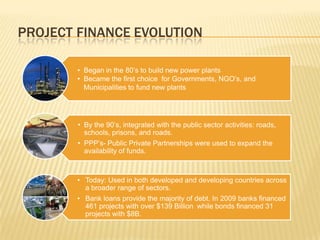

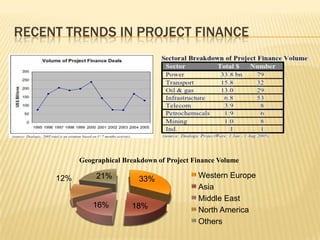

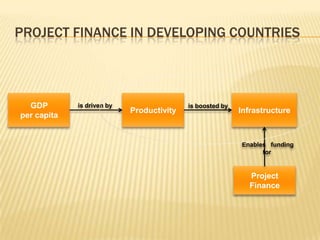

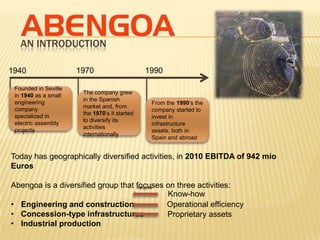

The document provides an overview of project finance, detailing its structure, risks, and comparisons with corporate finance. It discusses the evolution of project finance since the 1980s, including its application in various sectors and offers case studies such as the Dabhol power project and Abengoa, illustrating the complexities and lessons learned in managing risks and financing strategies. The analysis emphasizes the importance of organizational structure, contractual frameworks, and the impact of leverage on financial performance.