Areva T&D India 2QCY2010 Results Below Estimates on Margin Pressures

1. 2QCY2010 Result update| Capital Goods

July 30, 2010

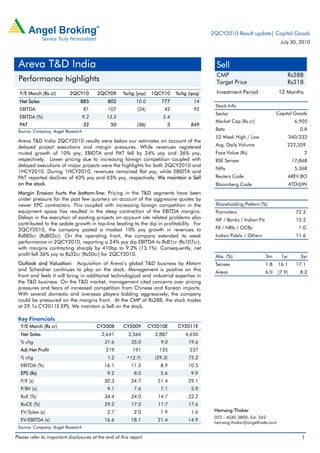

Areva T&D India Sell

CMP Rs288

Performance highlights Target Price Rs218

Y/E March (Rs cr) 2QCY10 2QCY09 %chg (yoy) 1QCY10 %chg (qoq) Investment Period 12 Months

Net Sales 885 802 10.0 777 14

Stock Info

EBITDA 81 107 (24) 42 92

Sector Capital Goods

EBITDA (%) 9.2 13.3 5.4

Market Cap (Rs cr) 6,905

PAT 32 50 (36) 3 849

Source: Company, Angel Research Beta 0.8

52 Week High / Low 340/232

Areva T&D India 2QCY2010 results were below our estimates on account of the

delayed project executions and margin pressures. While revenues registered Avg. Daily Volume 222,359

muted growth of 10% yoy, EBIDTA and PAT fell by 24% yoy and 36% yoy, Face Value (Rs) 2

respectively. Lower pricing due to increasing foreign competition coupled with BSE Sensex 17,868

delayed executions of major projects were the highlights for both 2QCY2010 and

Nifty 5,368

1HCY2010. During 1HCY2010, revenues remained flat yoy, while EBIDTA and

PAT reported declines of 43% yoy and 65% yoy, respectively. We maintain a Sell Reuters Code AREV.BO

on the stock. Bloomberg Code ATD@IN

Margin Erosion hurts the bottom-line: Pricing in the T&D segments have been

under pressure for the past few quarters on account of the aggressive quotes by

newer EPC contractors. This coupled with increasing foreign competition in the Shareholding Pattern (%)

equipment space has resulted in the steep contraction of the EBITDA margins. Promoters 72.2

Delays in the execution of existing projects on account site related problems also MF / Banks / Indian Fls 15.2

contributed to the sedate growth in top-line leading to the dip in profitability. For

2QCY2010, the company posted a modest 10% yoy growth in revenues to FII / NRIs / OCBs 1.0

Rs885cr (Rs802cr). On the operating front, the company extended its weak Indian Public / Others 11.6

performance in 2QCY2010, reporting a 24% yoy dip EBITDA to Rs81cr (Rs107cr),

with margins contracting sharply by 410bp to 9.2% (13.1%). Consequently, net

profit fell 36% yoy to Rs32cr (Rs50cr) for 2QCY2010. Abs. (%) 3m 1yr 3yr

Outlook and Valuation: Acquisition of Areva’s global T&D business by Alstom Sensex 1.8 16.1 17.1

and Scheidner continues to play on the stock. Management is positive on this

Areva 6.0 (7.9) 8.2

front and feels it will bring in additional technological and industrial expertise in

the T&D business. On the T&D market, management cited concerns over pricing

pressures and fears of increased competition from Chinese and Korean imports.

With several domestic and overseas players bidding aggressively, the company

could be pressured on the margins front. At the CMP of Rs288, the stock trades

at 29.1x CY2011E EPS. We maintain a Sell on the stock.

Key Financials

Y/E March (Rs cr) CY2008 CY2009 CY2010E CY2011E

Net Sales 2,641 3,566 3,887 4,650

% chg 31.6 35.0 9.0 19.6

Adj Net Profit 219 191 135 237

% chg 1.2 12.7) (29.3) 75.2

EBITDA (%) 16.1 11.3 8.9 10.5

EPS (Rs) 9.2 8.0 5.6 9.9

P/E (x) 30.3 34.7 51.4 29.1

P/BV (x) 9.1 7.6 7.1 5.9

RoE (%) 34.4 24.0 14.7 22.2

RoCE (%) 29.2 17.0 11.7 17.6

EV/Sales (x) 2.7 2.0 1.9 1.6 Hemang Thaker

022 - 4040 3800; Ext: 342

EV/EBITDA (x) 16.6 18.1 21.4 14.9

hemang.thaker@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. Areva T&D India | 2QCY2010 Result update

Exhibit 1: 2QCY2010 Performance

Y/E March (Rs cr) 2QCY2010 2QCY2009 % chg(yoy) 1QCY2010 % chg (qoq) CY2009 CY2008 %chg (yoy)

