Download as PPSX, PPTX

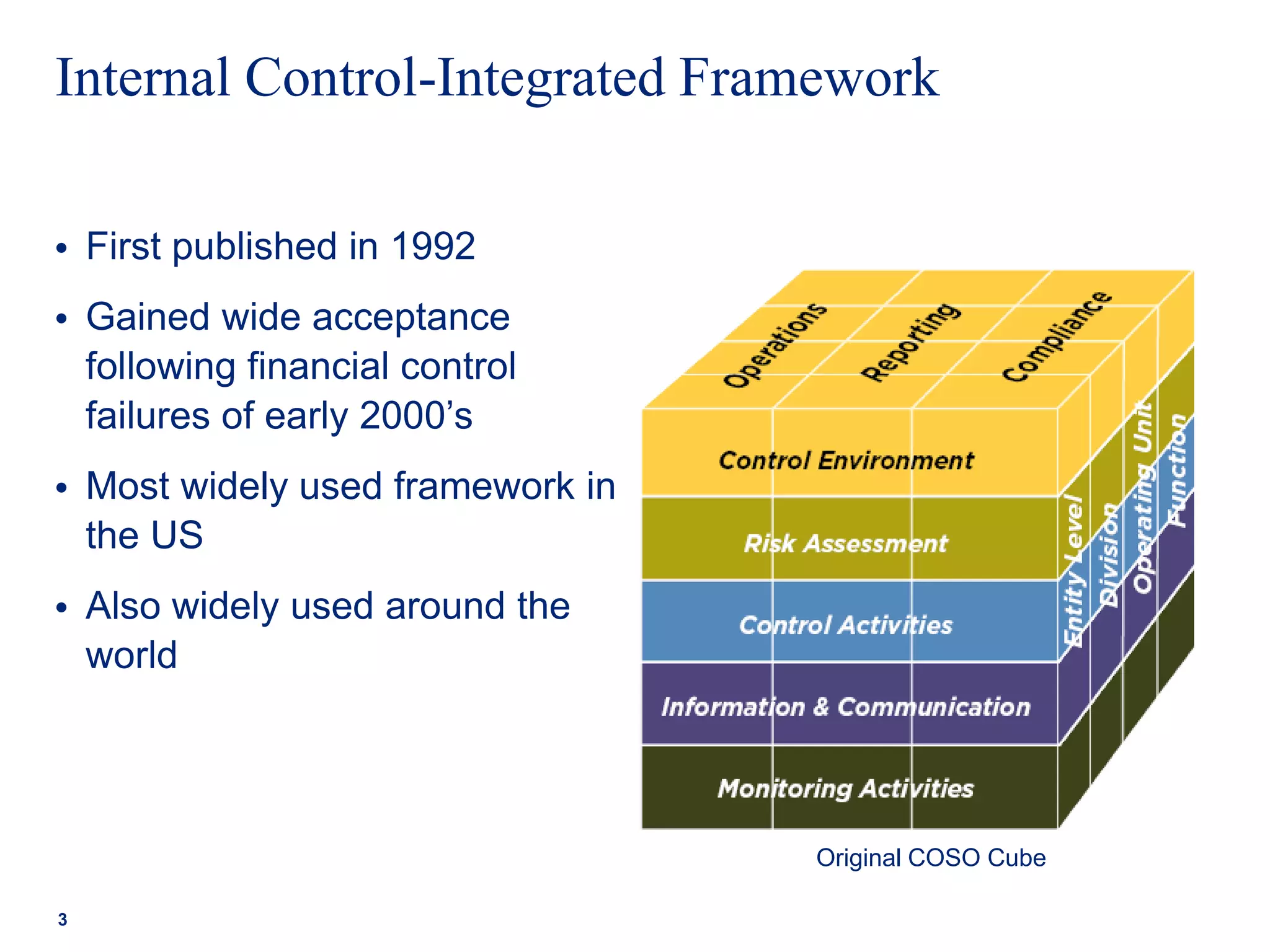

The document discusses the COSO internal control framework. It provides background on COSO, describing it as a joint initiative to provide guidance on internal controls. The framework was first published in 1992 and provides principles and attributes for internal controls relating to control environment, risk assessment, control activities, information/communication, and monitoring. It discusses changes in the updated framework to make it more relevant to today's business environment. Key changes include clarifying the role of objective setting, reflecting the increased relevance of technology, and enhancing governance concepts.

Introduction to COSO and its framework for internal control, highlighting its history and widespread acceptance.

Details on the methodology behind updating the internal control framework, emphasizing clarity, technology relevance, and anti-fraud considerations.

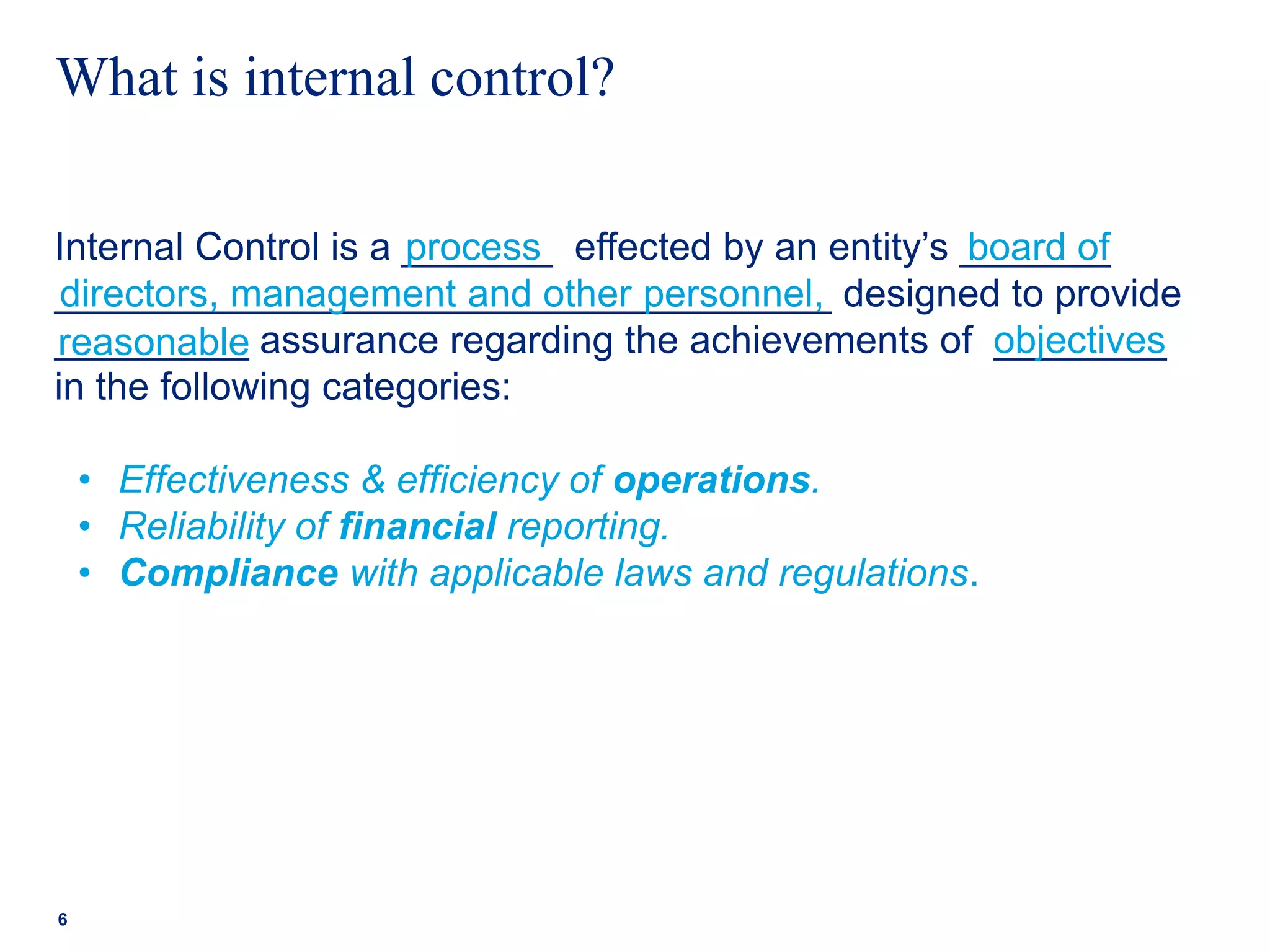

Definition of internal control and its objectives, including operational efficiency, financial reporting, and compliance.

