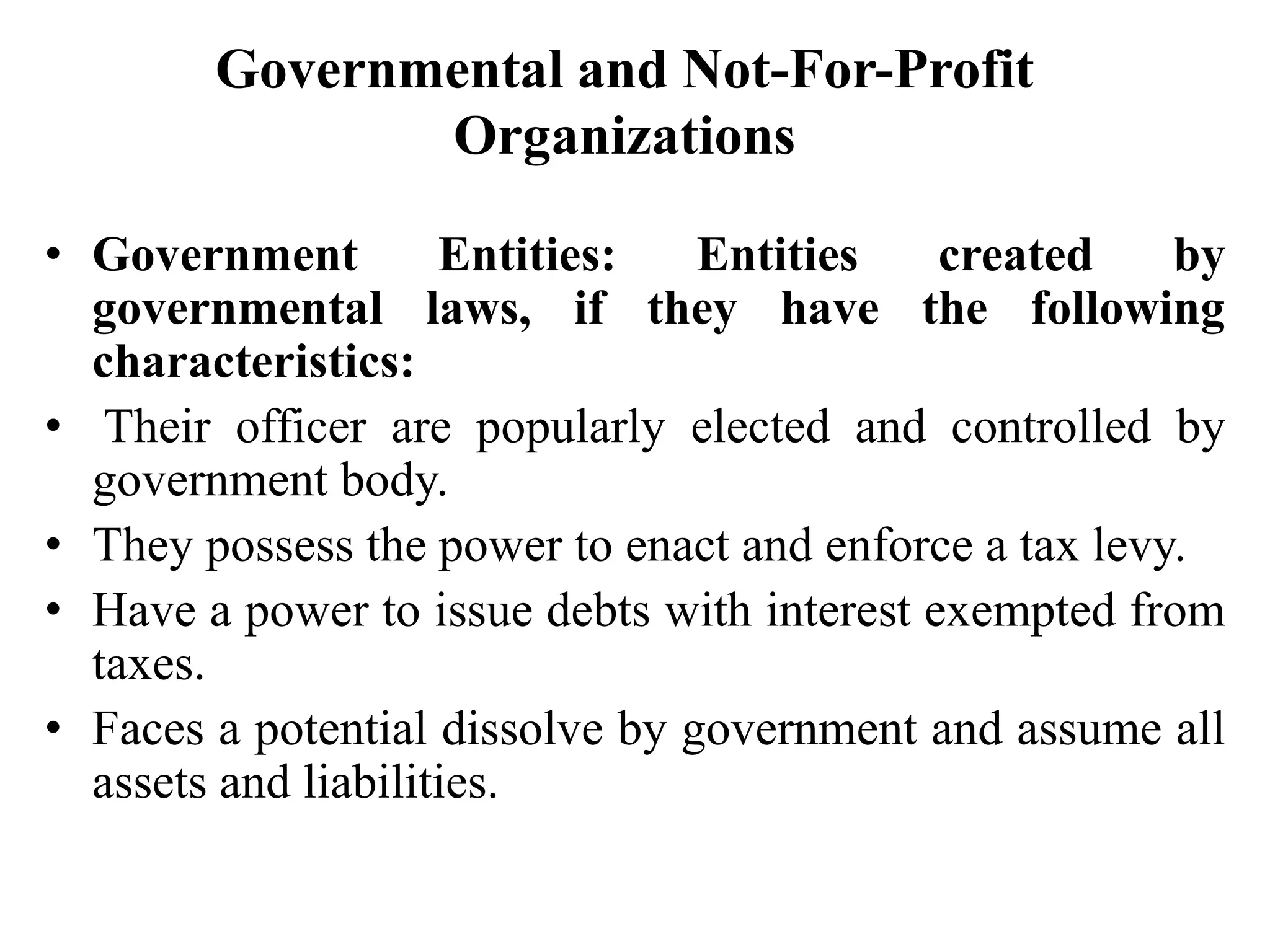

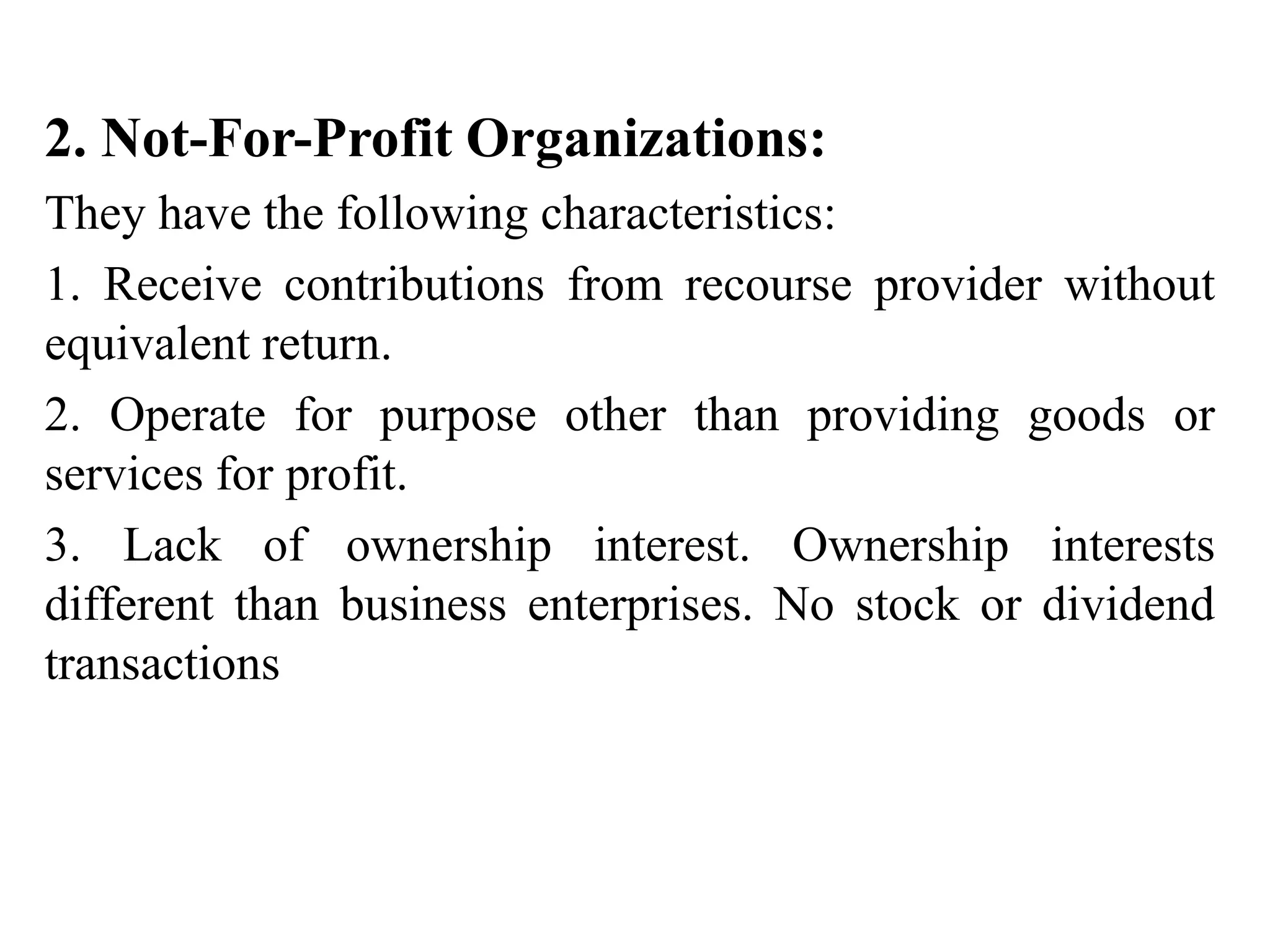

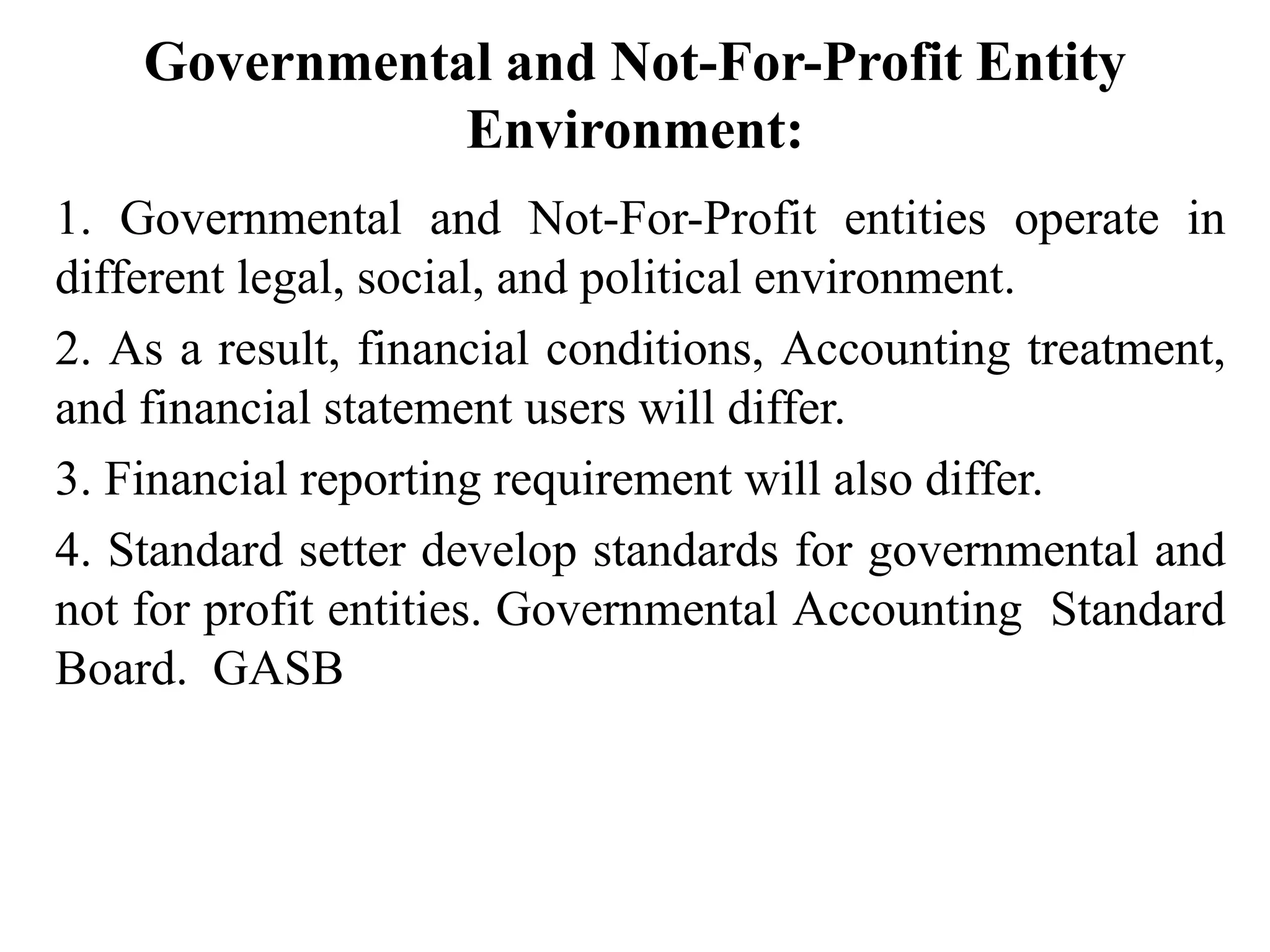

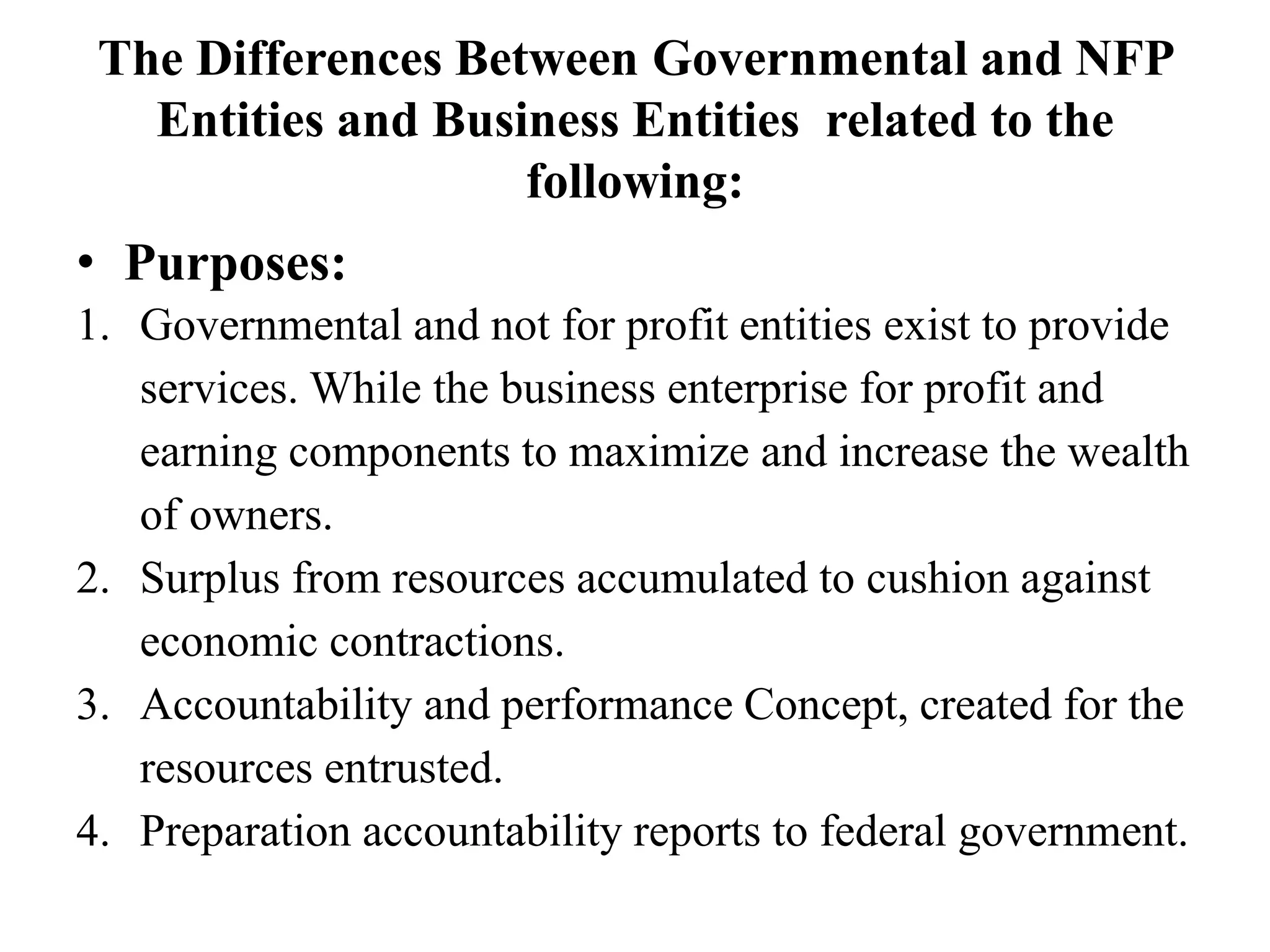

