Download to read offline

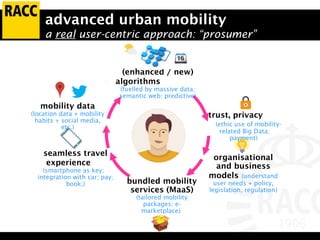

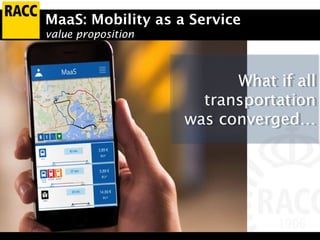

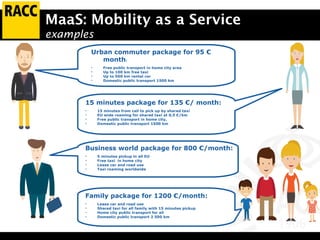

The document discusses challenges and innovations in urban mobility, emphasizing the impact of urbanization and the need for new mobility concepts. Key trends include the rise of connected and autonomous vehicles, the role of smartphones as travel assistants, and the emergence of Mobility as a Service (MaaS) to offer tailored transportation solutions. It highlights the importance of data integration, user-centric approaches, and the potential for innovative business models in addressing urban congestion and enhancing mobility experiences.