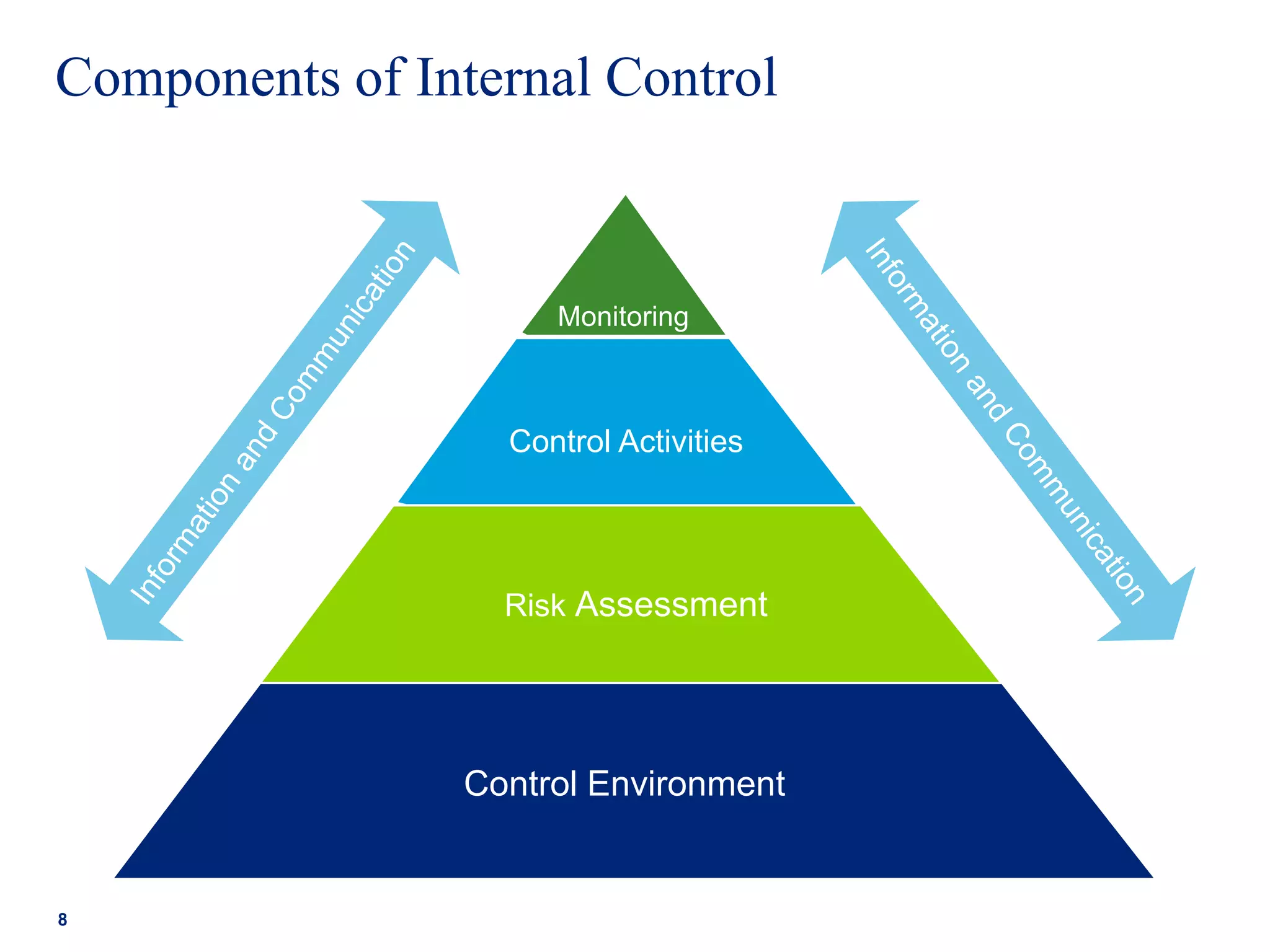

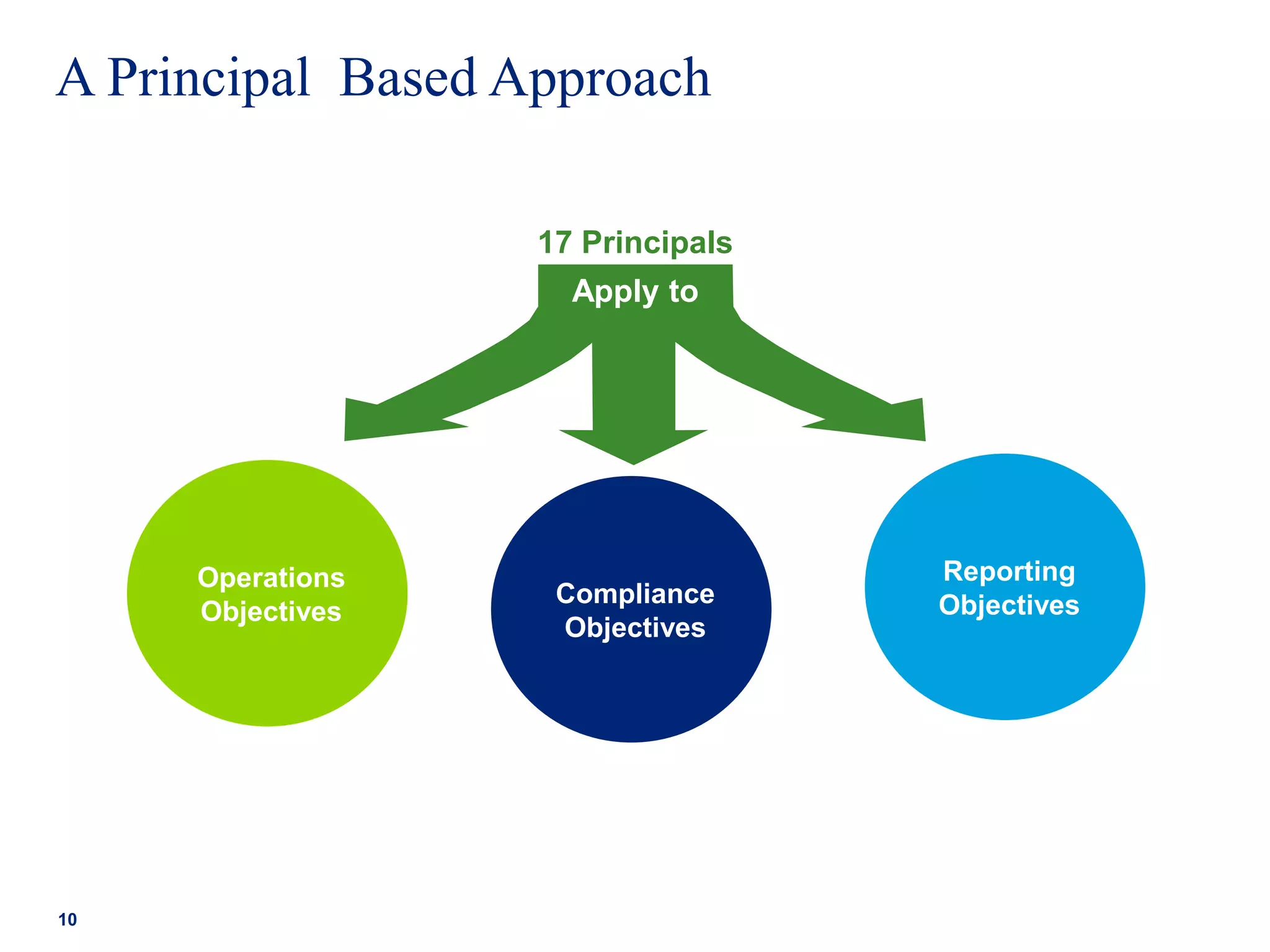

Outlines the five components of internal control and their significance in ensuring effective governance.

