Download to read offline

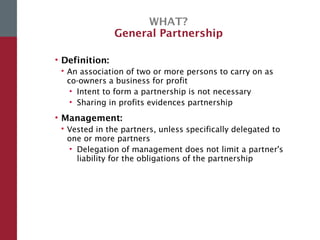

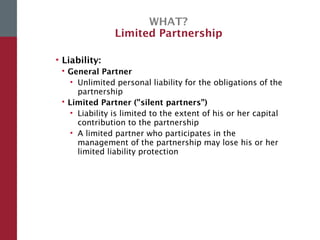

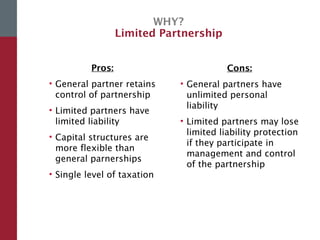

![WHAT?

Limited Partnership

• Definition:

A partnership comprising

• one or more general partners who manage [the]

business and who are personally liable for

partnership debts, and

• one or more limited partners who contribute capital

and share in profits but who take no part in running

[the] business and incur no liability with respect to

partnership obligations beyond contribution](https://image.slidesharecdn.com/2015-11-4wsucorpstructureformationforstart-ups-170204050244/85/2015-11-4_WSU_Defining-a-Corporate-Structure-for-a-Startup-Company-15-320.jpg)

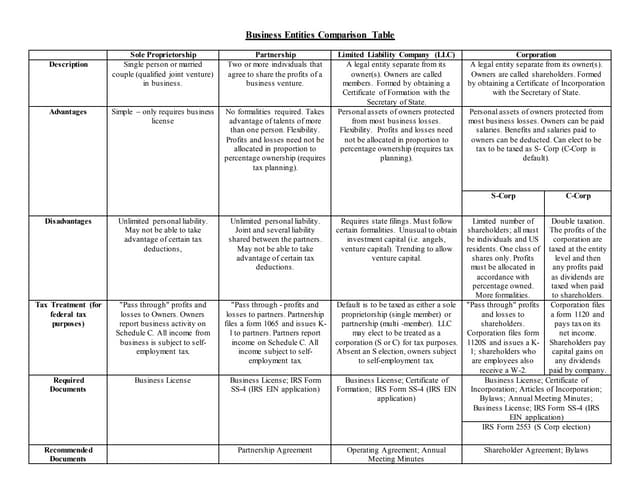

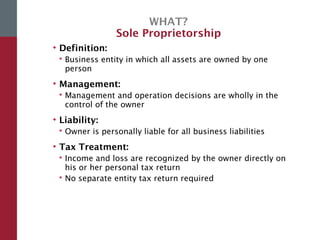

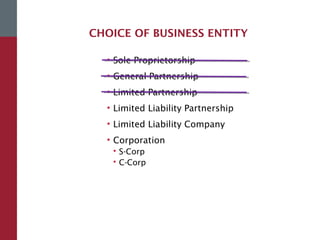

The document provides a comprehensive overview of corporate structures for start-ups, detailing various business entities such as sole proprietorships, partnerships, LLCs, and corporations (S and C). It discusses the advantages and disadvantages of each entity type, formation processes, tax treatments, and liability considerations, emphasizing the importance of a well-defined corporate structure for attracting investors. Key factors to consider when choosing a business entity are also outlined, including financing methods and flexibility in ownership and capital structure.