Download to read offline

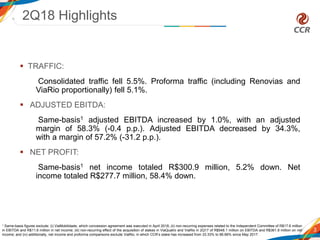

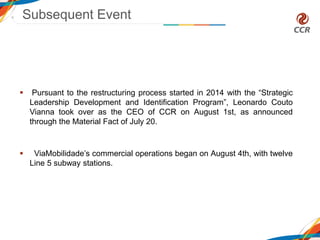

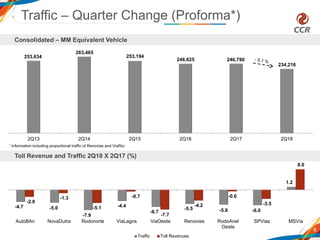

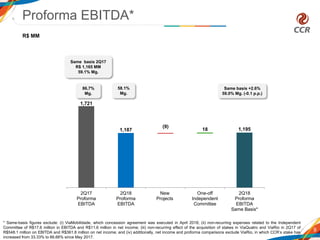

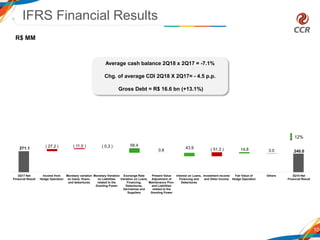

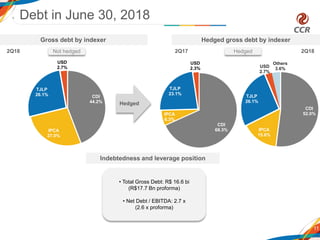

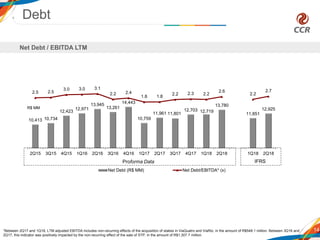

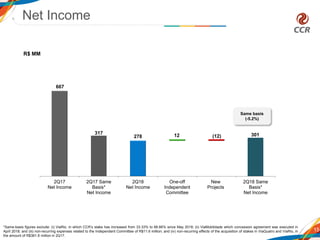

- Consolidated traffic fell 5.5% in 2Q18 compared to 2Q17. Adjusted EBITDA on a same-basis increased 1.0% to R$1,091.7 million, with a margin of 58.3% (-0.4 p.p.). Net income on a same-basis totaled R$300.9 million, down 5.2%. - Leonardo Couto Vianna took over as CEO of CCR on August 1, 2018. ViaMobilidade's commercial operations began on August 4, 2018. - Gross debt totaled R$16.6 billion as of June 30, 2018, with an average cost of debt of C