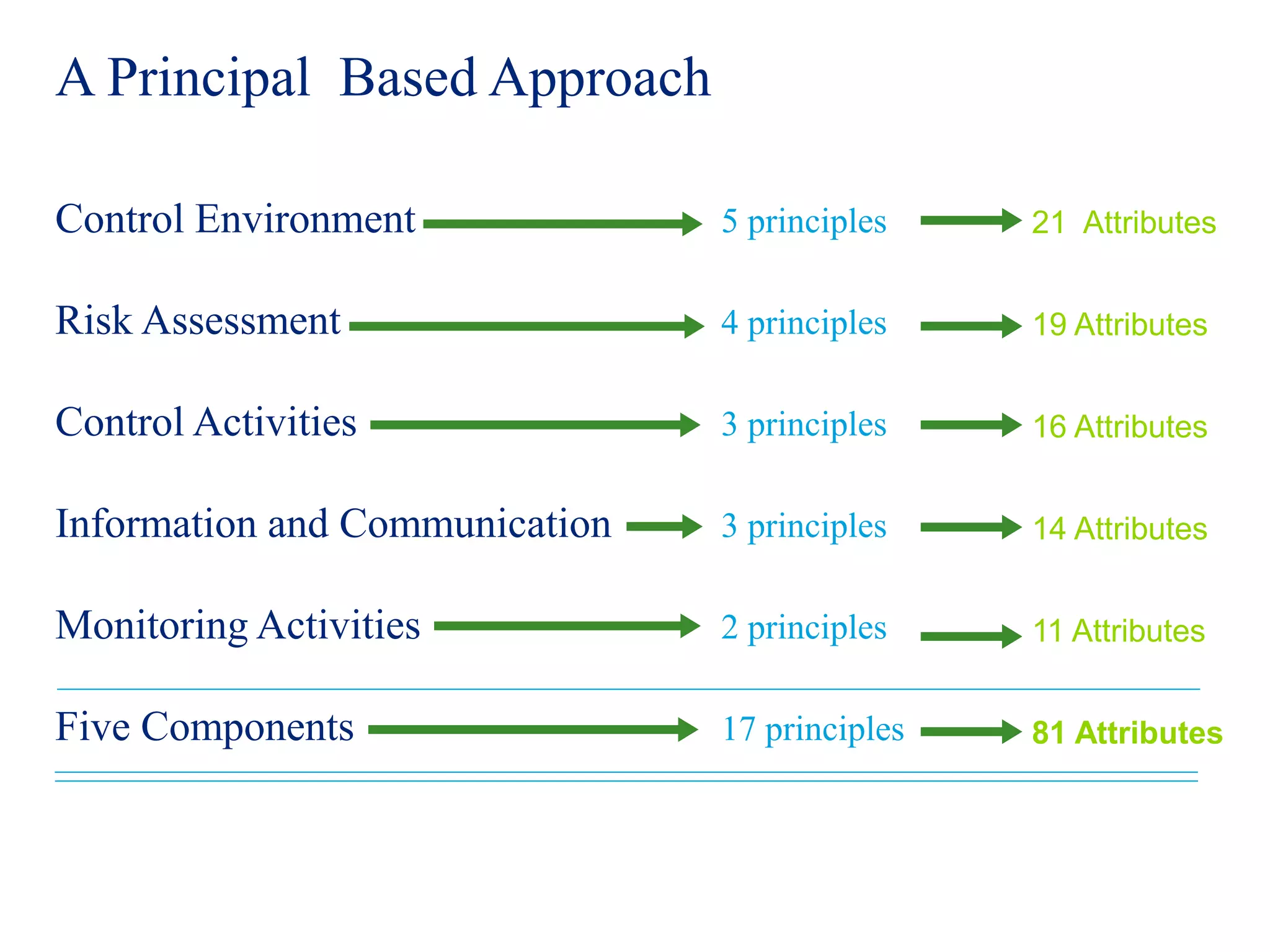

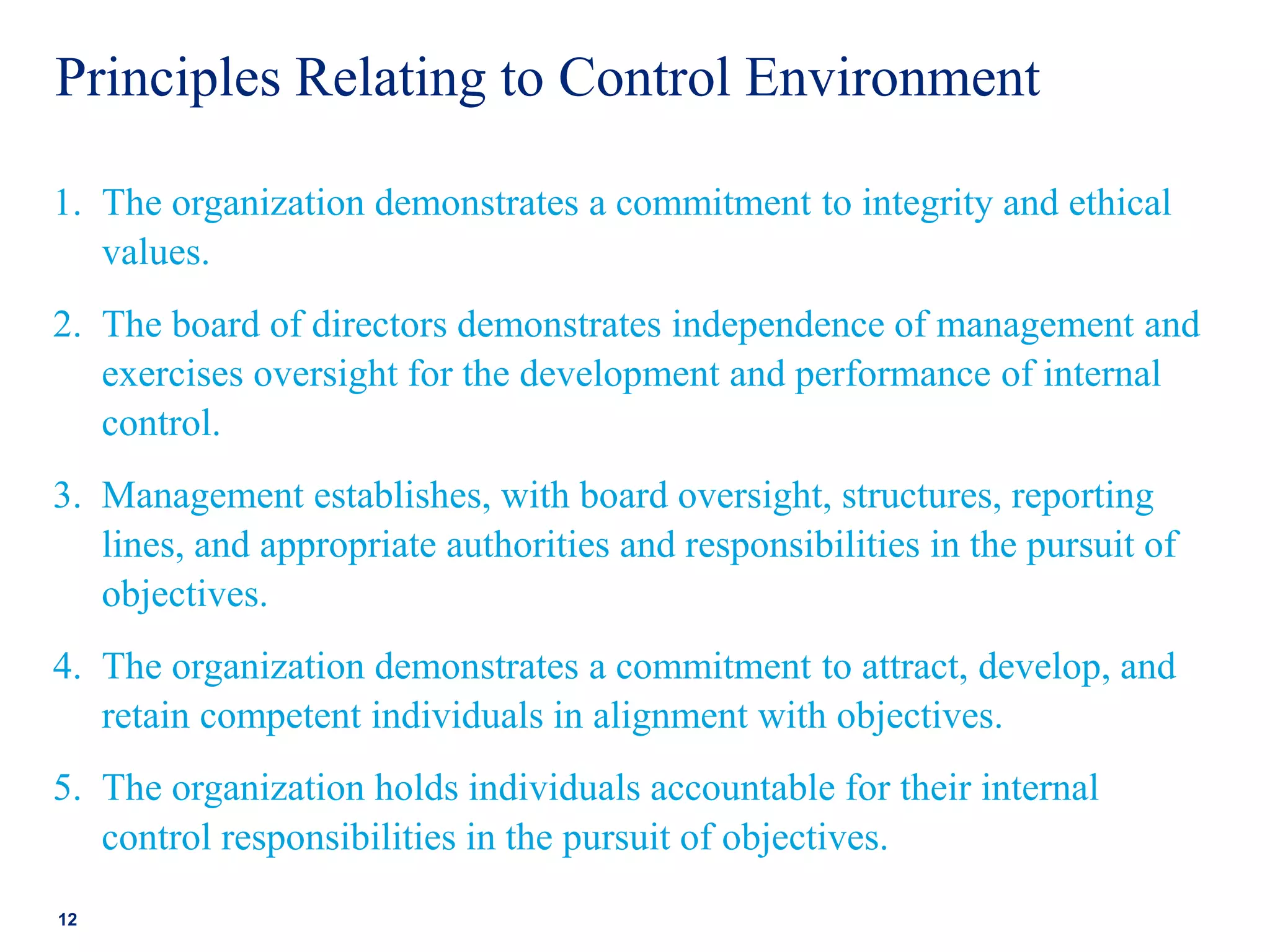

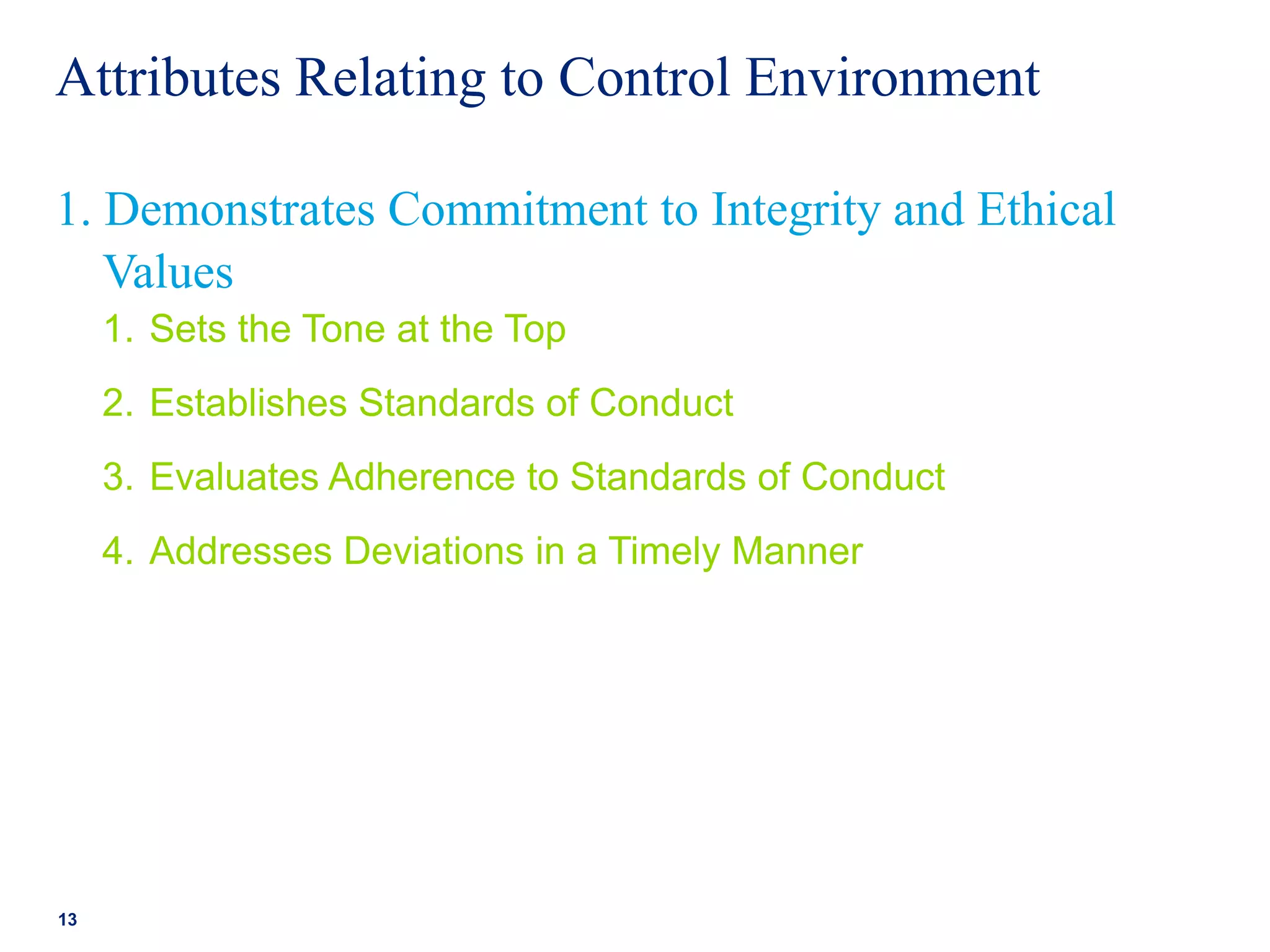

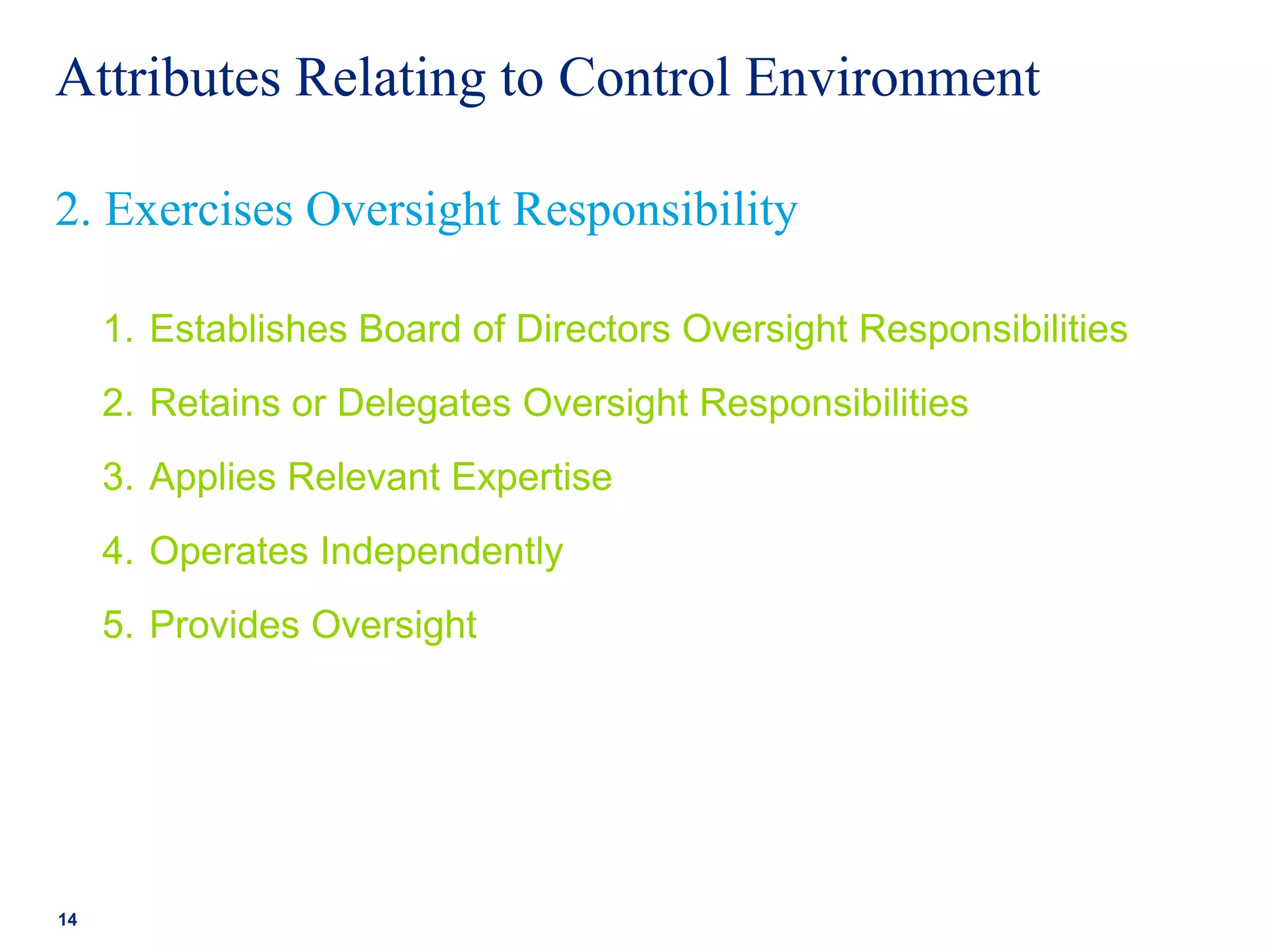

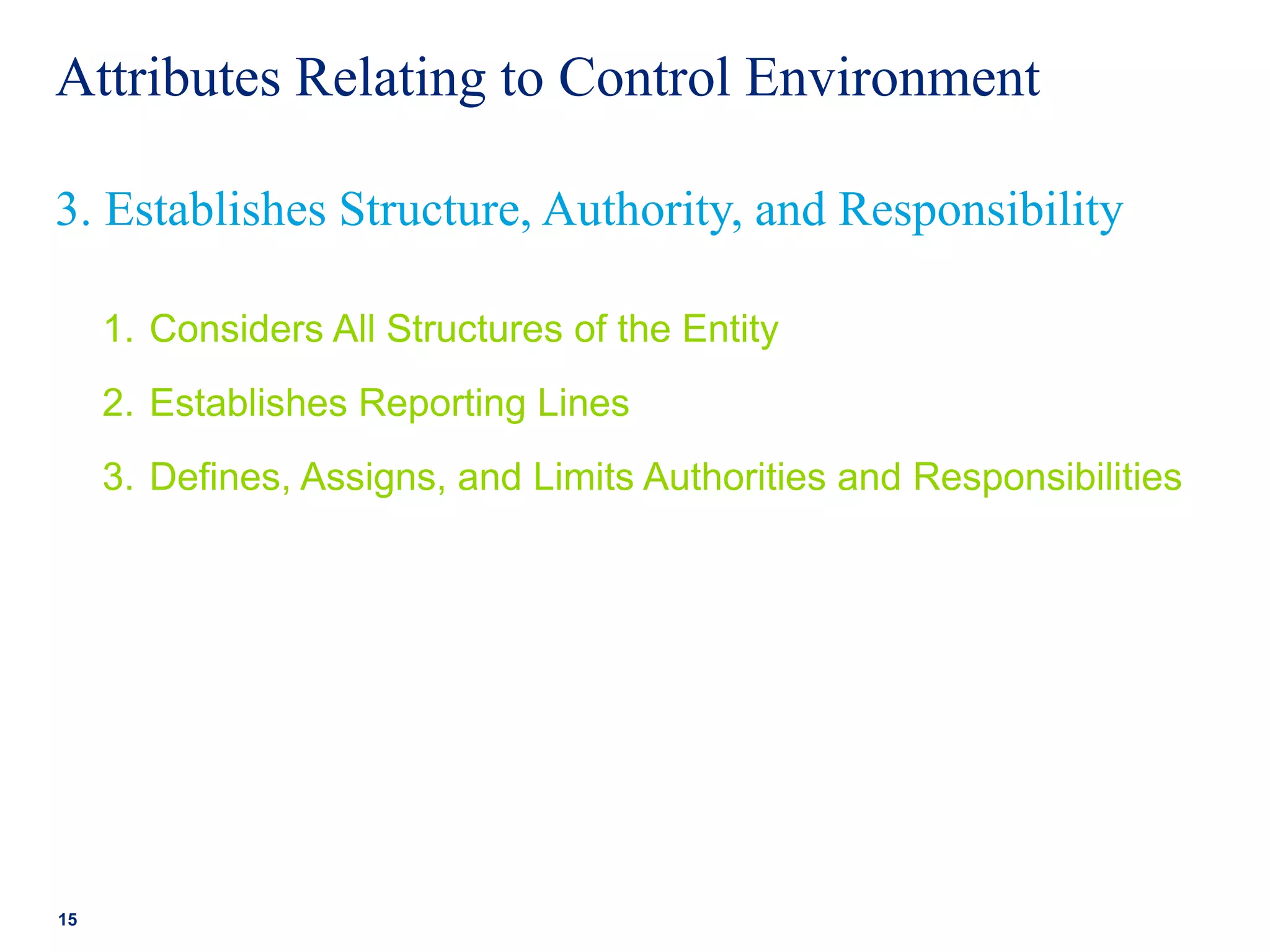

