Controlling

Controlling means comparingthe actual performance of an organization with the planned

performance and taking corrective actions if the actual performance does not match the

planned performance.

Controlling cannot prevent the deviation in actual and planned performance; however, it can

minimize the deviations by taking corrective actions and decisions that can reduce their

recurrence.

3.

Definitions of Controlling

“ManagerialControl implies the measurement of accomplishment against the standard and

the correction of deviations to assure attainment of objectives according to plans.” Koontz

and O’ Donnell

“Control is the process of bringing about conformity of performance with planned action.”

Dale Henning

4.

Nature of Controlling

1.Goal-oriented function:

It aims at ensuring that the resources of the organization are used effectively and

efficiently.

2. Continuous process:

It means that once the actual performance and standard performance of a business are

compared and corrective actions are taken, the controlling process does not end.

3. All-pervasive:

It means that the controlling function is exercised by the firms at all levels of management.

4. A forward-looking and backward-looking function:

As a forward-looking function, it aims at improving the future performance of an

organization on the basis of its past experiences.

However, as a backward-looking function, it measures and compares the actual

performance and planned performance (fixed in past) of the organization.

5.

Importance of Controlling

Controllingfunction is important for every organization due to the following reasons:

1. Accomplishing Organizational Goals

Controlling is a goal-oriented process as it aims at determining whether the pre-determined

plans are being performed accordingly and whether required progress is made towards the

achievement of the objectives.

2. Judging Accuracy of Standards

An effective controlling process can help an organization in verifying whether or not the firm

has set the standards accurate.

3. Making Efficient Use of Resources

Controlling helps an organization in reducing wastage of resources, as it aims at ensuring that

every activity of the firm is performed according to the pre-determined goals.

6.

4. Improving EmployeeMotivation

As controlling process includes comparing the pre-determined goals of an organization

with its actual performance, it properly communicates the role of employees in advance.

5. Ensuring Order and Discipline

An efficient control system in an organization can help its managers in creating an

atmosphere of discipline and order in the firm.

6. Facilitating Coordination in Action

Controlling process also helps an organization in facilitating coordination between different

divisions and departments by providing the employees with unity of direction.

7.

Limitations of Controlling

1.Difficulty in Setting Quantitative Standards

When an organization cannot define its standards in quantitative terms, the controlling

system becomes less effective.

For example, it is difficult to measure the human behavior of employees in quantitative

terms, which makes it difficult for the firm to measure their performance from the

standards.

2. Little Control on External Factors

The controlling system of an organization can effectively control the internal factors;

however, it is not easy to control the external factors of an organization.

For example, a firm can check and control any change in its production (internal factor),

but cannot keep a check on the changing technological advancement, government policies,

etc. (external factors).

8.

3. Resistance fromemployees

The effectiveness of the controlling system highly depends on whether or not the employees

have accepted the process. It means that if the employees think of the control system as a

restriction on their freedom, they will resist the system.

For example, the employees of an organization might object when they are kept under

various restrictions making them feel their freedom is being taken.

4. Costly Affair

Controlling is an expensive process, which means that every employee’s performance has to

be measured and reported to the higher authorities, which requires a lot of costs, time, and

effort. Because of this reason, it becomes difficult for small business firms to afford such an

expensive system.

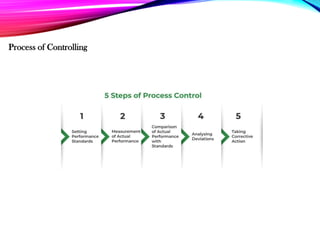

1. Setting PerformanceStandards

The first step of the process of controlling is to establish standards of performance against

which the actual performance of the organization is measured.

2. Measurement of Actual Performance

Once the organization has established the standards, the second step of the process of

controlling is to measure the actual performance in a reliable and objective manner.

3.Comparison of Actual Performance with Standards

The third step of the process of controlling is to compare the actual performance of the

organization with the established standards (in the first step).

By comparing the actual performance with the standards, an organization can determine the

deviation between them.

11.

4. Analyzing Deviations

Theactual performance and set standards of an organisation rarely match with each other.

Usually, there is always some variation between the expected and actual performance.

5. Taking Corrective Action

The last and final step of the process of controlling is to take corrective action. If the

deviations are within the acceptable limits set by the managers, then there is no need to take

corrective action.

However, if the deviations go beyond the set acceptable limit in the key areas, then proper and

immediate managerial actions are required. An organization can easily rectify the defects in

the actual performance through the corrective steps.

12.

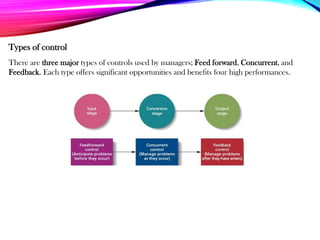

Types of control

Thereare three major types of controls used by managers; Feed forward, Concurrent, and

Feedback. Each type offers significant opportunities and benefits four high performances.

13.

Feed forward controlis also called preliminary control; these take place before any work

takes place.

They ensure that all objective for a project are clear, and that the right resources are made

available for those who need them in order to correctly accomplish any assigned tasks.

The goal of these controls is to solve problems before they are able to occur. It is a forward-

thinking approach, and is very important for company’s to establish them before working on

projects.

