Download as PDF, PPTX

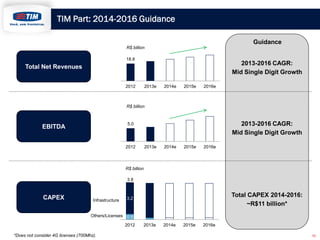

The document discusses TIM Participações' industrial plan for 2014-2016. It begins with statements regarding forward-looking projections and uncertainties. It then provides an overview of TIM's 2013 year-to-date financial and operational results, noting consistent performance despite a changing macroeconomic scenario in Brazil. Finally, it outlines TIM's strategic positioning and opportunities in the mobile and fixed markets in Brazil, and provides guidance for total revenues, EBITDA, and CAPEX from 2013-2016.