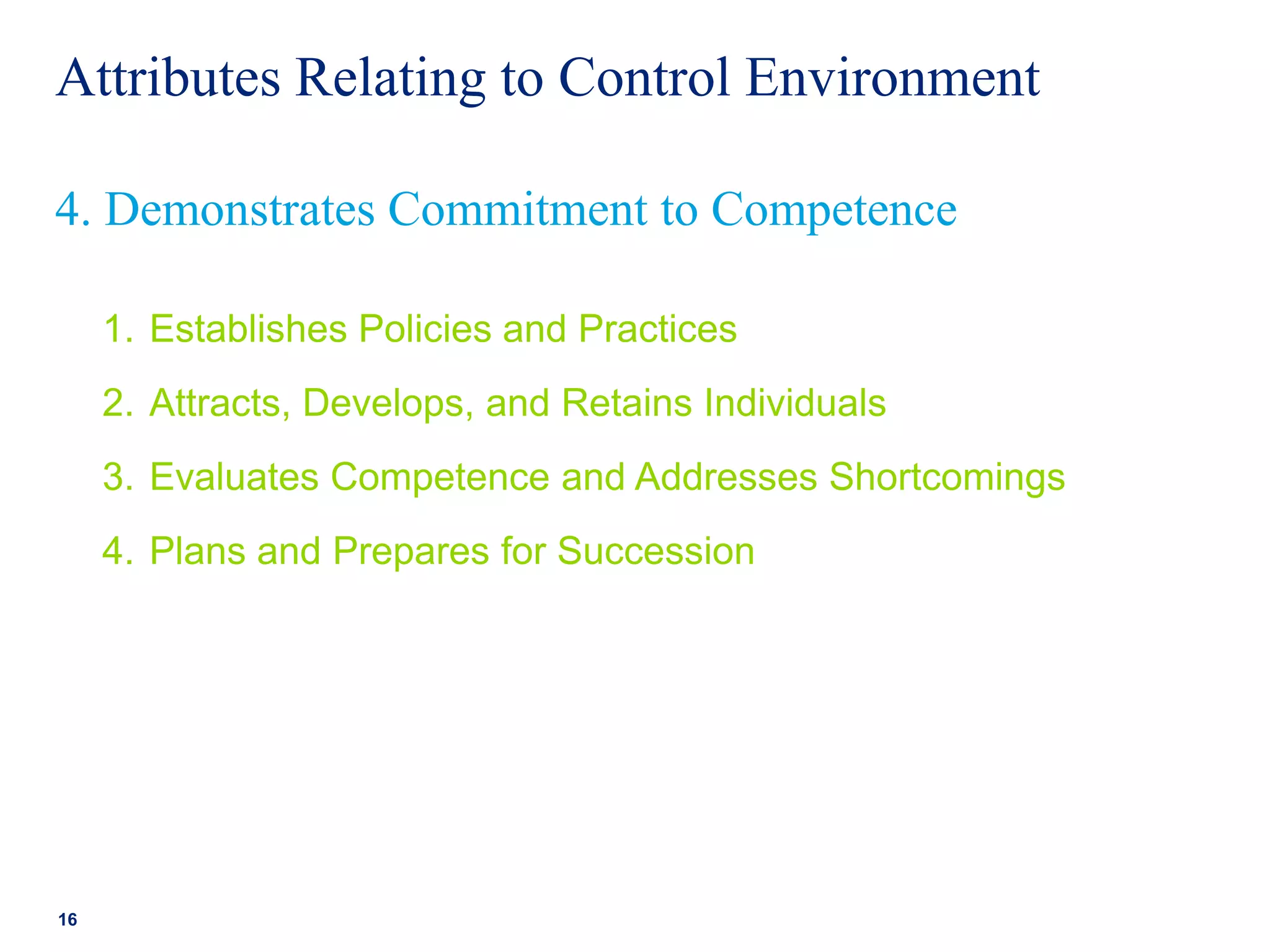

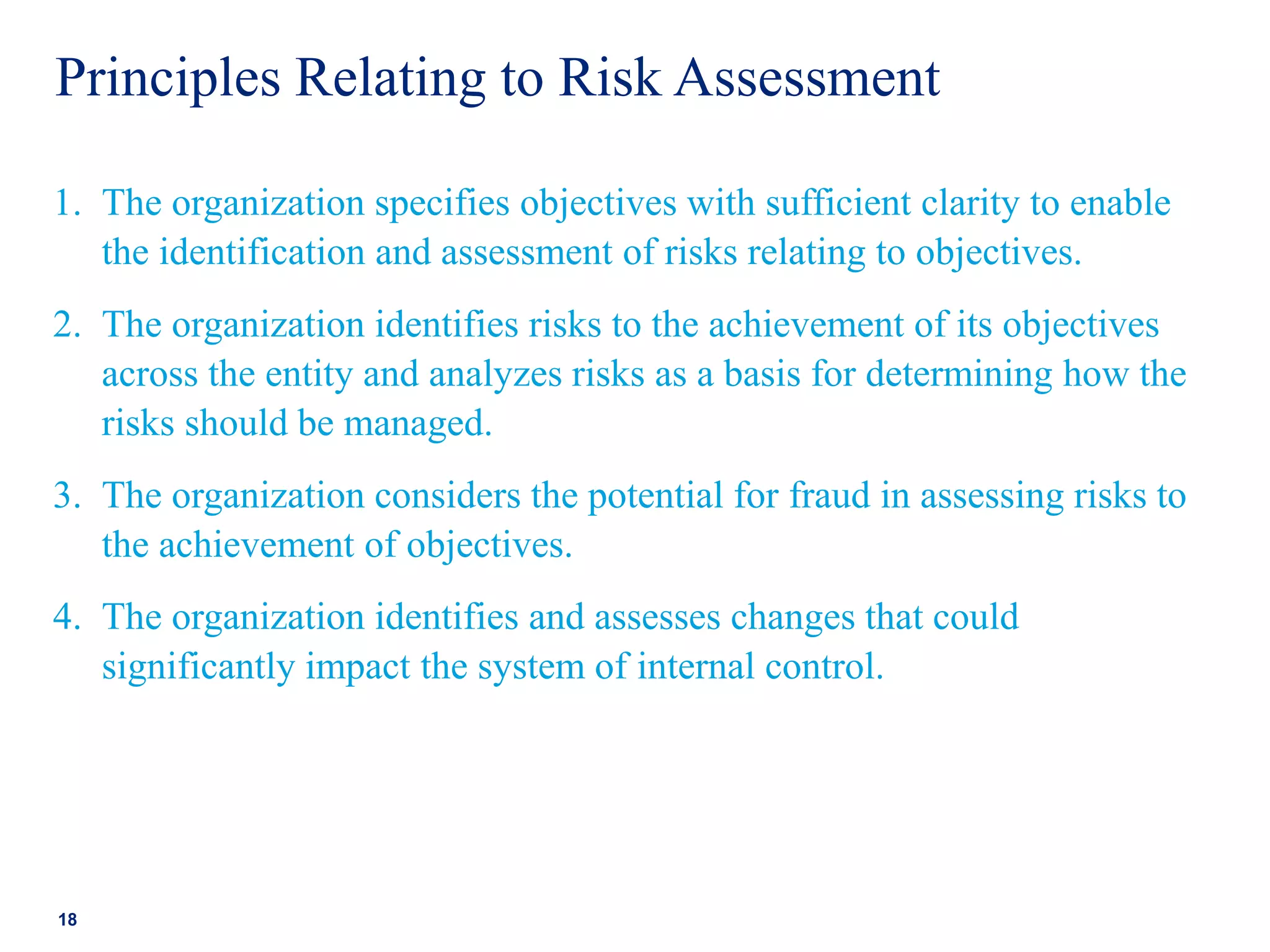

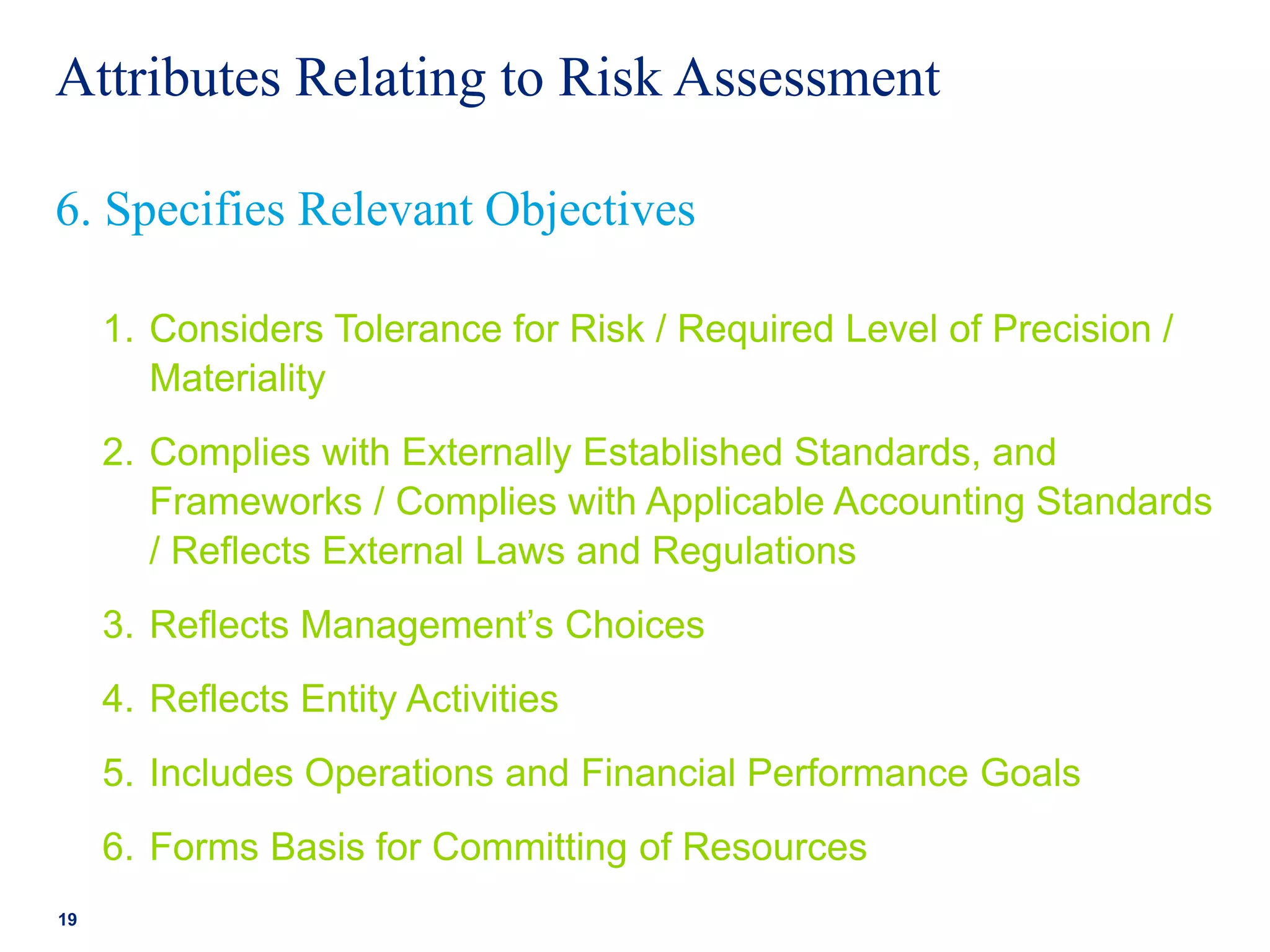

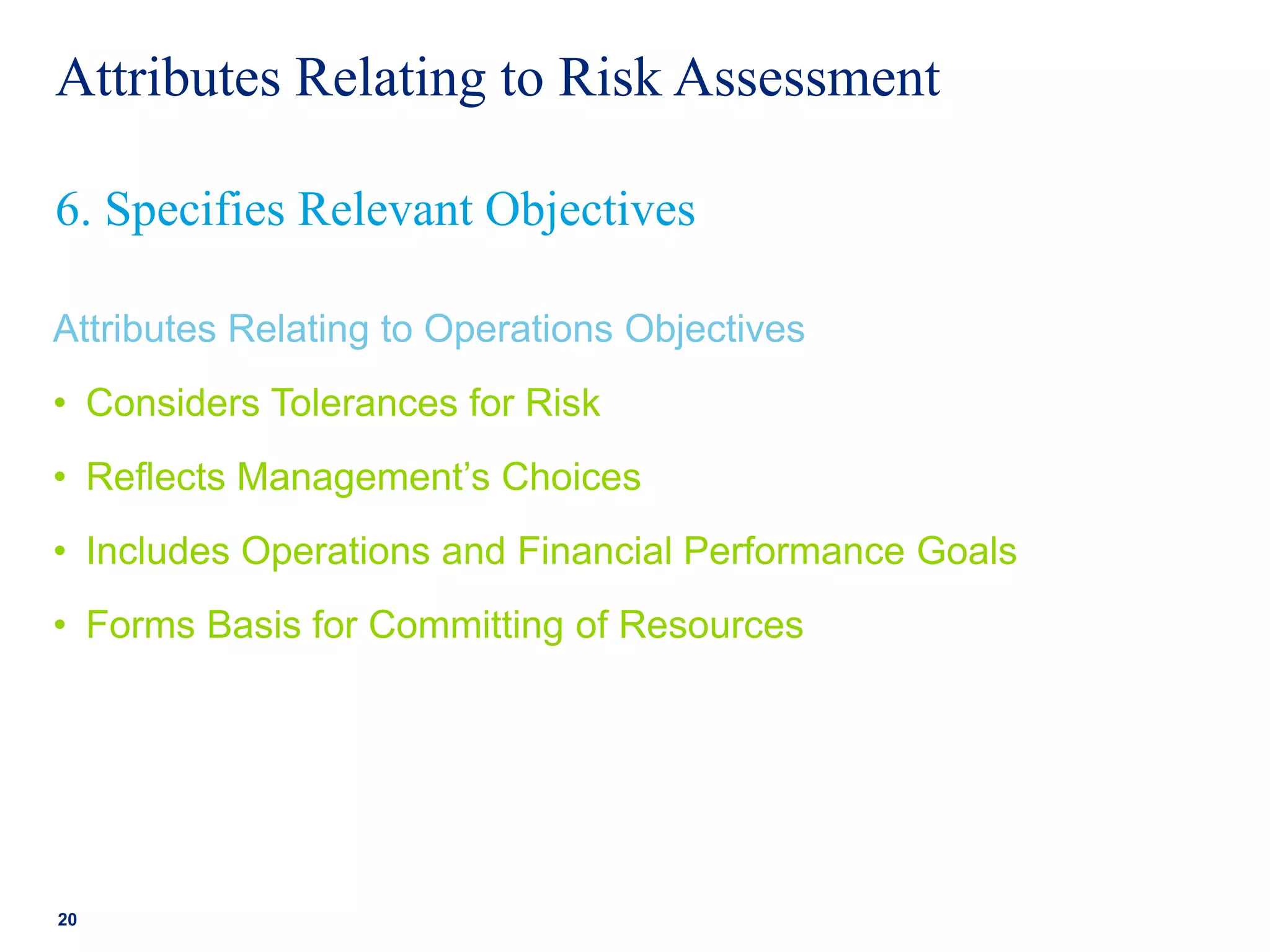

