Download to read offline

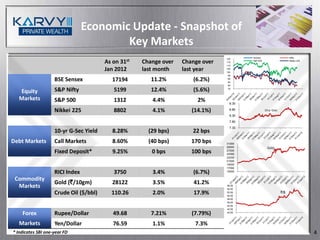

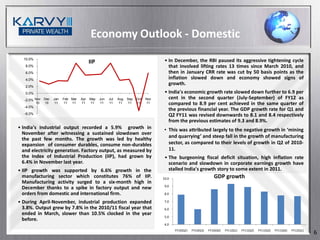

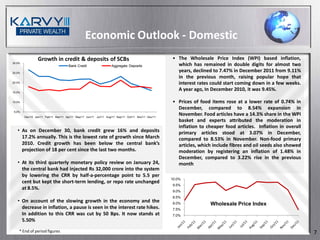

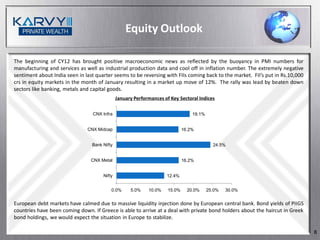

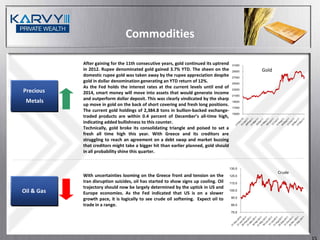

The document provides an economic and market outlook for February 2012. It notes that while recent increases in risk asset prices globally may be due to a turnaround in sentiment rather than fundamentals, several domestic avenues like long term debt, mid cap equities and infrastructure companies could provide returns with a genuine long term investment horizon. India's GDP growth slowed in the second quarter of FY12, but industrial output grew 5.9% in November. Inflation declined to 7.47% in December raising hopes that interest rates may start to fall. The equity market rallied in January led by banking, metals and capital goods sectors.