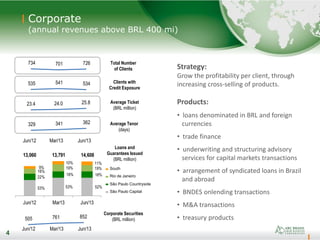

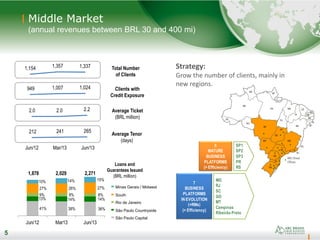

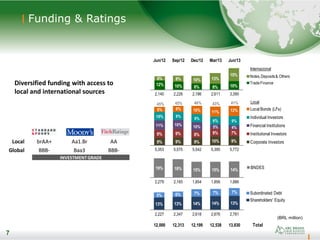

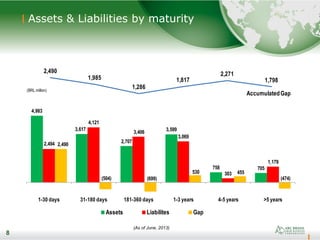

This document provides an investor presentation for Banco ABC Brasil covering their strategy, business segments, funding and capital base, and financial highlights. It summarizes that Banco ABC Brasil focuses on providing commercial banking services to large corporate and middle-market clients in Brazil. Their strategy is to increase profitability per large corporate client through cross-selling more products, and grow their middle-market client base. They have a diversified funding base and strong capital and financial ratios.