Downloaded 27 times

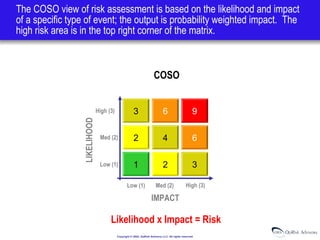

The document discusses operational risk measurement using internal and external loss data to calculate aggregate mean loss and aggregate Value at Risk (VaR). Loss events are placed in a risk matrix and combined to form loss distributions for each risk type. A Monte Carlo simulation is then used to calculate the 99th percentile VaR, providing a measure of unexpected loss exposure. This integrated approach allows measurement of both expected and unexpected operational risk levels across an organization.