Feed forward Control

14.

Concurrent control focuseson what is happening during the actual work process; this is the

step following feed forward control.

These are sometimes referred to as steering control, because they make sure all things are

being done according to the original or revised plans.

The goal of this type of control is to solve problems as they occur, it is important to try to

solve problems right away so that other ones do not occur, as many projects rely on previous

steps before moving on.

Concurrent Control

15.

Feedback control isalso called post-action control; simply because these take place after the

work is complete.

This is the final major type of control that managers use; feedback control focuses on the

quality of the end result, instead of the inputs and outputs.

The main goals at this stage are to solve problems after they have occurred, and to prevent

future ones. Not all problems are identified and solved in concurrent control, but however,

can be addressed afterwards.

Feedback Control

A technique to find root

causes is the 5 whys approach

16.

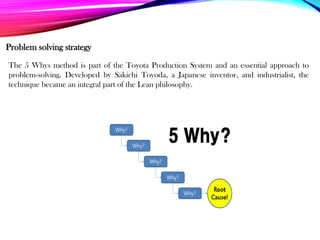

Problem solving strategy

The5 Whys method is part of the Toyota Production System and an essential approach to

problem-solving. Developed by Sakichi Toyoda, a Japanese inventor, and industrialist, the

technique became an integral part of the Lean philosophy.

17.

5 Whys

The 5whys is a simple problem technique that easily gets to the root of a problem. It is a

strategy in which when a problem occurs, you simply ask “why?”.

After you get an answer, you then ask “why?” again, until you reach the root. It is quite

common that your problem will not be solved with just one why, often there a multiple whys

that need to be answered.

This technique is not limited to only 5, a problem may be solved with 3, 5, 8, and so on.

18.

1. What isthe problem?

The first stage in this problem solving process is defining what exactly the problem is. It is

important to be specific and clear when defining this problem.

2. What is my plan?

Think of at least 2-3 possible strategies to solve your problem. Find out exactly where and

what needs to be investigated.

3. What might happen if?

From the possible strategies in the previous step, choose the one that has the best fit. This

would be the one that is most likely to succeed, and have the least amount of drawbacks.

4. Try it out!

Implement the chosen strategy. If this seems to work, move on to the next step.

5. Measure/Evaluate

Did your strategy work? If not, repeat these steps with a new strategy; if it did, great, your

problem is solved!

Basic 5 Step Approach

19.

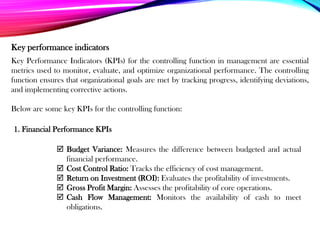

Key performance indicators

KeyPerformance Indicators (KPIs) for the controlling function in management are essential

metrics used to monitor, evaluate, and optimize organizational performance. The controlling

function ensures that organizational goals are met by tracking progress, identifying deviations,

and implementing corrective actions.

Below are some key KPIs for the controlling function:

1. Financial Performance KPIs

Budget Variance: Measures the difference between budgeted and actual

financial performance.

Cost Control Ratio: Tracks the efficiency of cost management.

Return on Investment (ROI): Evaluates the profitability of investments.

Gross Profit Margin: Assesses the profitability of core operations.

Cash Flow Management: Monitors the availability of cash to meet

obligations.

20.

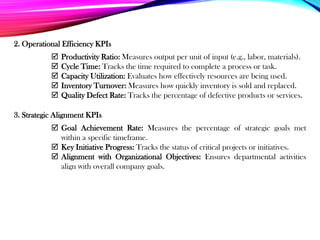

2. Operational EfficiencyKPIs

3. Strategic Alignment KPIs

Productivity Ratio: Measures output per unit of input (e.g., labor, materials).

Cycle Time: Tracks the time required to complete a process or task.

Capacity Utilization: Evaluates how effectively resources are being used.

Inventory Turnover: Measures how quickly inventory is sold and replaced.

Quality Defect Rate: Tracks the percentage of defective products or services.

Goal Achievement Rate: Measures the percentage of strategic goals met

within a specific timeframe.

Key Initiative Progress: Tracks the status of critical projects or initiatives.

Alignment with Organizational Objectives: Ensures departmental activities

align with overall company goals.

21.

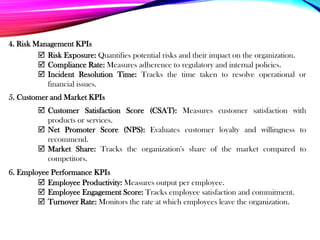

4. Risk ManagementKPIs

5. Customer and Market KPIs

6. Employee Performance KPIs

Risk Exposure: Quantifies potential risks and their impact on the organization.

Compliance Rate: Measures adherence to regulatory and internal policies.

Incident Resolution Time: Tracks the time taken to resolve operational or

financial issues.

Customer Satisfaction Score (CSAT): Measures customer satisfaction with

products or services.

Net Promoter Score (NPS): Evaluates customer loyalty and willingness to

recommend.

Market Share: Tracks the organization's share of the market compared to

competitors.

Employee Productivity: Measures output per employee.

Employee Engagement Score: Tracks employee satisfaction and commitment.

Turnover Rate: Monitors the rate at which employees leave the organization.