Downloaded 9,921 times

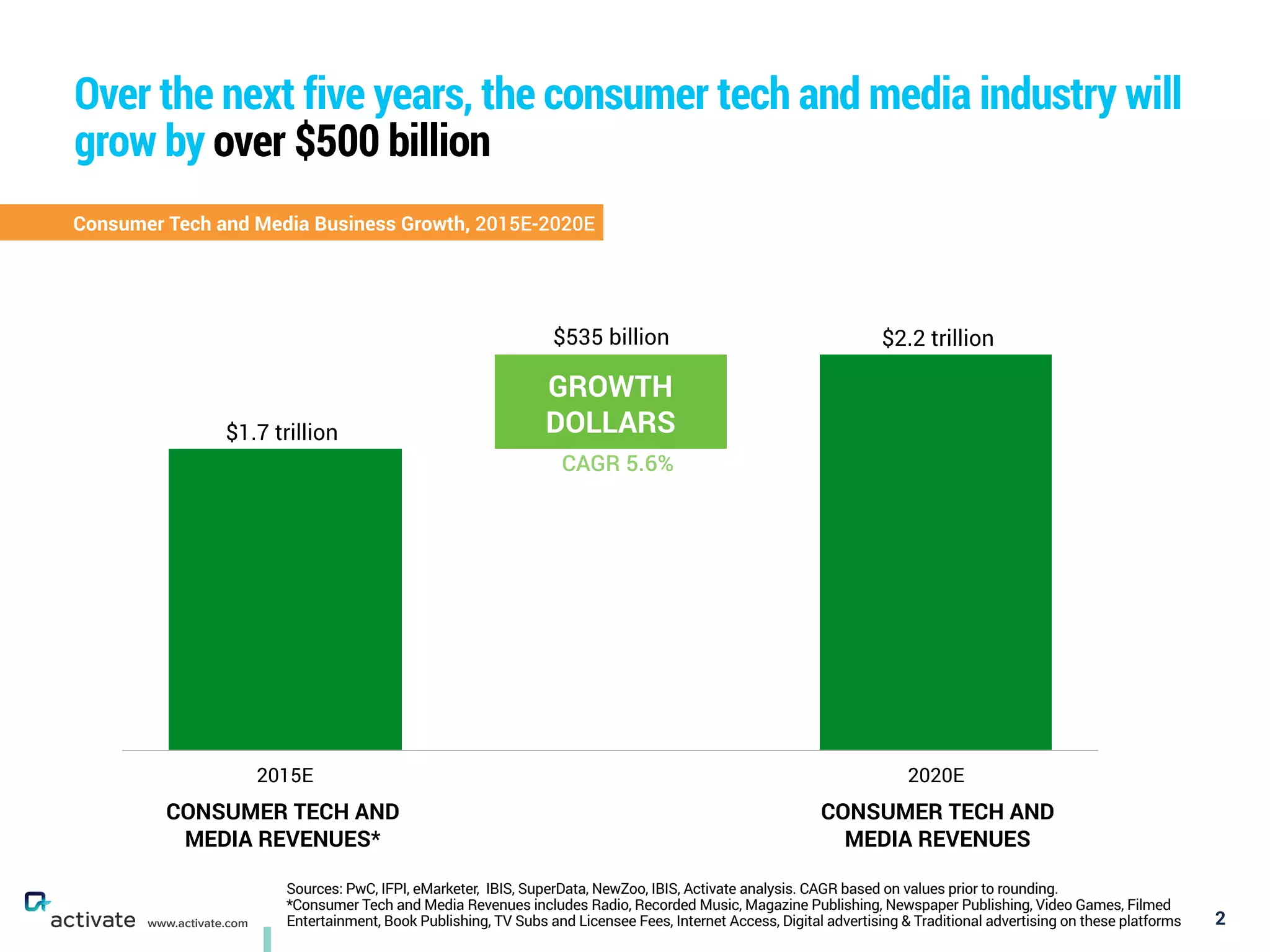

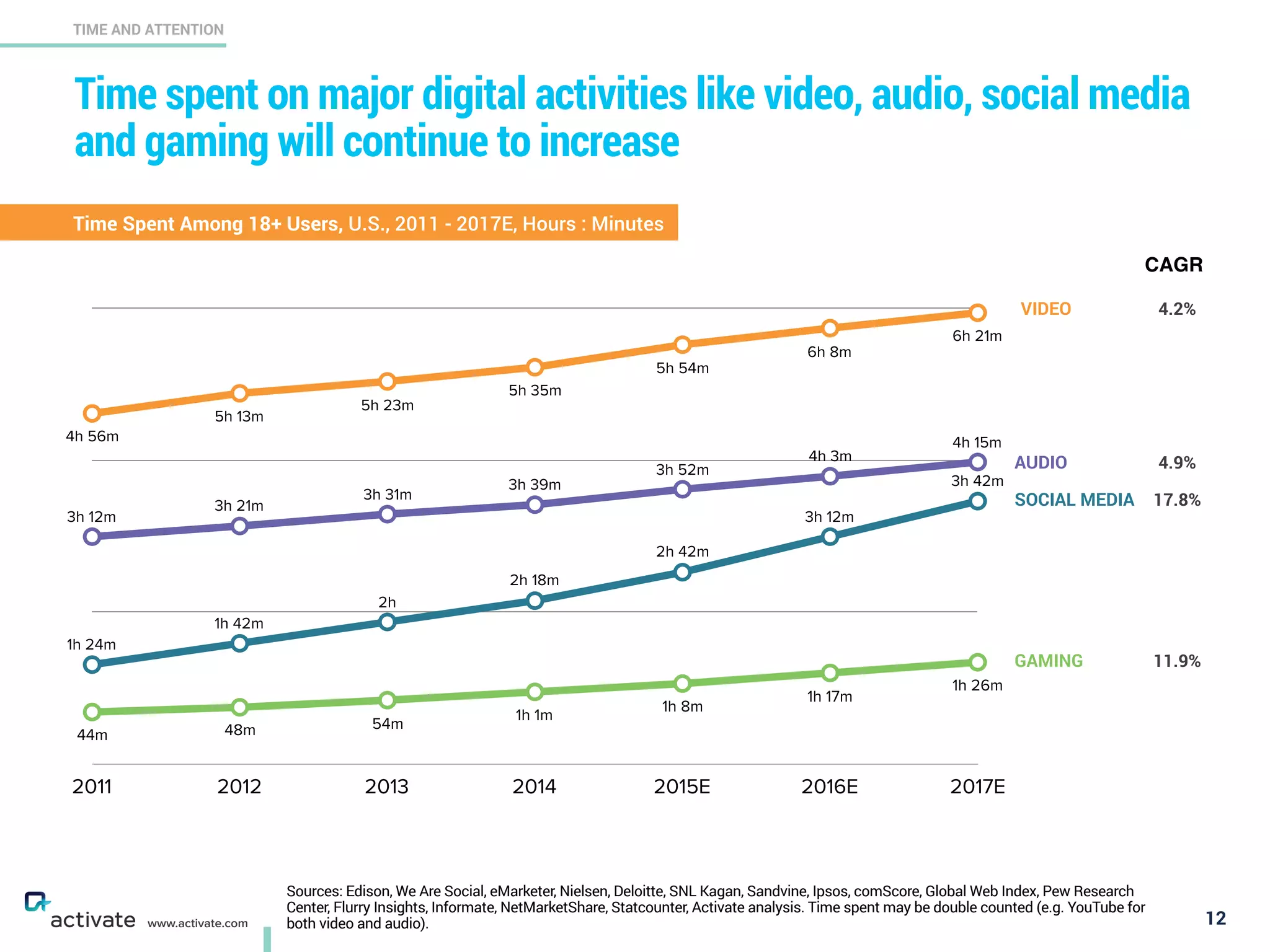

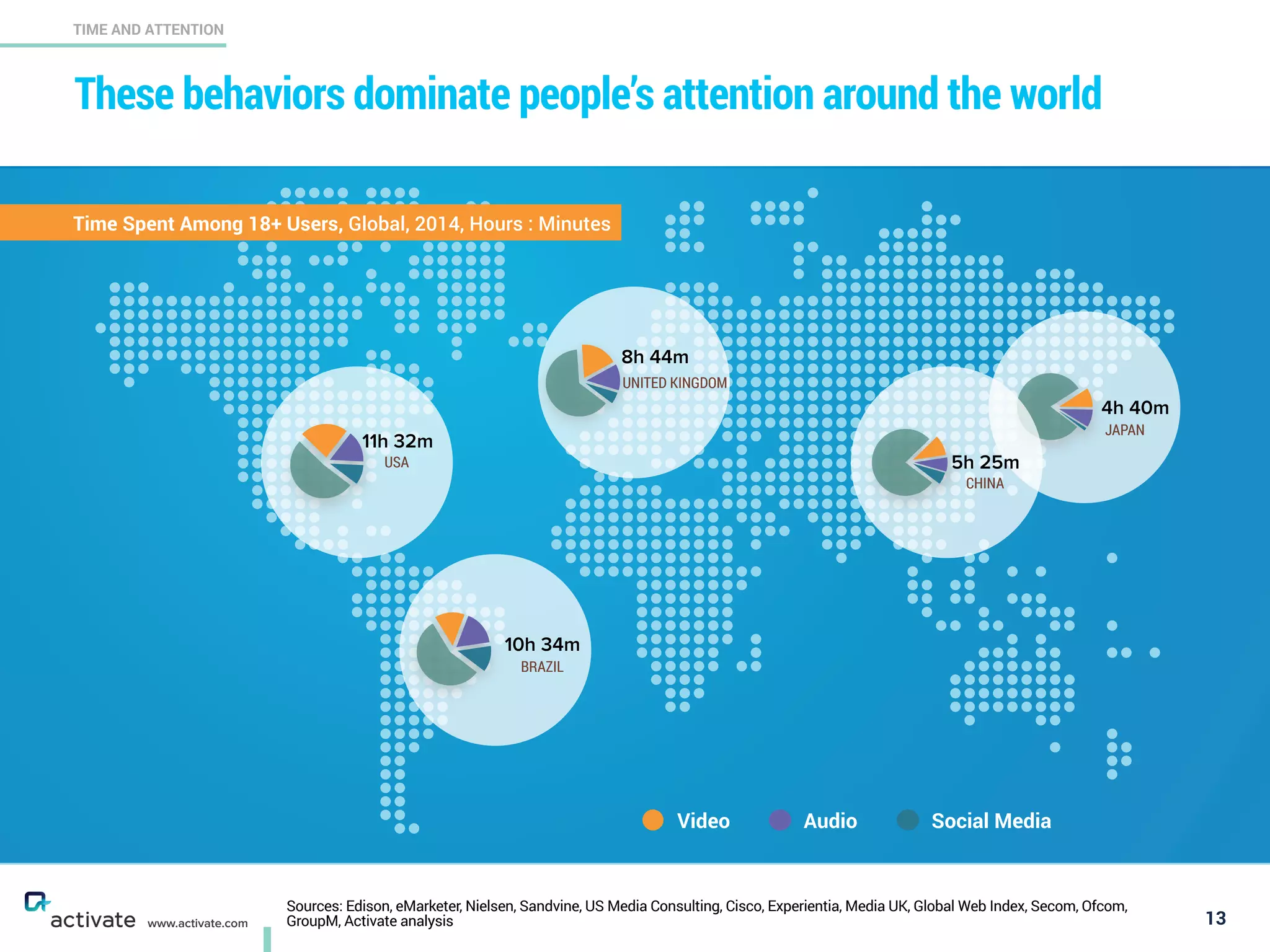