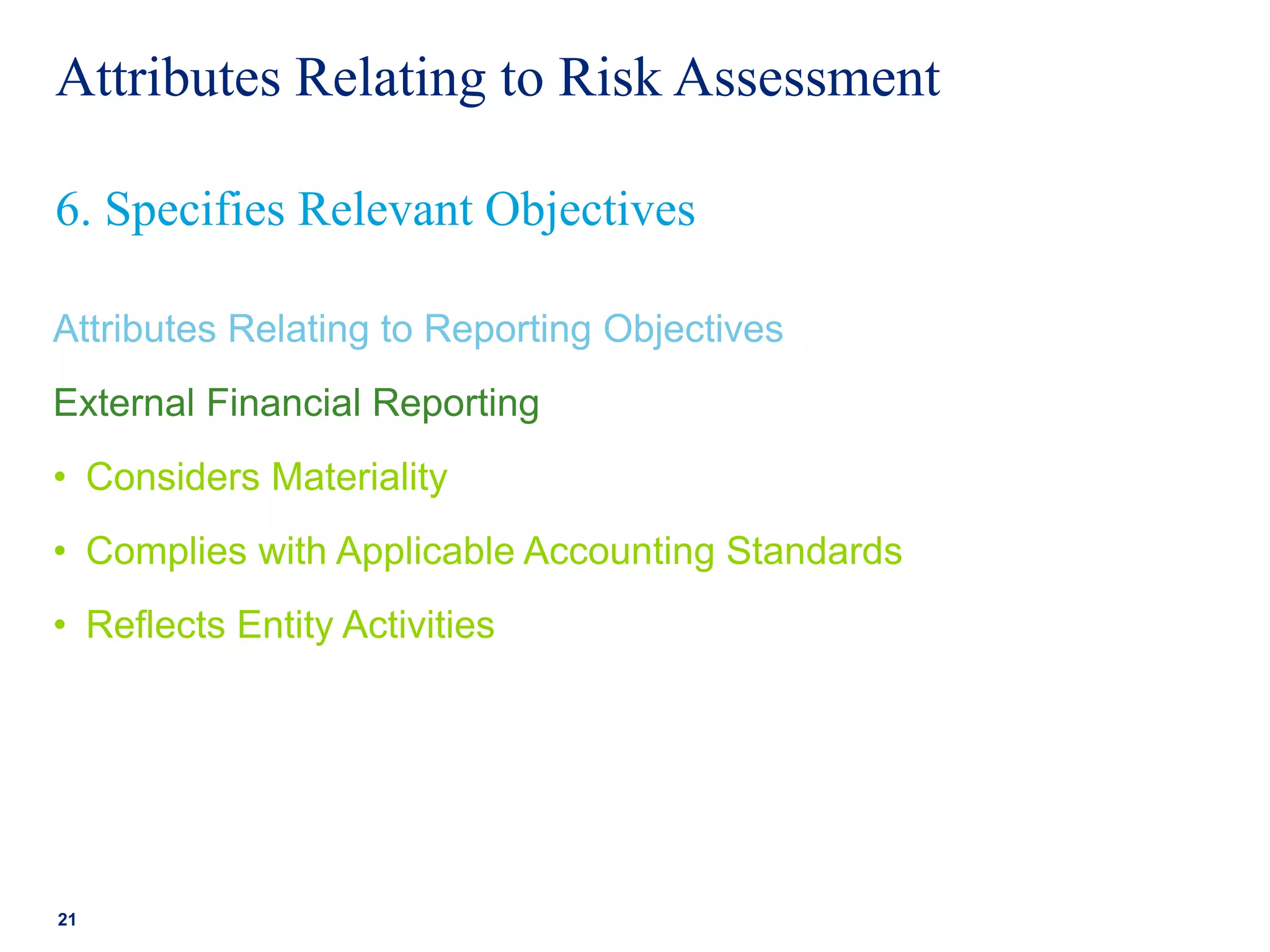

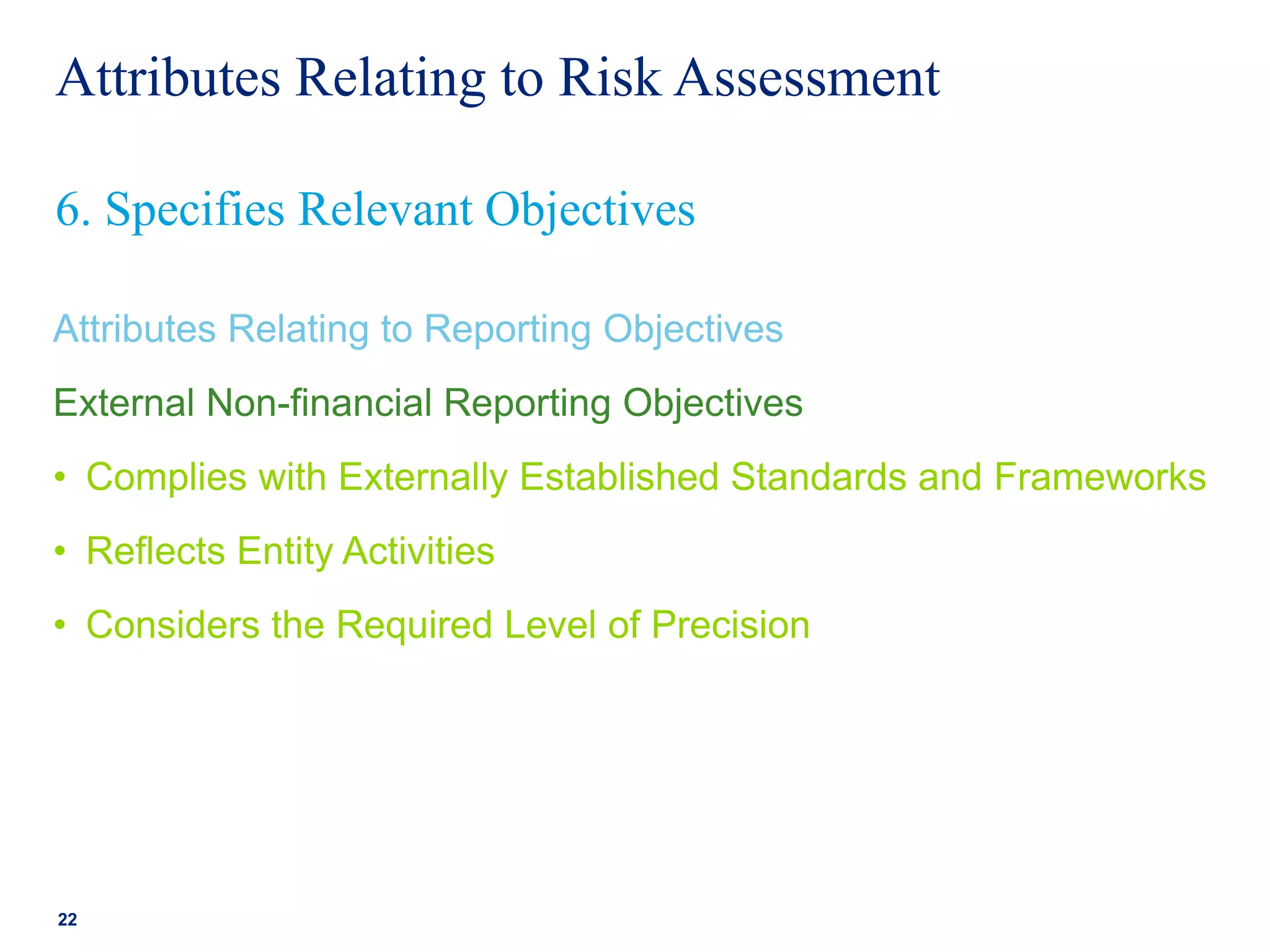

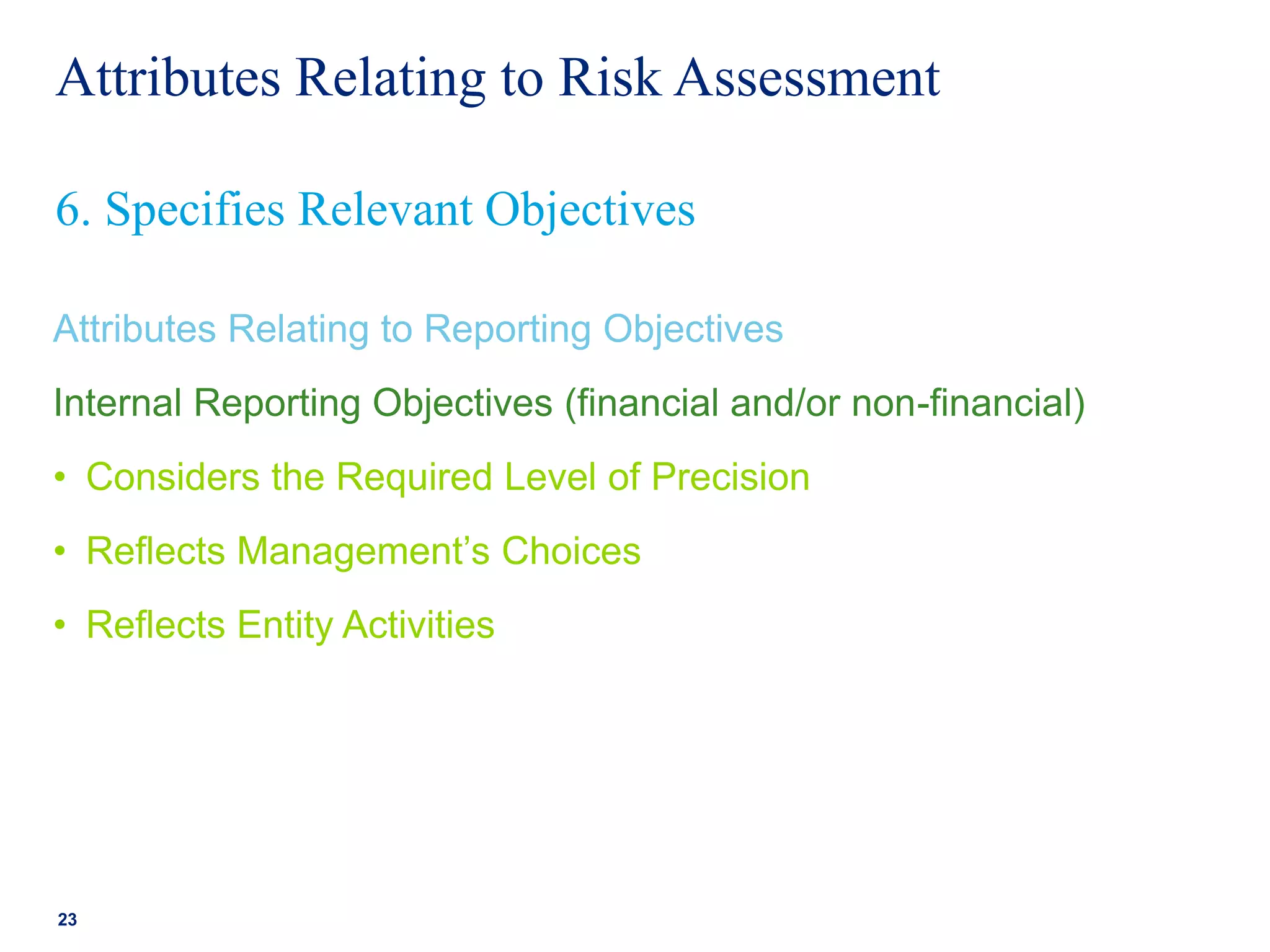

Explores principles and attributes related to the control environment and risk assessment.

