joint Arrangement is to construct and sell

residential units to the public

• Neither the legal form nor the contractual terms give the

parties rights to the assets or obligations for the liabilities of

the arrangement

• Contributed equity by the parties is sufficient to buy the land

and raise debt finance for the construction

• Sales proceeds will be used to repay external debt and

remaining profit is distributed to parties

• Parties provide guarantee to financier

Example: Construction and real estate

19.

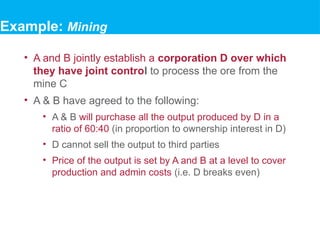

• A andB jointly establish a corporation D over which

they have joint control to process the ore from the

mine C

• A & B have agreed to the following:

• A & B will purchase all the output produced by D in a

ratio of 60:40 (in proportion to ownership interest in D)

• D cannot sell the output to third parties

• Price of the output is set by A and B at a level to cover

production and admin costs (i.e. D breaks even)

Example: Mining

20.

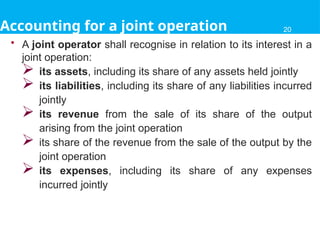

Accounting for ajoint operation

• A joint operator shall recognise in relation to its interest in a

joint operation:

its assets, including its share of any assets held jointly

its liabilities, including its share of any liabilities incurred

jointly

its revenue from the sale of its share of the output

arising from the joint operation

its share of the revenue from the sale of the output by the

joint operation

its expenses, including its share of any expenses

incurred jointly

20

21.

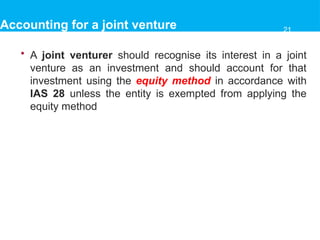

Accounting for ajoint venture

• A joint venturer should recognise its interest in a joint

venture as an investment and should account for that

investment using the equity method in accordance with

IAS 28 unless the entity is exempted from applying the

equity method

21

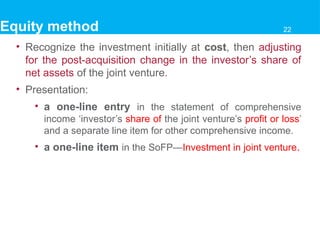

22.

• Recognize theinvestment initially at cost, then adjusting

for the post-acquisition change in the investor’s share of

net assets of the joint venture.

• Presentation:

• a one-line entry in the statement of comprehensive

income ‘investor’s share of the joint venture’s profit or loss’

and a separate line item for other comprehensive income.

• a one-line item in the SoFP—Investment in joint venture.

Equity method 22

23.

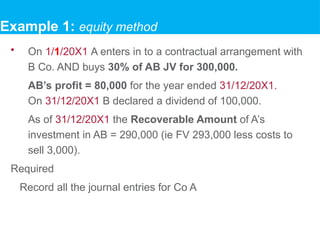

Example 1: equitymethod

• On 1/1/20X1 A enters in to a contractual arrangement with

B Co. AND buys 30% of AB JV for 300,000.

AB’s profit = 80,000 for the year ended 31/12/20X1.

On 31/12/20X1 B declared a dividend of 100,000.

As of 31/12/20X1 the Recoverable Amount of A’s

investment in AB = 290,000 (ie FV 293,000 less costs to

sell 3,000).

Required

Record all the journal entries for Co A

24.

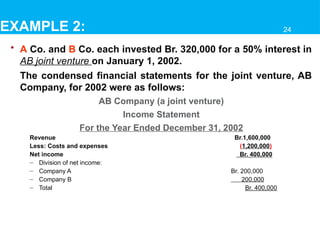

EXAMPLE 2:

• ACo. and B Co. each invested Br. 320,000 for a 50% interest in

AB joint venture on January 1, 2002.

