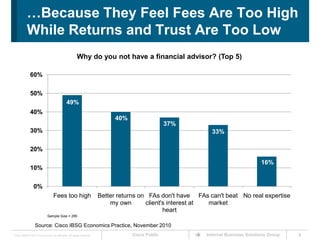

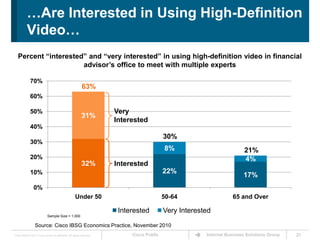

The document discusses the findings of a Cisco wealth management survey indicating that under-50 investors lack confidence in financial markets and often spread their assets across multiple firms due to dissatisfaction with high fees and low returns. This demographic, which holds 28% of U.S. assets, is tech-savvy and shows a strong interest in utilizing technology and online communities for investment management. With $18 billion in revenue at stake, the wealth management industry is urged to adapt to these investors' preferences for improved service and interaction.