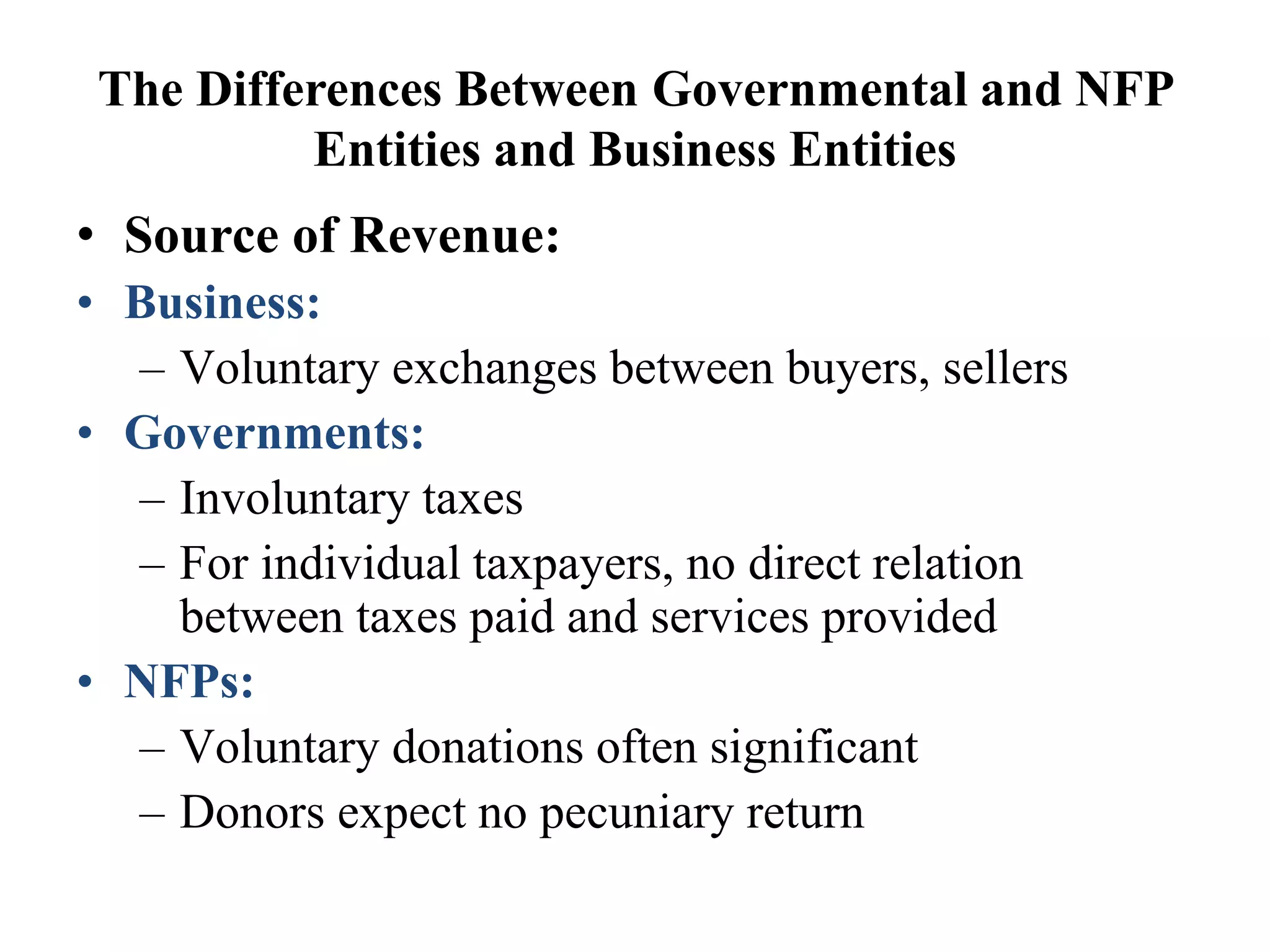

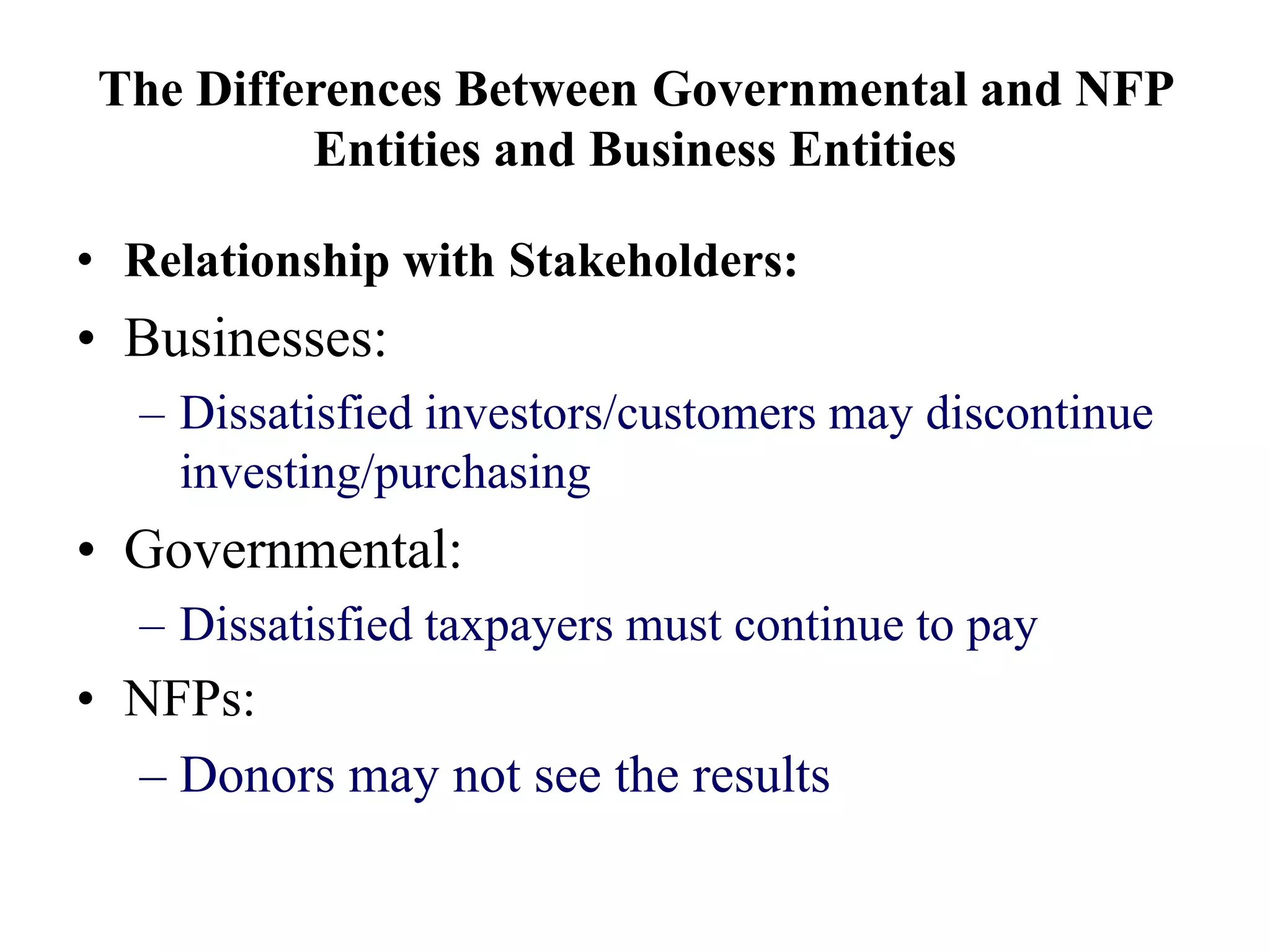

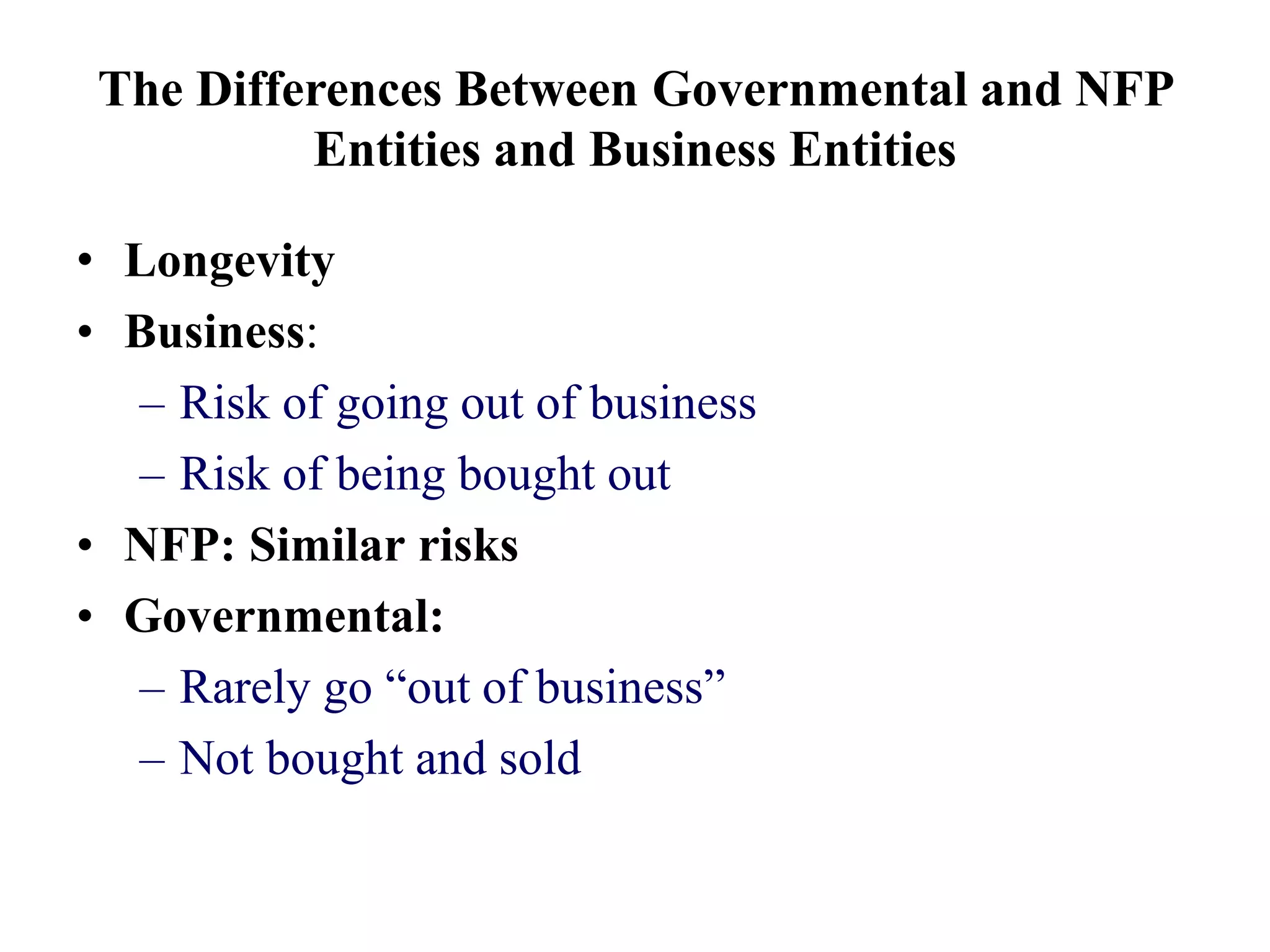