The condensed financial statements for the joint venture, AB

Company, for 2002 were as follows:

AB Company (a joint venture)

Income Statement

For the Year Ended December 31, 2002

Revenue Br.1,600,000

Less: Costs and expenses (1,200,000)

Net income Br. 400,000

– Division of net income:

– Company A Br. 200,000

– Company B 200,000

– Total Br. 400,000

24

25.

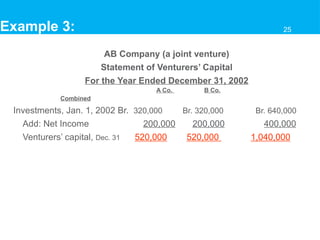

Example 3:

AB Company(a joint venture)

Statement of Venturers’ Capital

For the Year Ended December 31, 2002

A Co. B Co.

Combined

Investments, Jan. 1, 2002 Br. 320,000 Br. 320,000 Br. 640,000

Add: Net Income 200,000 200,000 400,000

Venturers’ capital, Dec. 31 520,000 520,000 1,040,000

25

26.

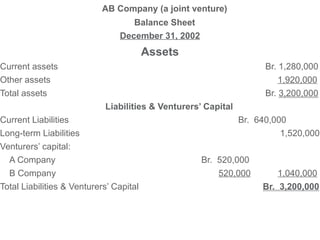

AB Company (ajoint venture)

Balance Sheet

December 31, 2002

Assets

Current assets Br. 1,280,000

Other assets 1,920,000

Total assets Br. 3,200,000

Liabilities & Venturers’ Capital

Current Liabilities Br. 640,000

Long-term Liabilities 1,520,000

Venturers’ capital:

A Company Br. 520,000

B Company 520,000 1,040,000

Total Liabilities & Venturers’ Capital Br. 3,200,000

26

27.

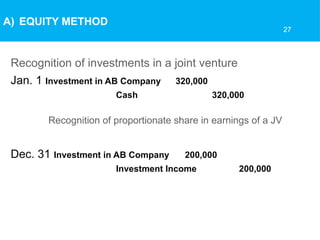

Recognition of investmentsin a joint venture

Jan. 1 Investment in AB Company 320,000

Cash 320,000

Recognition of proportionate share in earnings of a JV

Dec. 31 Investment in AB Company 200,000

Investment Income 200,000

A) EQUITY METHOD

27

28.

• The IFRSrequires an entity to disclose information that

enables users of FS to evaluate:

• the nature of, and risks associated with, its interests in other

entities; and

• the effects of those interests on its financial position, financial

performance and cash flows.

28

Disclosures 28

29.

Disclosure: Joint arrangementsand associates

Nature, extent and financial effects of interests in

joint arrangements and associates,

• List and nature of interests

• Quantitative financial information

• Unrecognised share of losses of JVs and

associates

• Fair value (if published quoted prices available)

• Nature and extent of any significant restrictions

on transferring funds

Nature of, and changes in, the risks

associated with the involvement

• Commitments and contingent liabilities

29

30.

Judgements and estimates

•An entity must disclose information about significant

judgements and assumptions it has made in determining…

• joint control (see IFRS 11) of an arrangement

• type of joint arrangement when the arrangement has been

structured through a separate vehicle

30

Disclosure: Joint arrangements and associates 30

Defn: are autonomousor semi-autonomous bodies

owned by the gov’t & engaged in providing services and

or products.

Background:

• The growth of public enterprises has been partly by

nationalization and partly through creation of new ones.

• Some industries are also reserved for the public

sector as a matter of national policy. EX: Airways,

defense industries, railways, Tele, energy, Shipping

… .

Public Enterprises 32

33.

