Download as PDF, PPTX

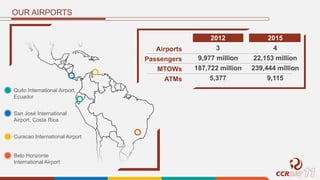

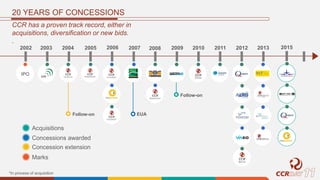

The document summarizes a presentation given by CCR, a Brazilian infrastructure company, about their current business and future outlook. It provides an overview of various transportation projects CCR is involved in, including highways, urban rail, and airports in Brazil and other countries. Updates are given on key performance metrics and investments made in projects like ViaQuatro, CCR Metro Bahia, CCR NovaDutra, CCR MSVia, and VLT Carioca. The presentation indicates that the business environment for infrastructure is promising in Brazil and that CCR has a track record of successful investments and expansion into new projects.