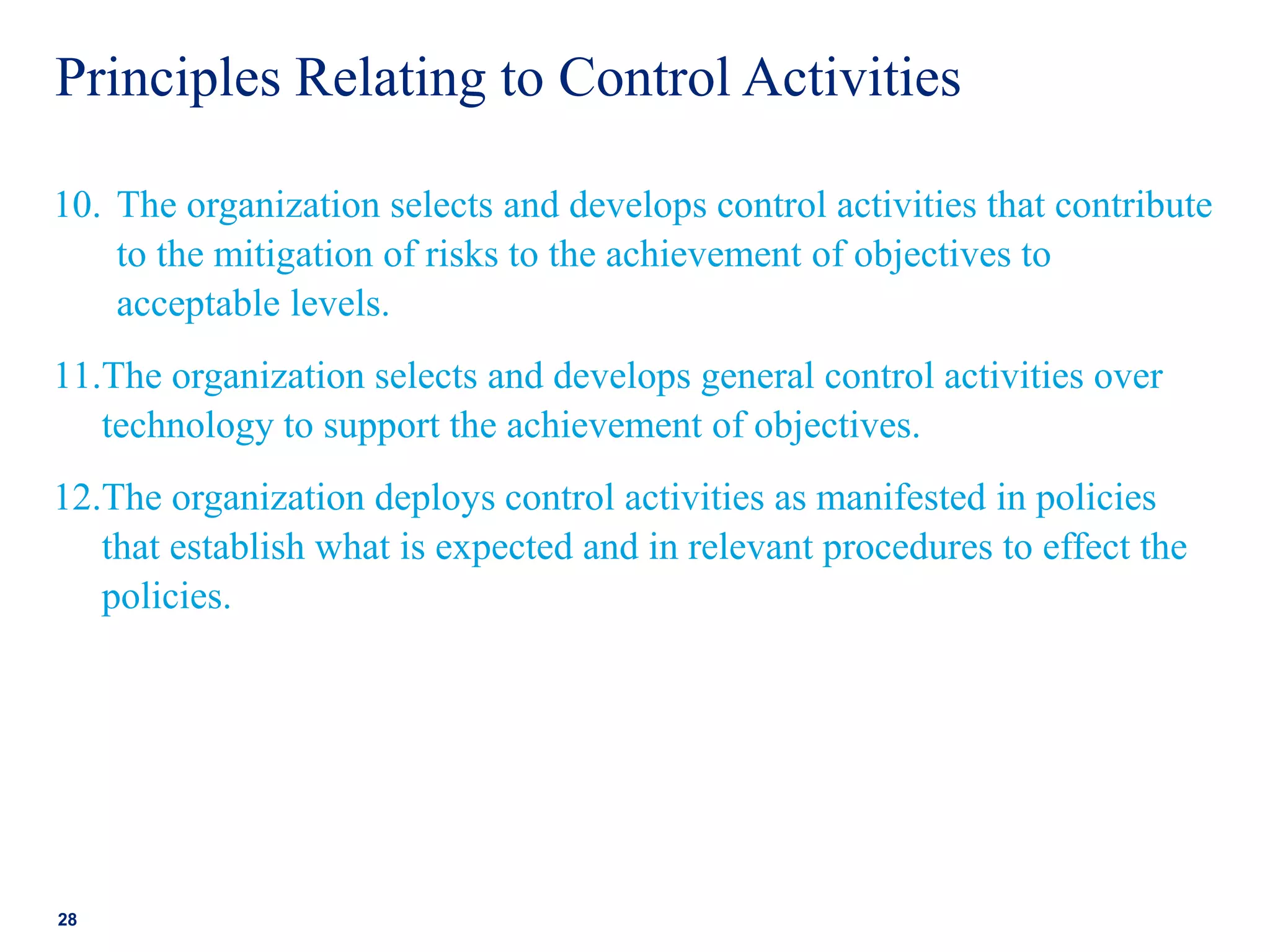

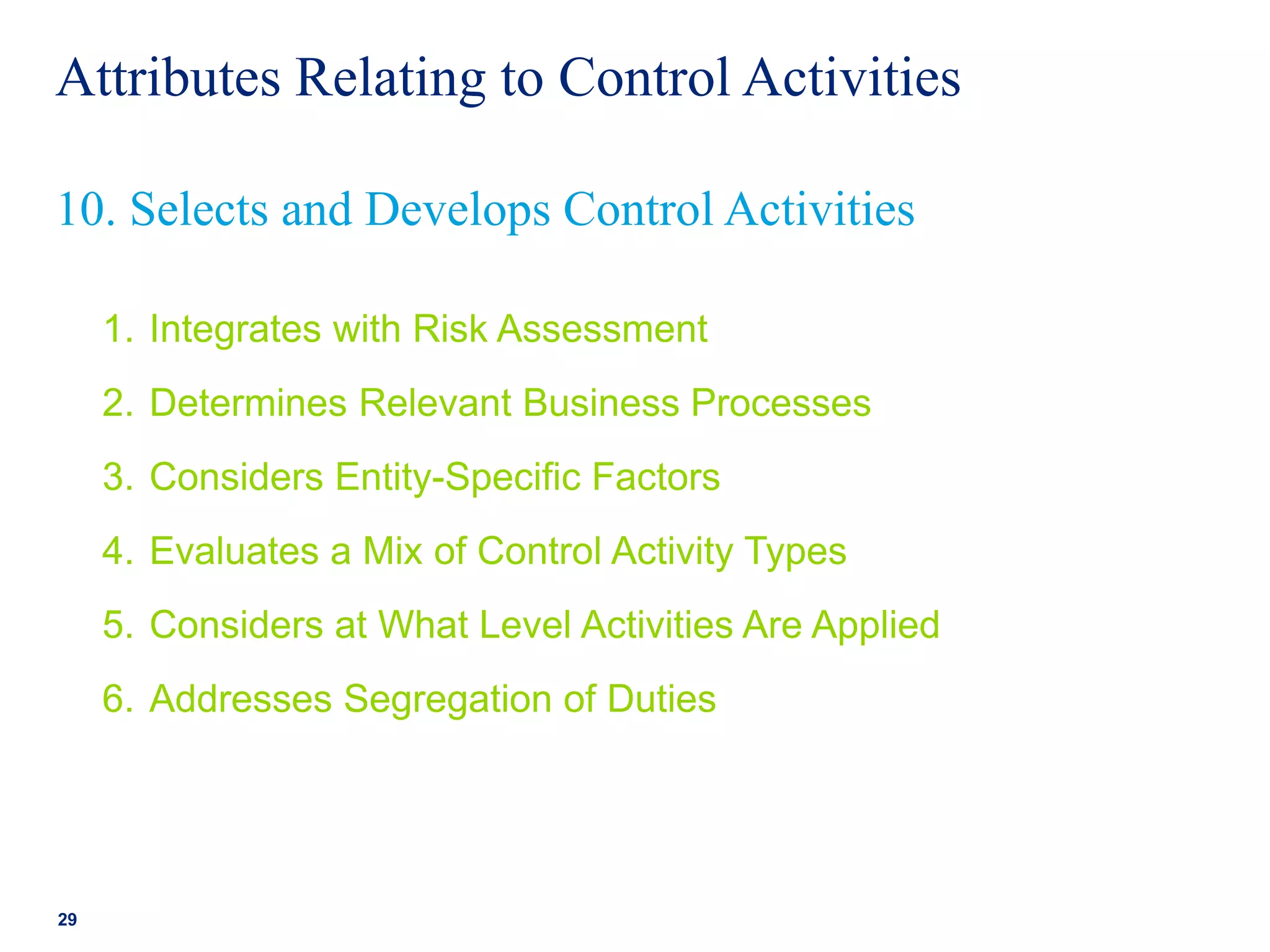

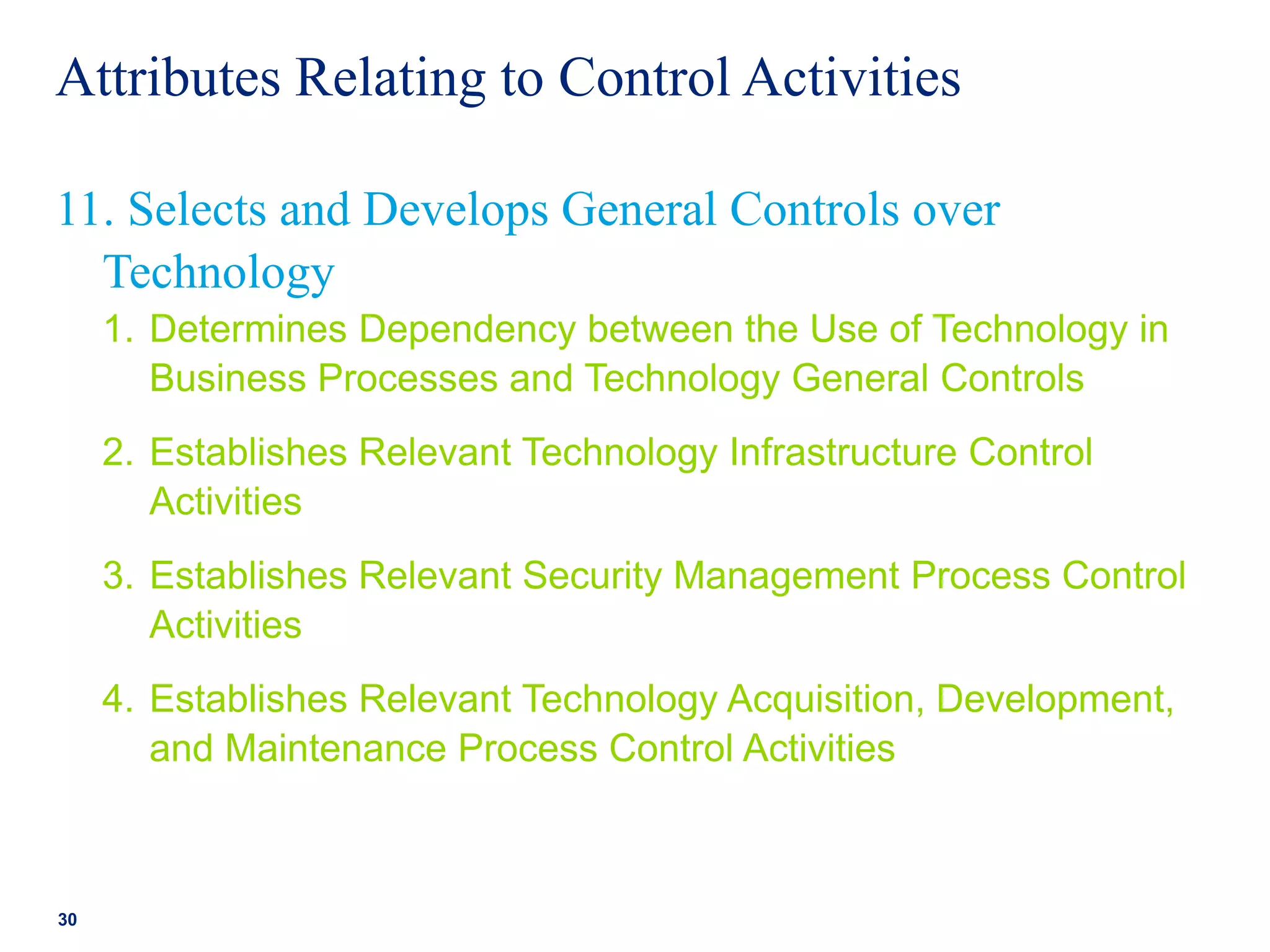

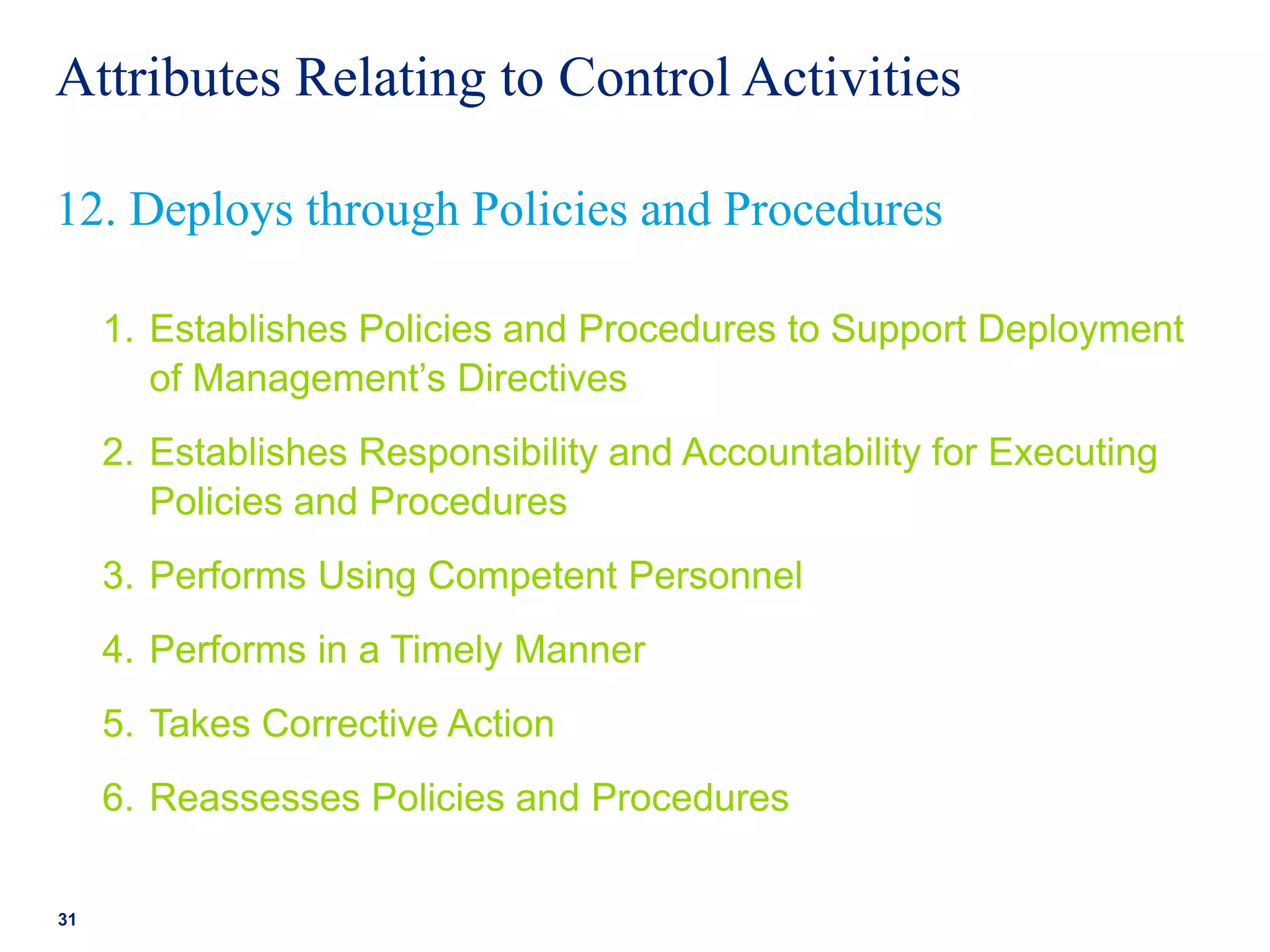

Principles relating to the selection and development of control activities to mitigate risks.