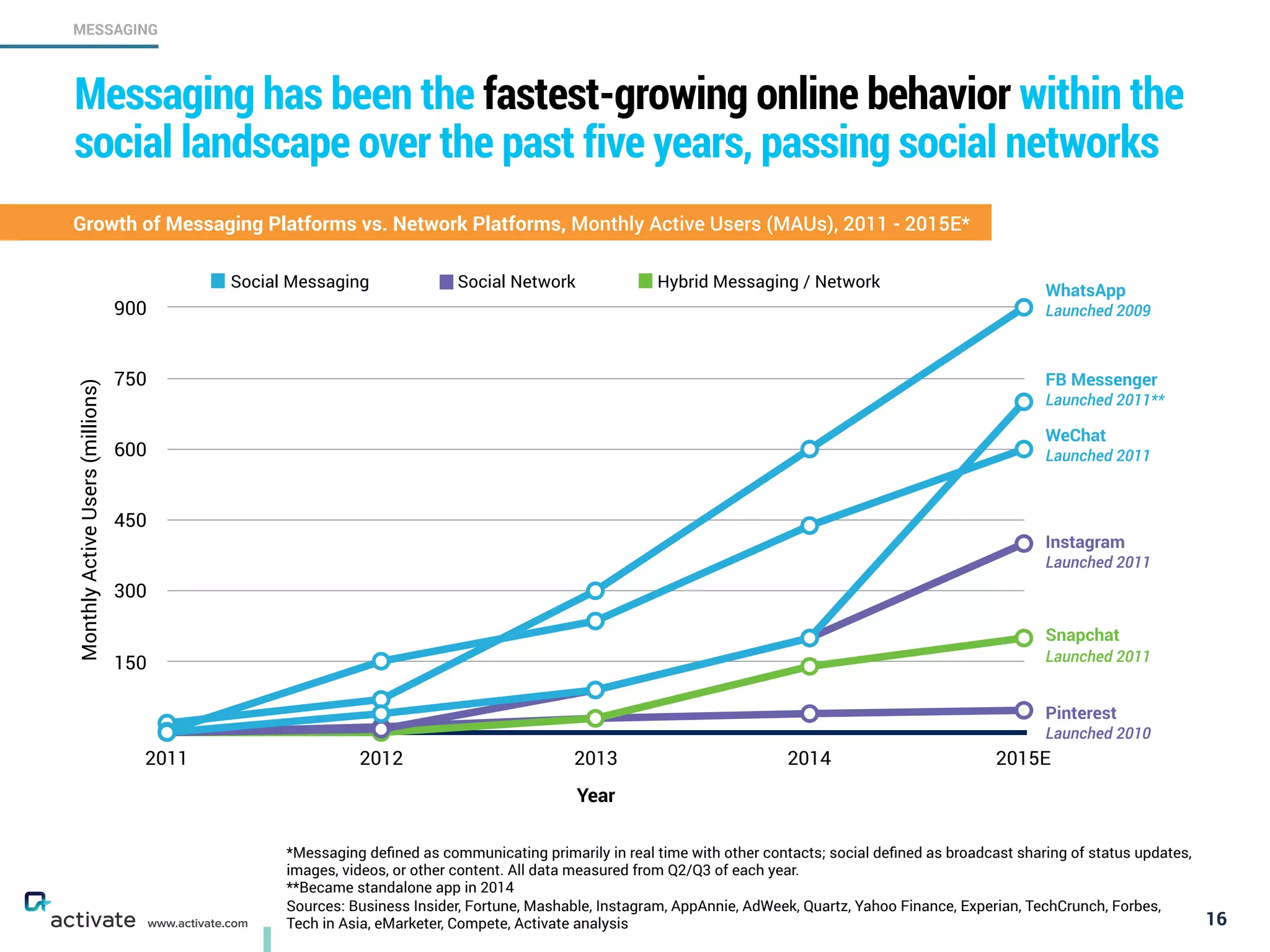

The document discusses trends in consumer tech and media from 2015-2020. It predicts that the industry will grow by over $500 billion in that time period, with the average American spending more time on tech and media than on work or sleep. It also notes that messaging platforms will surpass social networks as the dominant media activity and that the next big winners in streaming audio are already gaining popularity quietly.