Download to read offline

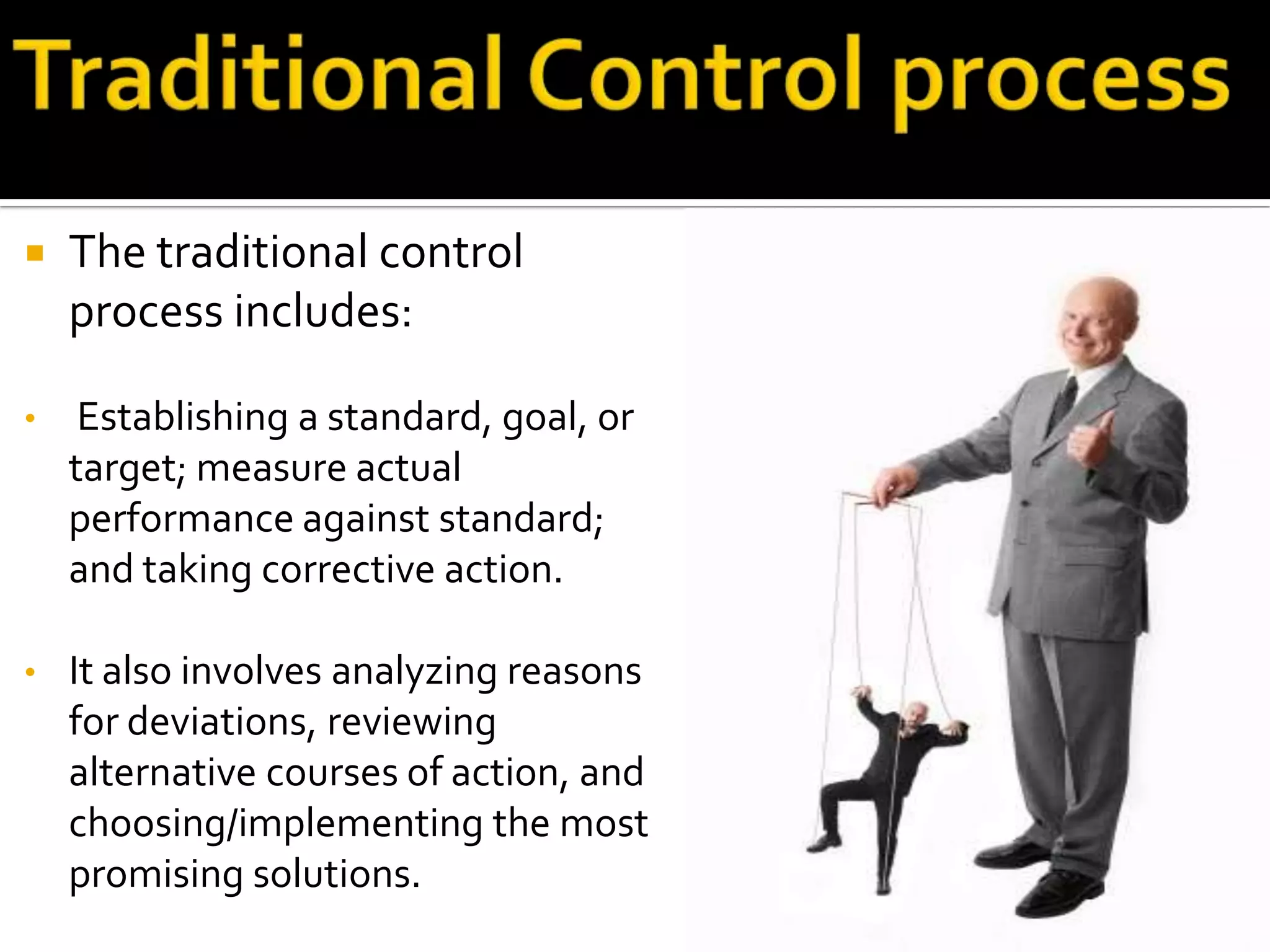

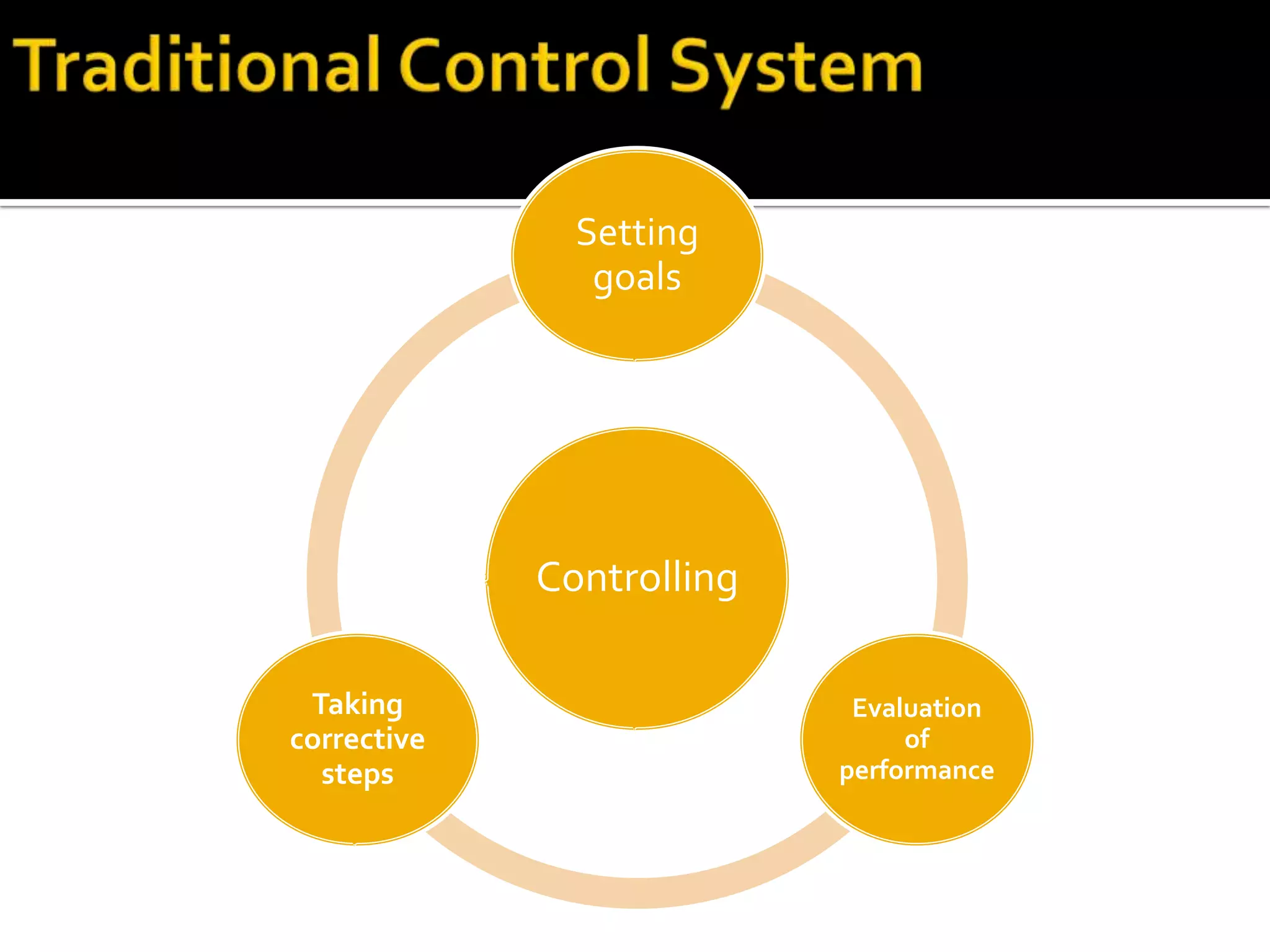

The document discusses traditional control processes used in business. It describes traditional control systems as involving setting standards and then monitoring performance. There are three main types of traditional controls: diagnostic controls which ensure goals are being met and issues can be explained, boundary controls which establish rules and identify actions to avoid, and interactive controls which allow for real-time strategic monitoring through face-to-face communication. Commitment-based controls rely on employee self-control and mutual understanding to keep things on track.