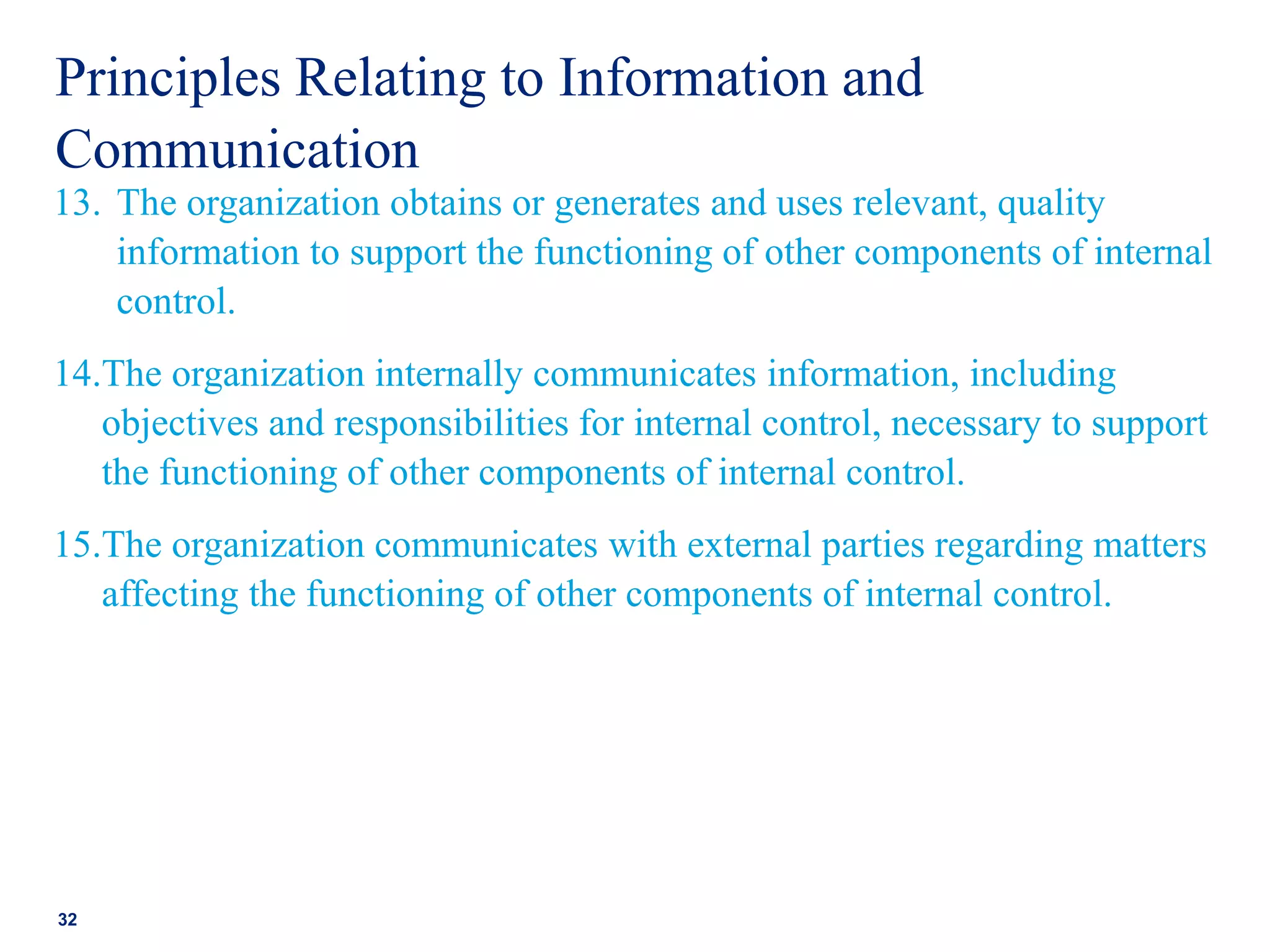

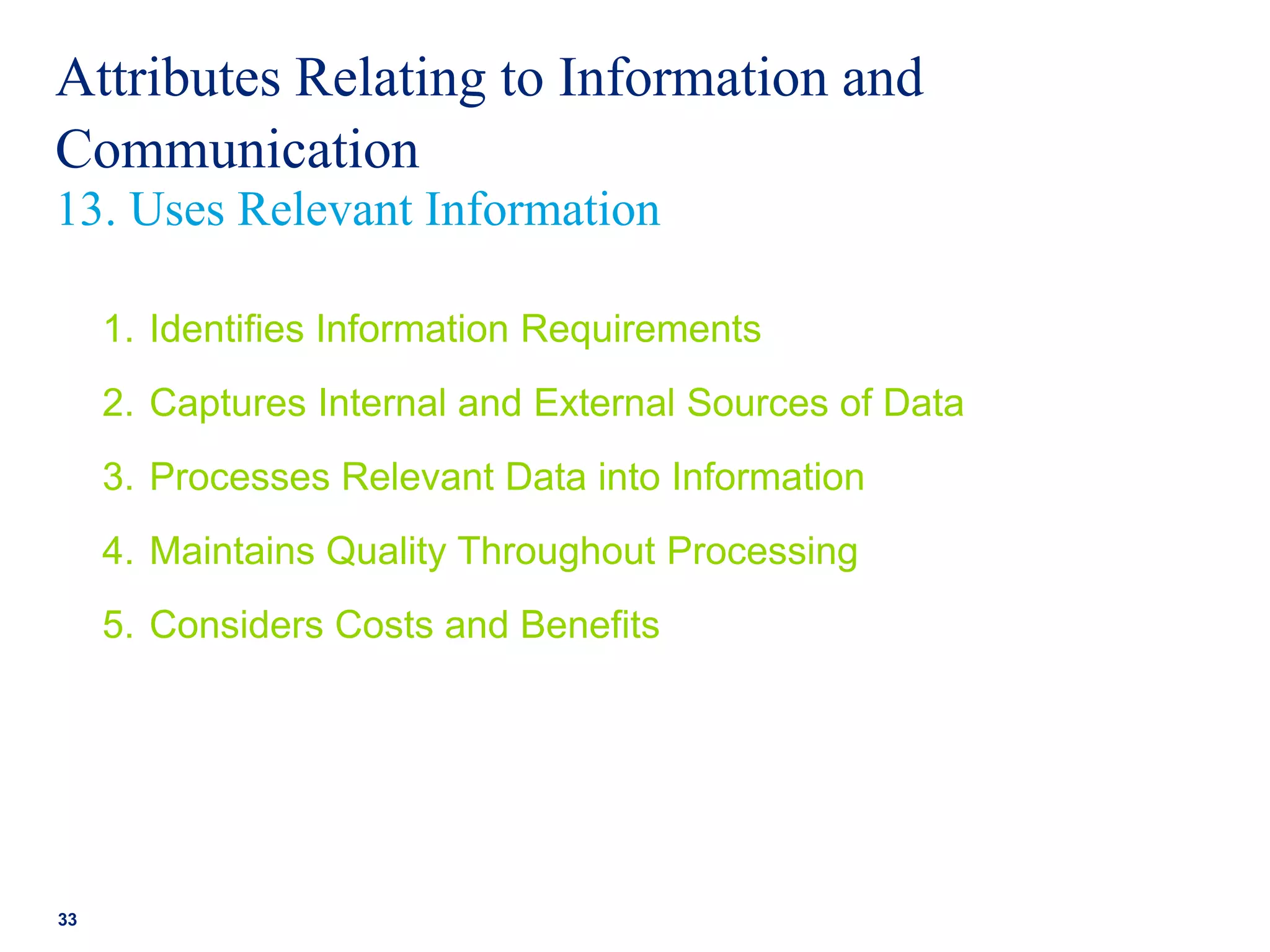

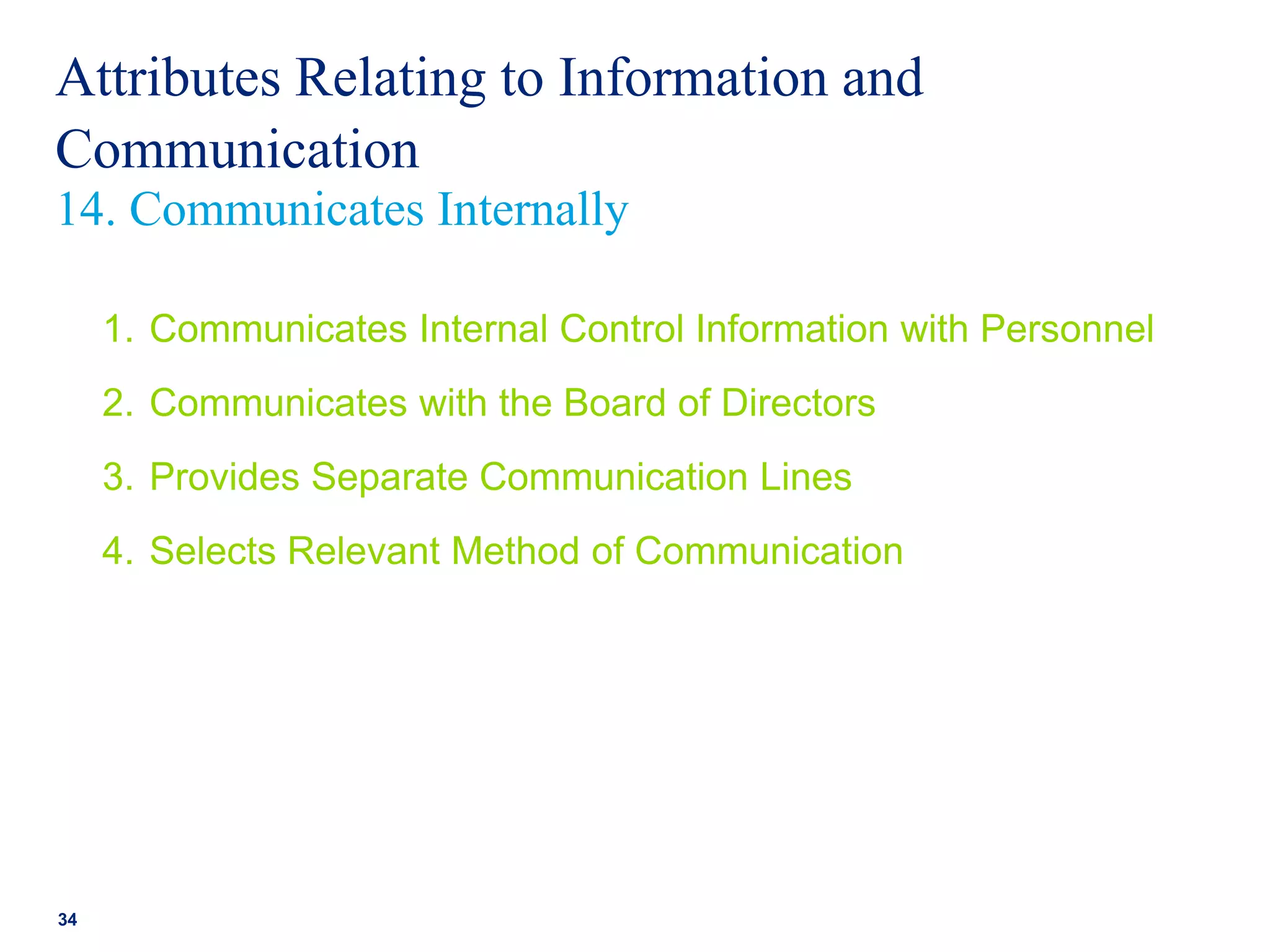

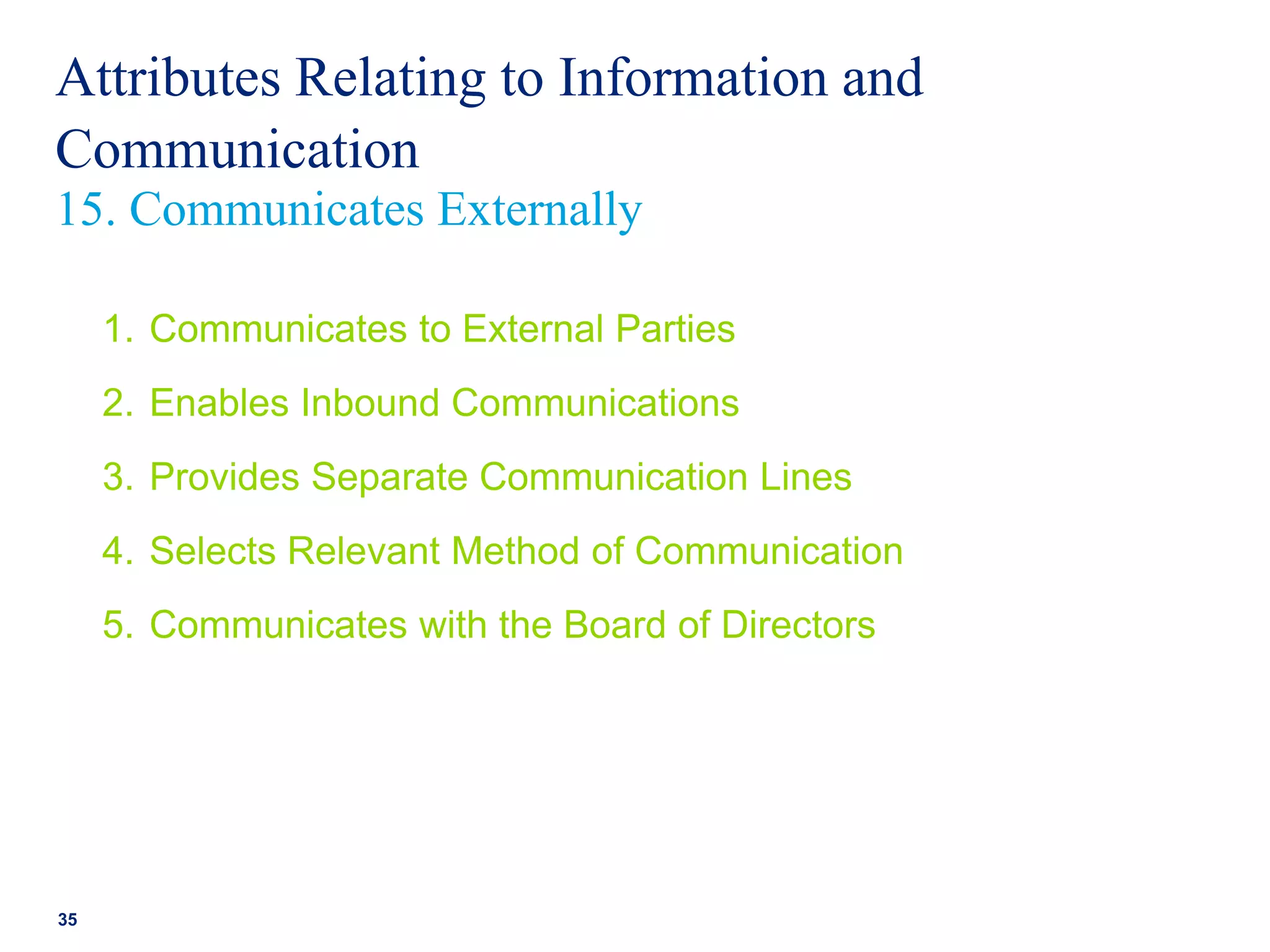

Principles for effective information handling and communication within an internal control framework.

