Downloaded 132 times

![Understanding and Predicting Ultimate Loss-Given-Default on Bonds and Loans Michael Jacobs, Ph.D., CFA Senior Financial Economist – Credit Risk Modeling Risk Analysis Division Washington, DC 20219 Presentation to the FMA Annual Meeting 10/19/07 [email_address] The views expressed herein are solely those of the author and do not reflect necessarily the policies or procedures of the Office of the Comptroller of the Currency or of the US Department of the Treasury. Comptroller of the Currency Administrator of National Banks](https://image.slidesharecdn.com/LGDPublicationPresentation2007FMA-123575912746-phpapp02/85/Understanding-and-Predicting-Ultimate-Loss-Given-Default-on-Bonds-and-Loans-1-320.jpg)

![Understanding and Predicting Ultimate Loss-Given-Default on Bonds and Loans Michael Jacobs, Ph.D., CFA Senior Financial Economist – Credit Risk Modeling Risk Analysis Division Washington, DC 20219 Presentation to the FMA Annual Meeting 10/19/07 [email_address] The views expressed herein are solely those of the author and do not reflect necessarily the policies or procedures of the Office of the Comptroller of the Currency or of the US Department of the Treasury. Comptroller of the Currency Administrator of National Banks](https://image.slidesharecdn.com/LGDPublicationPresentation2007FMA-123575912746-phpapp02/75/Understanding-and-Predicting-Ultimate-Loss-Given-Default-on-Bonds-and-Loans-1-2048.jpg)

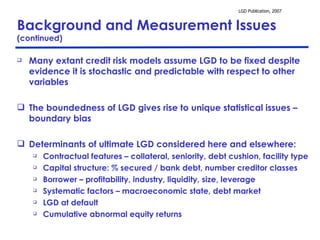

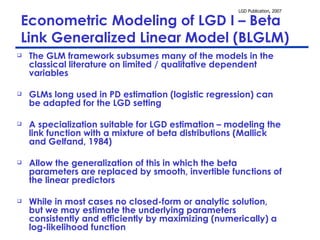

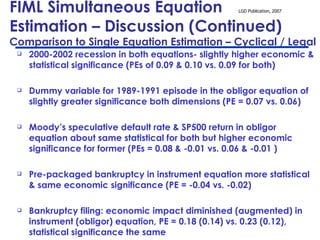

![Econometric Modeling of LGD III – Beta Kernel Conditional Density Estimation (BKDE) Standard non-parametric estimators of unknown probability distribution functions typically utilize the Gaussian kernel Boundary bias problem: assigns non-zero density outside the support on dependent variable when smoothing near boundary. Chen (1999): beta kernel density estimator (BKDE) on [0,1] Properties: flexible functional form, bounded support, tractability, non-negativity & finite sample optimal convergence rate Even if true density is unbounded at boundaries BKDE is consistent We extend the BKDE to a generalized BKDE (GBKDE): density a function of several variables affecting the smoothing Independent kernel & smoothing parameter in each dimension](https://image.slidesharecdn.com/LGDPublicationPresentation2007FMA-123575912746-phpapp02/85/Understanding-and-Predicting-Ultimate-Loss-Given-Default-on-Bonds-and-Loans-14-320.jpg)

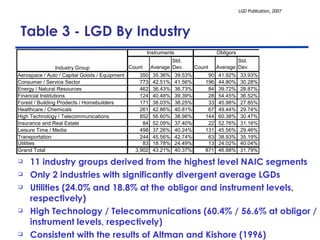

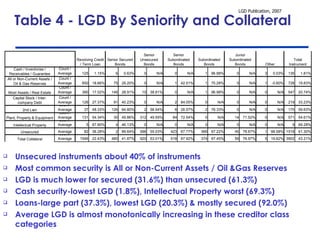

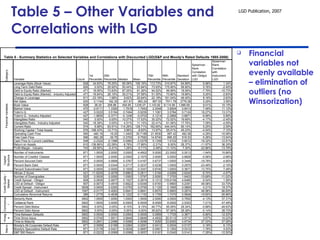

The document summarizes research on modeling and predicting ultimate loss-given-default (LGD) on bonds and loans. It discusses issues in LGD measurement, reviews theoretical and empirical credit risk models, and presents alternative econometric models to estimate LGD including a beta link generalized linear model. The research finds leverage, profitability, and market factors are associated with lower LGD, while contractual features like seniority and collateral impact LGD. Modeling LGD at both the obligor and instrument level improves performance.

![Lgd Model Jacobs 10 10 V2[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lgdmodeljacobs1010v21-12872530142448-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)