Because:

– Limitation ofthe free price mechanism

– Basic industries need huge investment

– Government’s duty to help in economic dev’t

– Creation of economic surpluses and their utilization

– Final choice of projects are made in the interest of the

economy as a whole

– If social benefits exceed social costs in the case of

any service, then its production should be taken up

– Limitation on demand of merit goods on account of price

if left in private hands

– The overall economic policy of a country may dictate

the use of public enterprises in some sectors

Why Public enterprises? 33

34.

Formation Provision:

• Everyenterprise shall be established by regulation

and the establishment regulation shall contain:

– The name of the enterprise

– A st. the enterprise shall be governed by the proc.

– The purpose for which the enterprise is established

– The authorized capital

– The amt of initial cap. paid up both in cash & in kind

– Not less than 25% of Auth. Cap.

– A st. that the ent. shall not be liable beyond its T-assets

= Limited Liability St.

– The head office of the enterprise

– A st. that may authorize the enterprise to open branches

– The name of the supervising authority

– The duration for which the enterprise is established

34

35.

• Each enterpriseshall have:

– A supervising authority

– Designated by the Council of Ministers

– Ex: FDRE Public Financial Enterprises

Agency

– A management board (3-12 In number)

– Management

– Necessary staff

Organization 35

36.

Accounting for PublicEnterprises

• Public enterprises are state owned, state controlled

business enterprises.

• They are characterized by public purpose, public

o/ship & control.

• Their accounting aspect is the same as business

accounting with minor differences in the owners’ equity

section as there are no shares and shareholders in

PEs.

36

37.

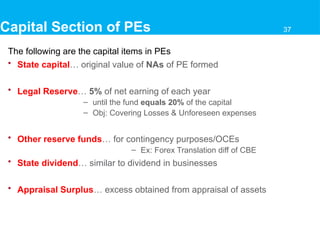

Capital Section ofPEs

The following are the capital items in PEs

• State capital… original value of NAs of PE formed

• Legal Reserve… 5% of net earning of each year

– until the fund equals 20% of the capital

– Obj: Covering Losses & Unforeseen expenses

• Other reserve funds… for contingency purposes/OCEs

– Ex: Forex Translation diff of CBE

• State dividend… similar to dividend in businesses

• Appraisal Surplus… excess obtained from appraisal of assets

37

38.

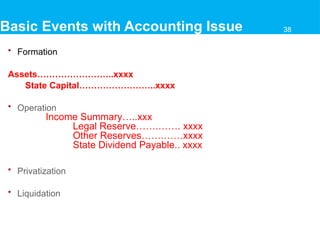

Basic Events withAccounting Issue

• Formation

Assets……………………..xxxx

State Capital……………………..xxxx

• Operation

Income Summary…..xxx

Legal Reserve…….……. xxxx

Other Reserves…….……xxxx

State Dividend Payable.. xxxx

• Privatization

• Liquidation

38

39.

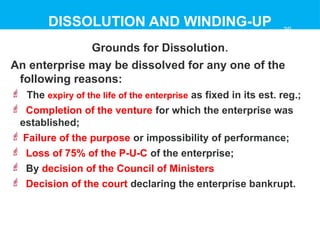

DISSOLUTION AND WINDING-UP

Groundsfor Dissolution.

An enterprise may be dissolved for any one of the

following reasons:

The expiry of the life of the enterprise as fixed in its est. reg.;

Completion of the venture for which the enterprise was

established;

Failure of the purpose or impossibility of performance;

Loss of 75% of the P-U-C of the enterprise;

By decision of the Council of Ministers

Decision of the court declaring the enterprise bankrupt.

39

#29 Main change from IAS 28 and IAS 31: the detailed quantitative summarised financial information for individually material JVs and associates, which aims to help users analyse the reporting entity’s activities that are conducted through JVs and associates, and to value the reporting entity’s investment in those entities (eg they will have a rough idea about the net dent position and will have information to be able to calculate EBITDA).