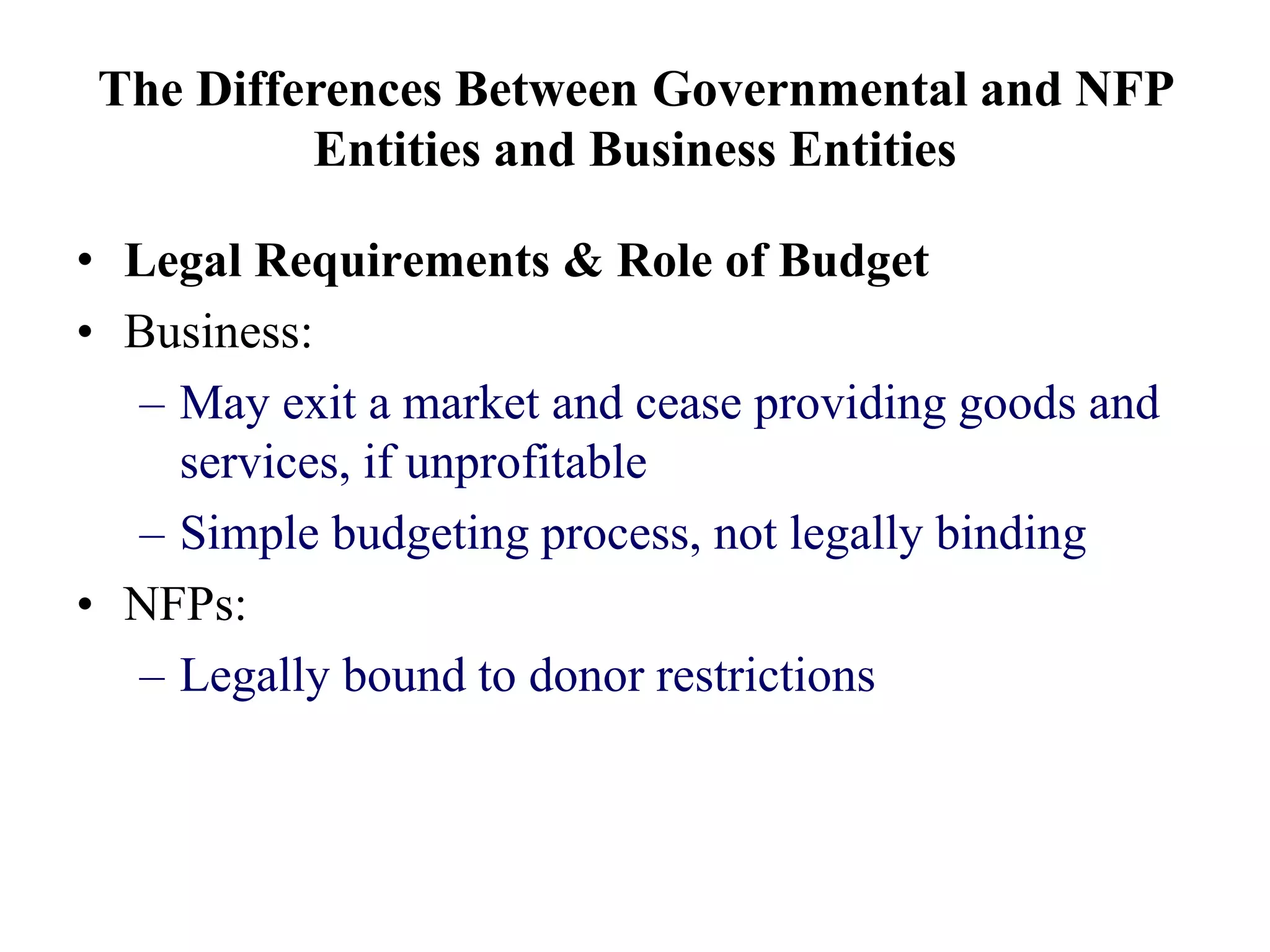

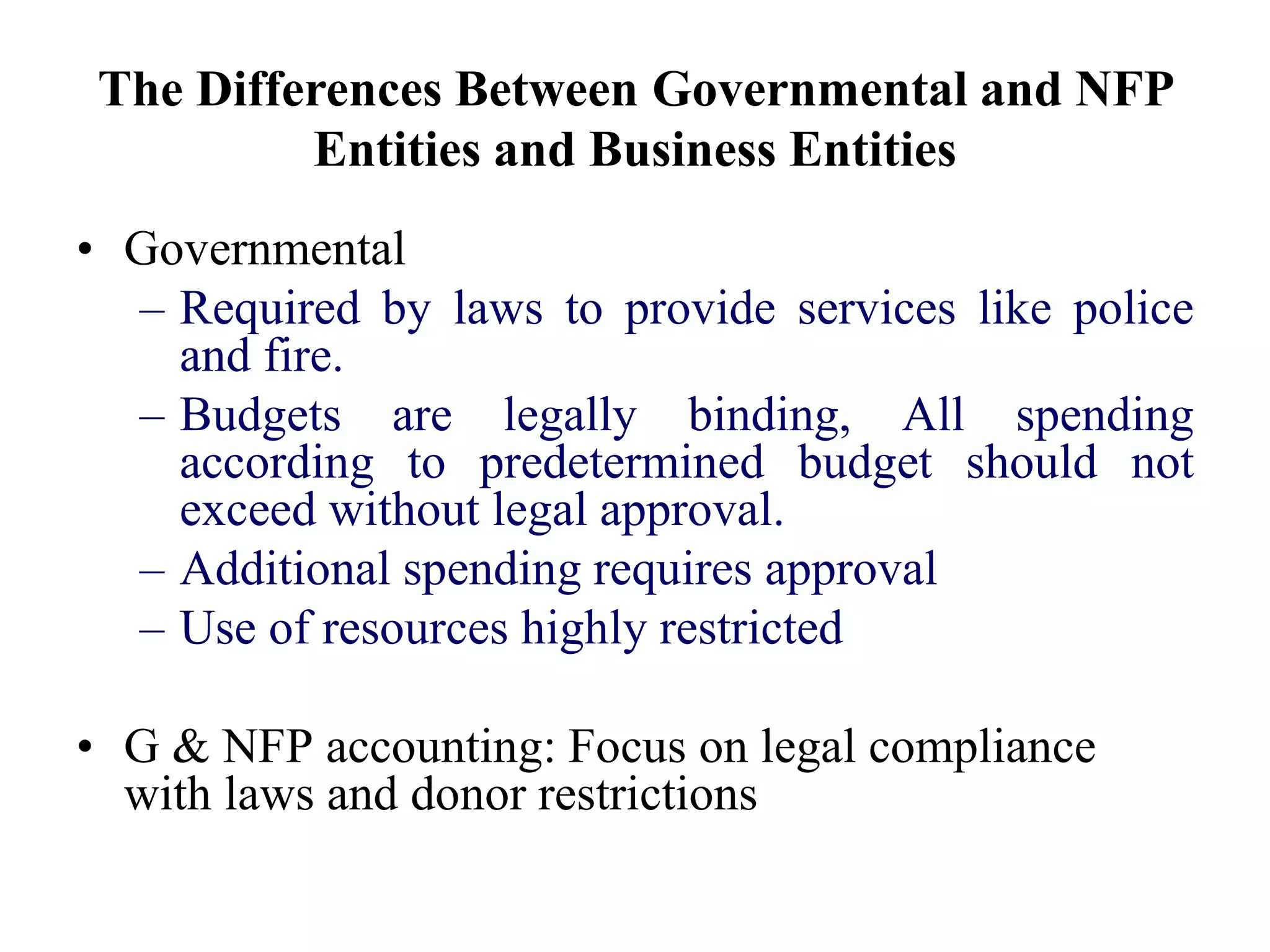

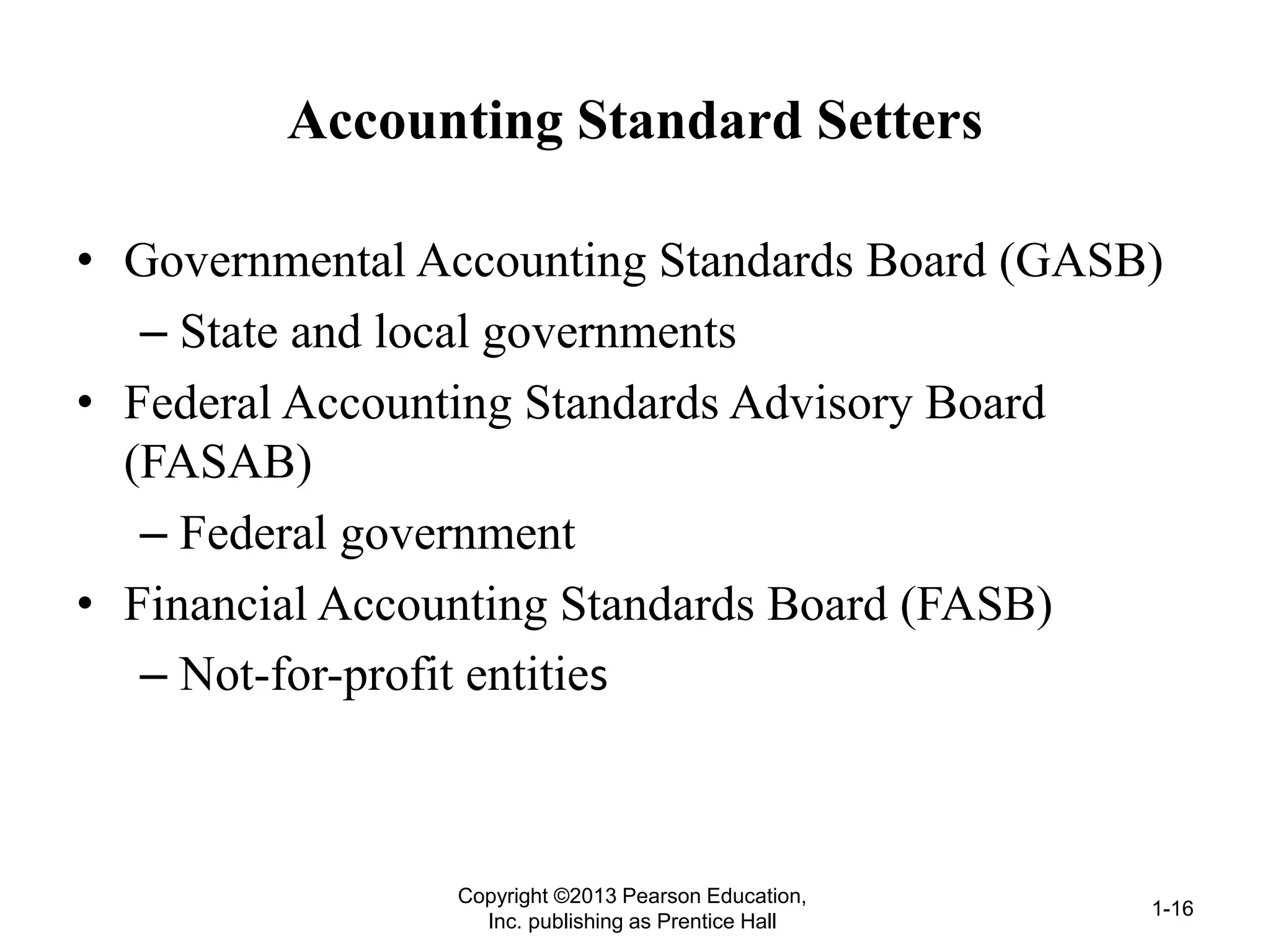

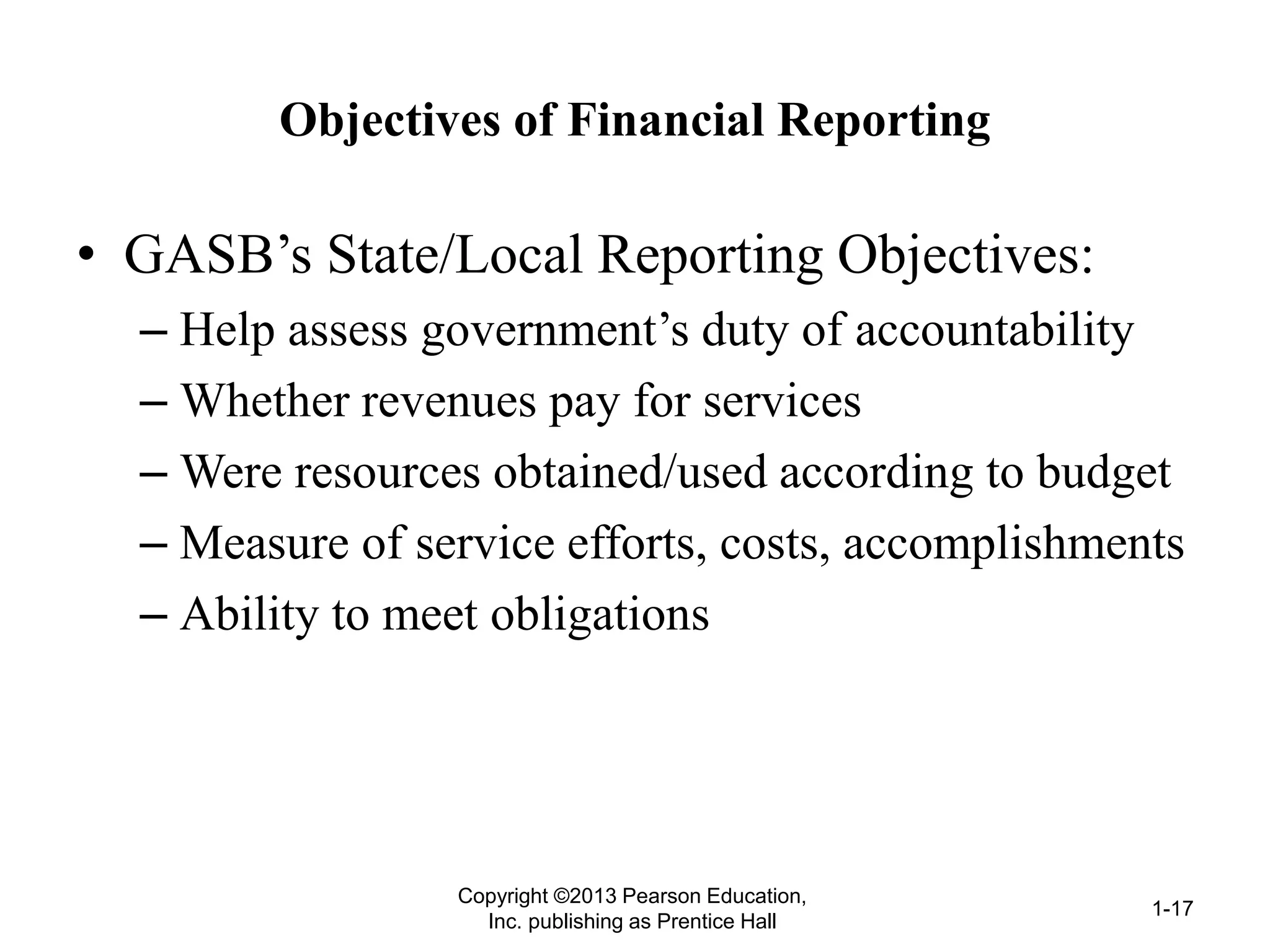

