Downloaded 301 times

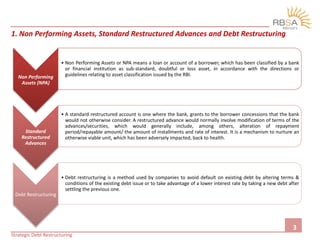

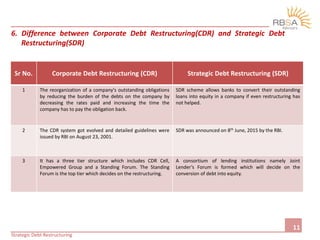

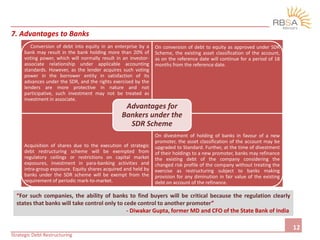

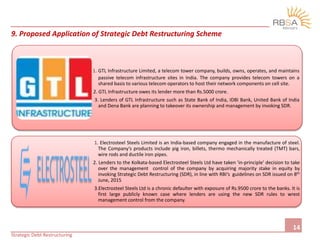

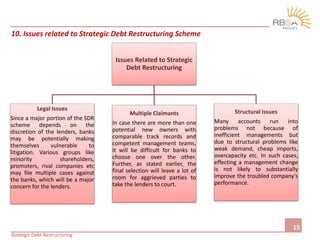

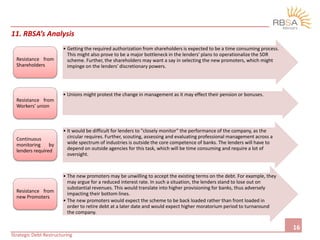

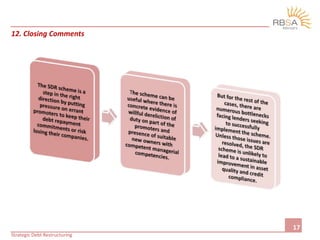

The document discusses strategic debt restructuring, a method introduced by the Reserve Bank of India to help banks recover loans from distressed listed companies. Under the strategic debt restructuring scheme, a consortium of lenders known as the Joint Lenders Forum can convert outstanding debts into equity shares, allowing them to acquire a majority ownership stake in the company, if the company fails to meet milestones in its restructuring package. The scheme is intended to revive stressed companies and provide an alternative to debt restructuring. Key aspects include eligibility criteria for lenders and companies, the debt conversion process, and requirements for the lenders to divest their stake within 18 months.

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)

![Hacking-Uncovered-How-People-Get-Hacked-and-How-to-Stay-Safe[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/hacking-uncovered-how-people-get-hacked-and-how-to-stay-safe1-260130170011-4883a9c7-thumbnail.jpg?width=640&height=640&fit=bounds)