Downloaded 199 times

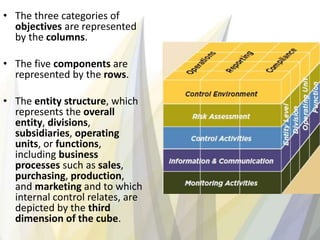

The document outlines the definition and components of internal control, emphasizing its role in achieving objectives related to operations, reporting, and compliance. It details the five key components: control environment, risk assessment, control activities, information and communication, and monitoring activities, and explores various principles and points of focus within each component. The document concludes by acknowledging the inherent limitations of internal controls, stating they can only provide reasonable assurance of achieving an entity's objectives.