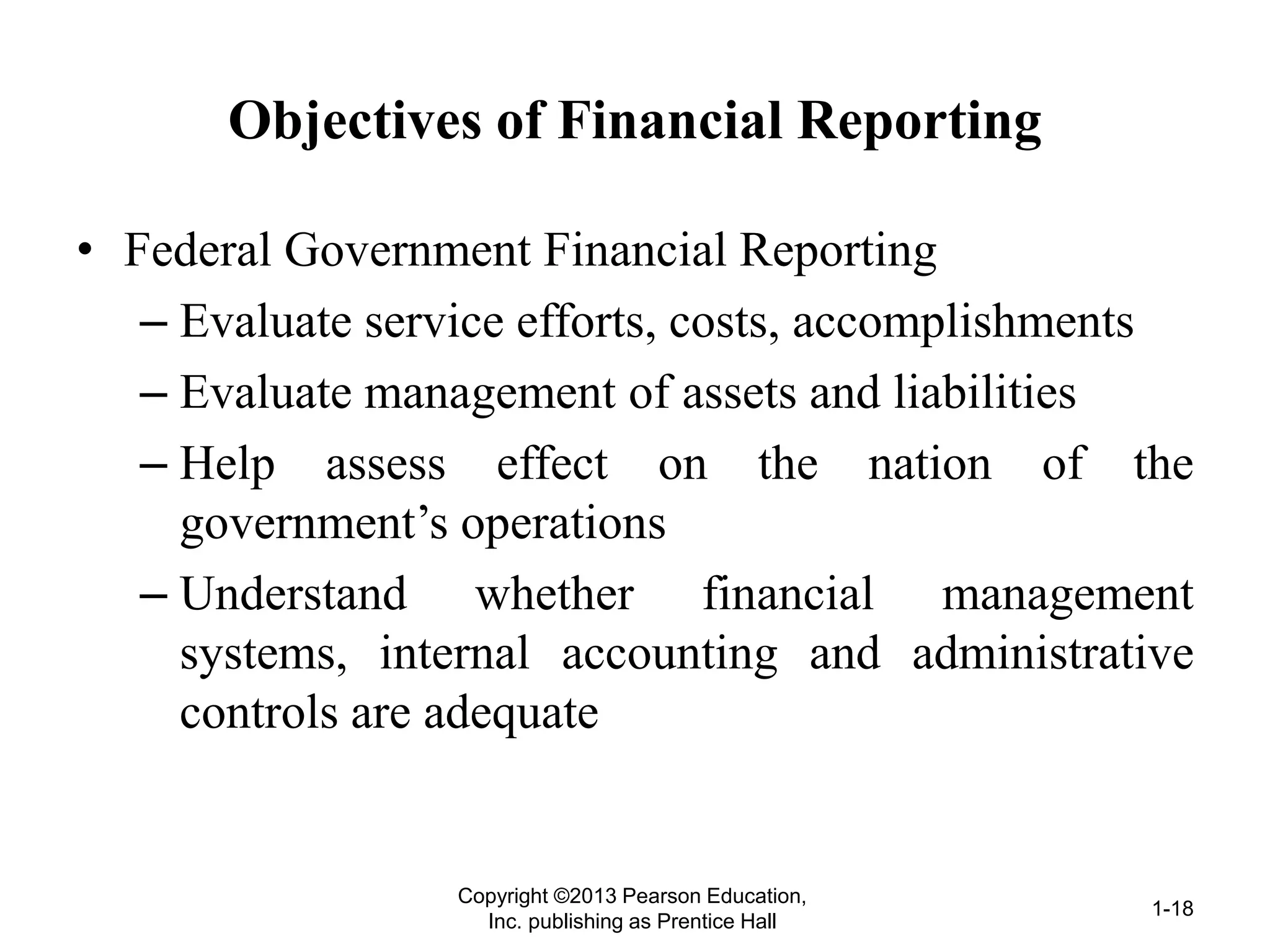

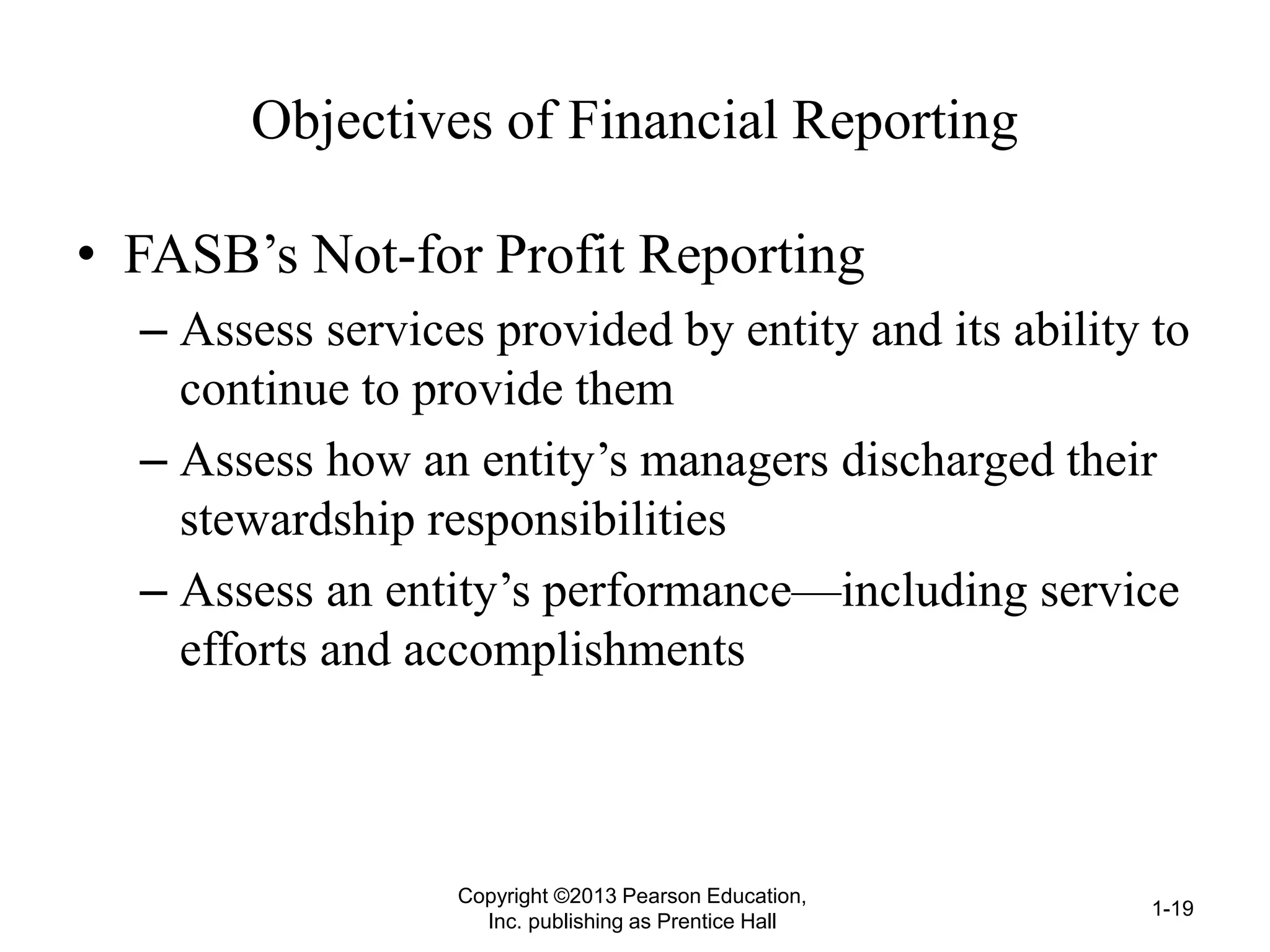

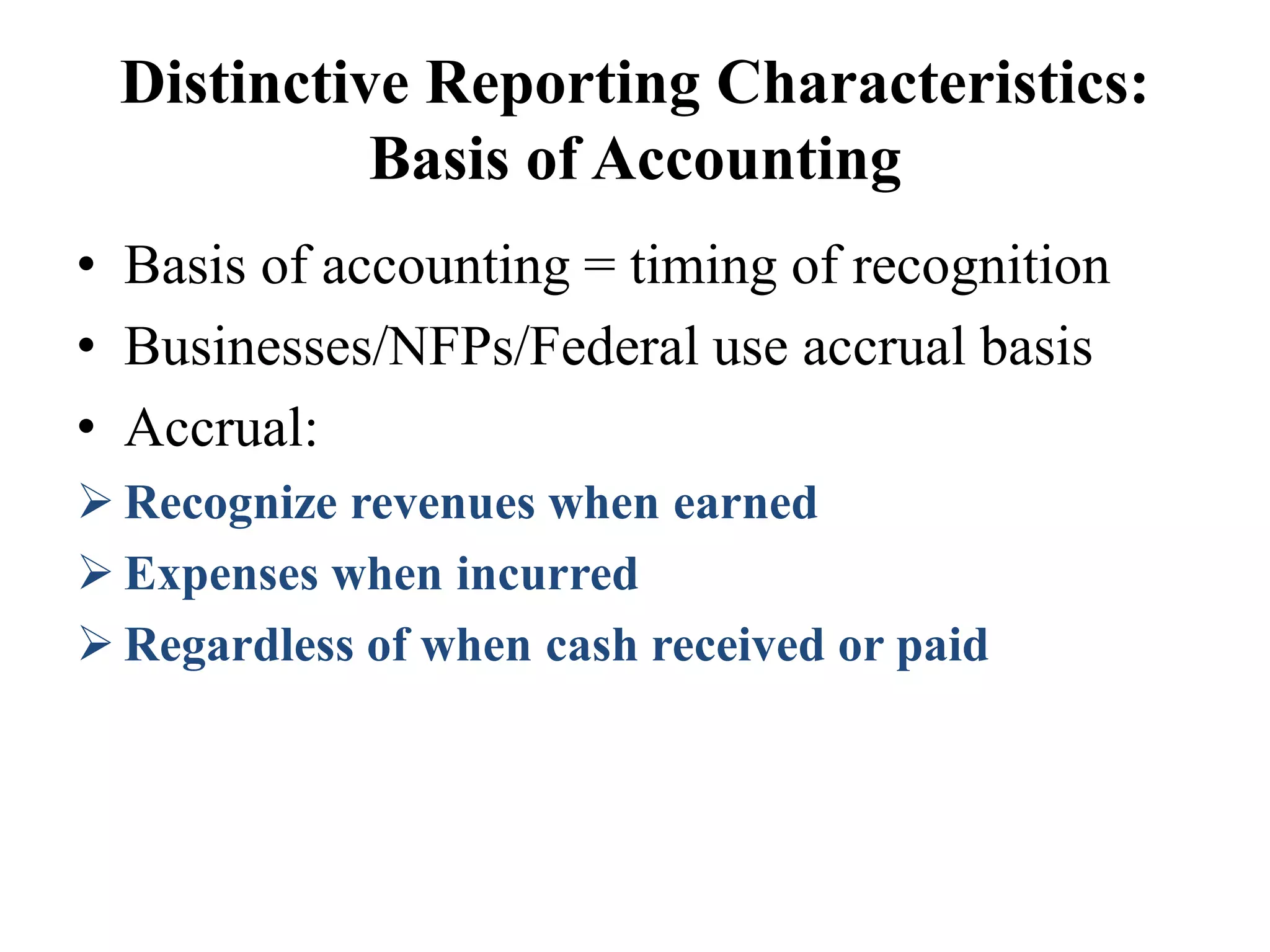

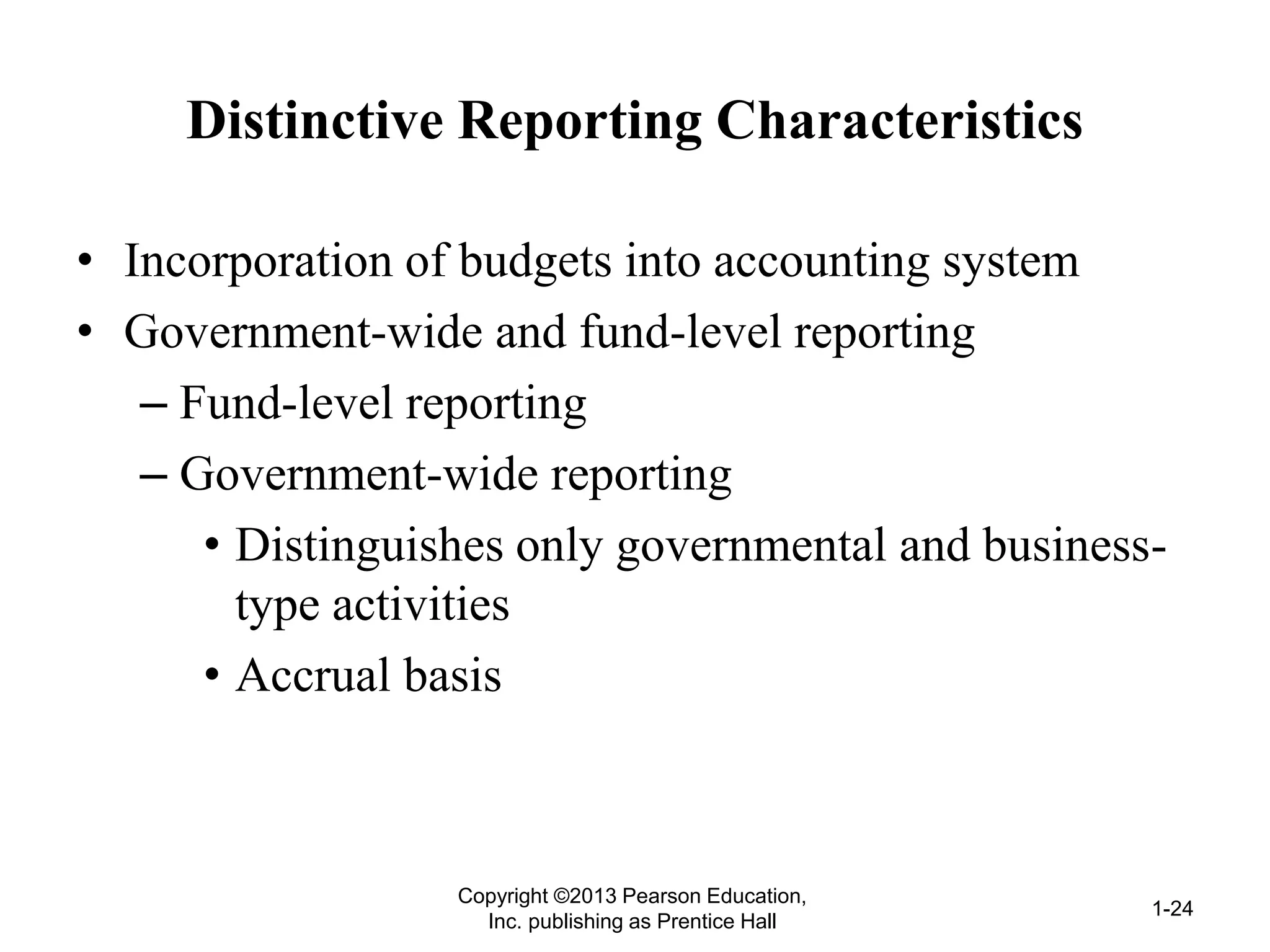

This document discusses the key differences between governmental/not-for-profit (NFP) entities and business enterprises. Governmental and NFP entities operate under different legal and financial constraints compared to businesses. They rely on involuntary taxes and voluntary donations rather than sales. Budgets are legally binding for governments and donor restrictions apply to NFPs. Financial reporting focuses on accountability, compliance with budgets/restrictions, and measuring service efforts rather than profitability. Fund accounting and modified accrual basis are used by governments.