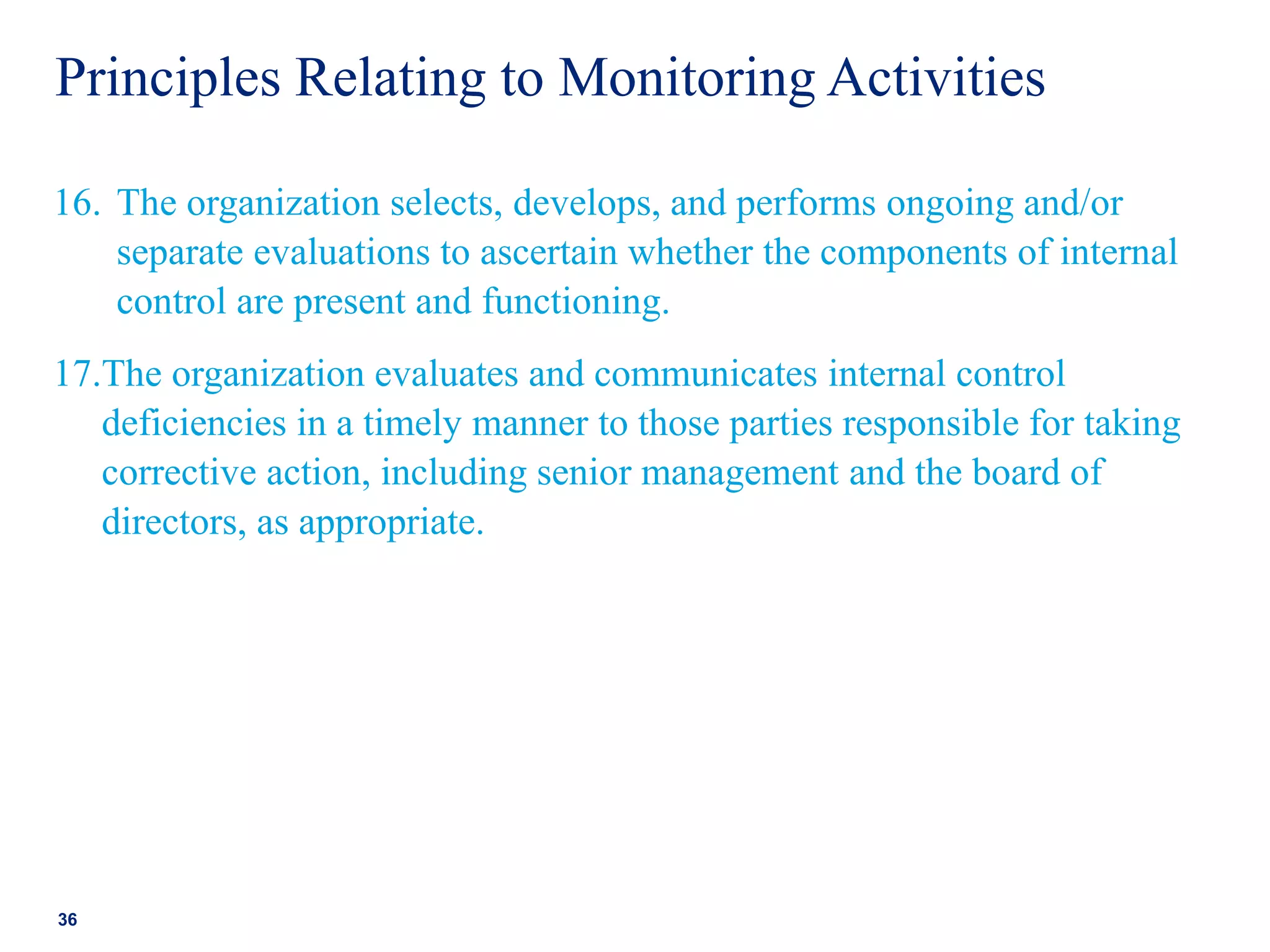

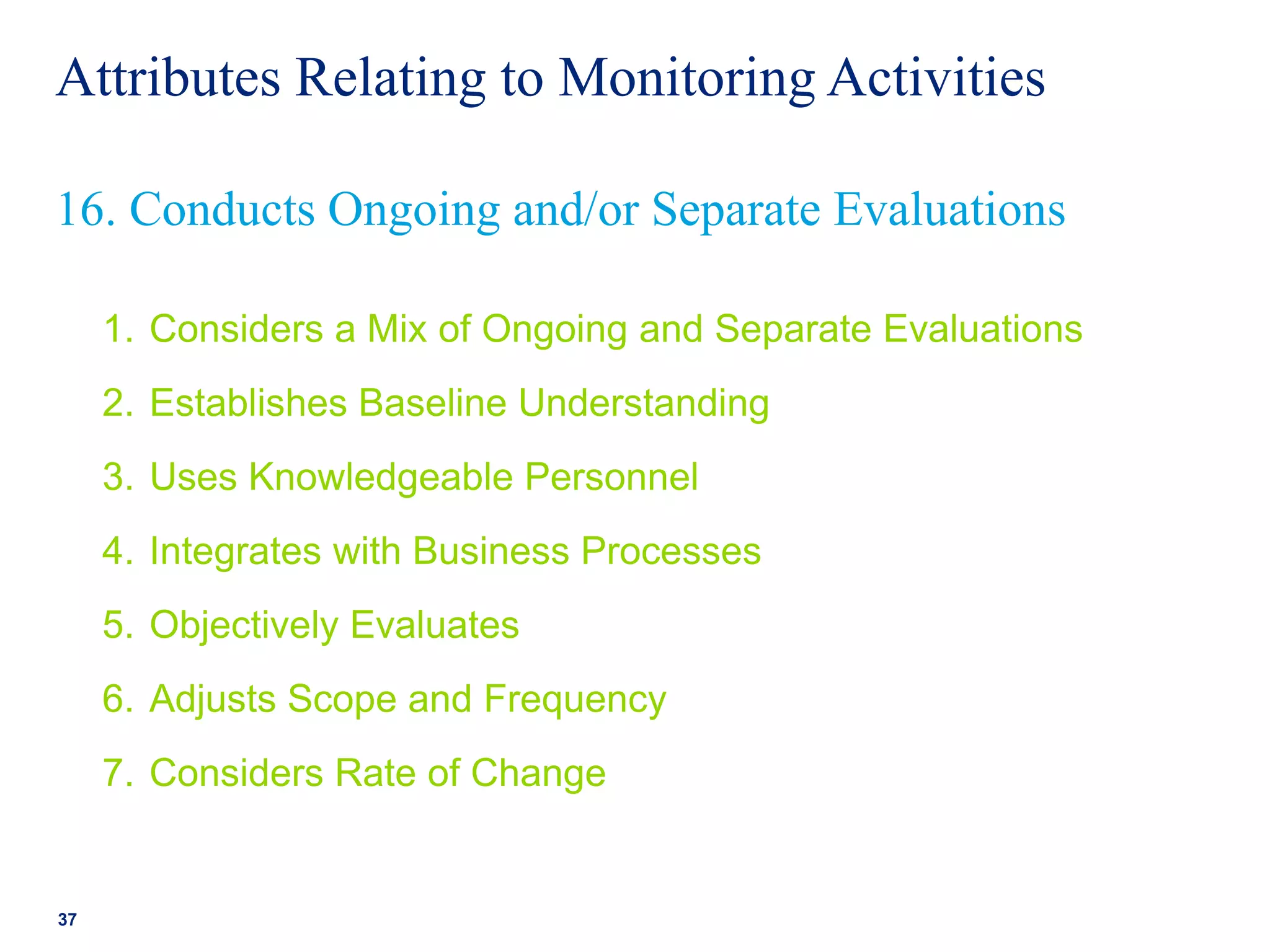

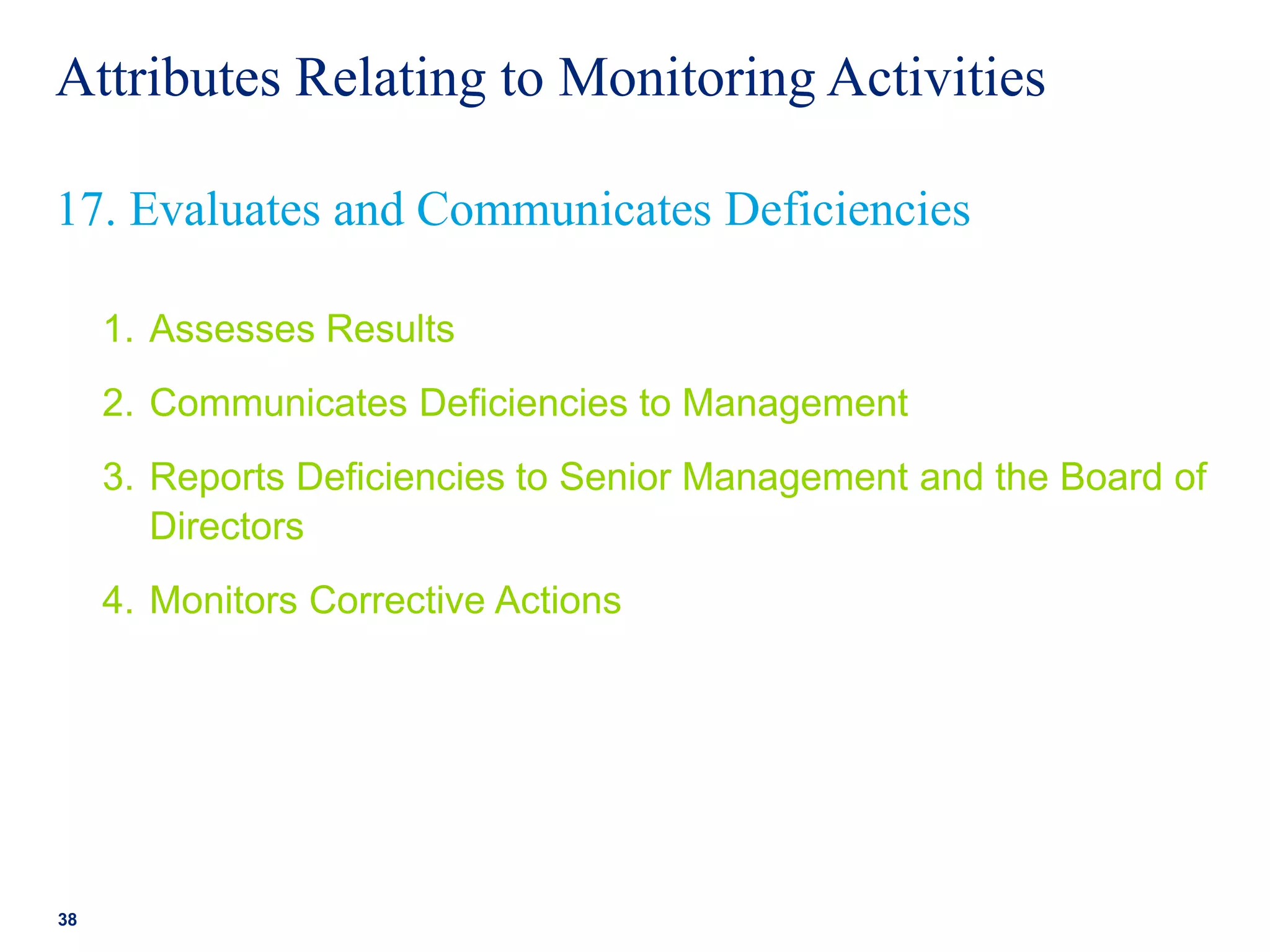

Discussion on principles and attributes for monitoring activities to ensure internal control effectiveness.

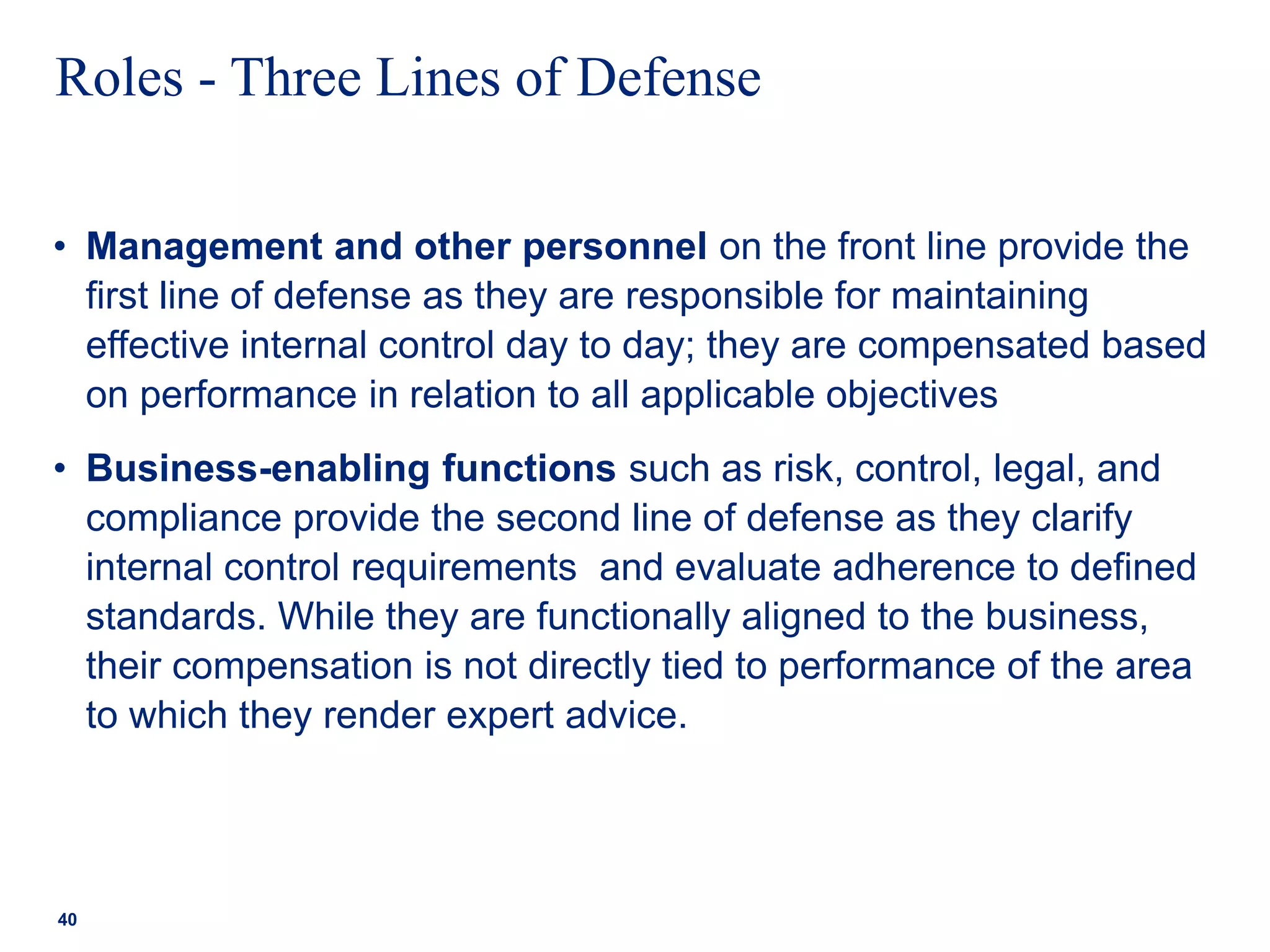

Defines the roles of various parties including management, board of directors, and internal auditors in internal control.

Criteria for assessing the effectiveness of internal controls and recognizing potential limitations.

Distinguishes what constitutes internal control versus decisions made by the board and opens for Q&A.