Net Sales 885 802 10 777 14 3,583 2,655 35.0

Raw Material 595 529 12 568 5 2,493 1,726 44.4

(% of Net Sales) 67.2 65.9 73.1 70 65

Employee Cost 87 70 24 86 1 292 209 39.8

(% of Net Sales) 9.8 8.7 11.0% 8.2 7.9

Other Expenses 122 96 27 81 51 379 281 34.9

(% of Net Sales) 13.8 12.0 10.5 10.6 10.6

Total Expenditure 804 695 16 735 9 3,164 2,216 42.8

EBITDA 81 107 (24) 42 93 419 439 (4.6)

EBITDA (%) 9.2 13.3 5.4 11.7 16.5

Interest 10 16 (37) 13.4 (23) 57.9 30.2 91.7

Depreciation 23 11 96 23.7 (5) 61.1 34 79.7

Others (4) - (8) (39) (79.5)

Profit before Tax 49 76 (36) 5.1 854 292 336 (13.1)

(% of Net Sales) 5.5 9.4 8.1 12.6

Total Tax 16 26 (36) 1.7 865 101 121 (16.3)

(% of PBT) 33.7 33.9 33.3 34.6 35.9

Adjusted PAT 32 50 (36) 3 849 191 215 (11.3)

(% of Net Sales) 3.6 6.2 5.3 8.1

Extraordinary items - - 1.5 11.5 (85.5)

Reported PAT 32 50 (36) 3 192 226 (14.9)

Source: Company, Angel Research

Pricing pressures – key cause for the sharp dent in margins: On the Operating

front, Areva T&D reported a sharp dent in EBITDA margin, by 410bp yoy to 9.2%

(13.3%) for 2QCY2011, which was below our estimate. This was partially due to

high raw material costs, which increased by 130bp to 67.2% (65.9%) of net sales.

Notably, the increased competitive pressures prevalent in the market have put a

severe strain on margins, with prices on an average falling by about 30% (25% for

transmission and 32-35% for distribution) for the company’s products. Employee

cost also rose sharply by 24% yoy to Rs87cr (Rs70cr). Besides, increased other

expenses including ramp up cost in the new factories, higher provisioning for

certain projects and mark-to-market losses (Rs12cr) further compounded the

margin fall for 2QCY2010. Consequently, net profit dropped by 36% yoy to

Rs32cr (Rs50cr). For 1HCY2010, net profit dropped sharply by 65% yoy to Rs35cr

(Rs101cr).

Management’s view on the T&D market: Management indicated uncertainty in the

revival of T&D market in 2HCY2010 mainly due to concerns on industry and

infrastructure sector that did not look positive. Pricing pressures were witnessed due

to many players entering the T&D space. Furthermore, the company faces threat

from Chinese and Korean players that have expertise in T&D products, which will

lead to competitive pressures. Price erosion remained a concern; the T&D segment

has witnessed price erosions of 25% and 32%, respectively. Management also

reasoned the low order intake, which was mainly on account of muted pace of

investments in the infrastructure space and high deficit between planned and

actual investments by the government.

July 30, 2010 2

3. Areva T&D India | 2QCY2010 Result update

Order inflows: The order backlog came in at Rs5,112cr, up 21% yoy. The order

inflow for the quarter was Rs1,019.2cr. Among the significant orders received by

the company during the quarter includes an electrical Balance of Plant (eBOP)

contract for the Warora thermal power plant, which is being set by the GMR Group

in Maharashtra. The contract, valued at ~Rs130cr, is for the supply and

installation of eBOP solutions for 2x300 MW thermal power plants in Warora

taluka in the district of Chandrapur, Maharashtra. The power project is coming up

in two phases of 300MW each in Warora.

Exhibit 2: Quarterly order backlog

6,000

4,975 5,112

5,000 4,600 4,775

3,932 4,097 4,232 4,225

4,000

3,230

(Rs cr)

3,000

2,000

1,000

-

2CY08 3CY08 4CY08 1CY09 2CY09 3CY09 4CY09 1CY10 2CY10

Source: Company, Angel Research

Sale process update – Chronology of events

In CY2009, Areva, the ultimate holding company decided to exit global T&D

business and consequent to the decision, Areva’s Executive Board has begun

negotiations with the Alstom-Schneider Consortium.

On January 2010, the Indian management was informed about the share

purchase agreement that was signed between the Areva Group and Alstom-

Schneider Electric (subject to clearances from the EU Commission and other

authorities).

On May 28, 2010, an open offer was launched by Alstom & Schneider to

acquire up to 4.78cr shares constituting 20% of issued share capital of Areva

T&D India at Rs295.4 per share.

On June 7, 2010, the global sale process was closed after

Alstom-Schneider Electric obtained required clearances from all the

authorities.

On July 20, 2010, the open offer was postponed till further notice due to

pending clearance of the open offer document from SEBI till date.

July 30, 2010 3

4. Areva T&D India | 2QCY2010 Result update

Investment Concerns

Generation delays to impact T&D growth: Areva T&D's fortunes are directly linked

to the growth of the Indian power sector. In the present macro environment,

though the power sector capex is relatively resilient with majority of the projects

being envisaged by the central and state sector utilities, major worry for the T&D

sector is generation capacity addition delays. This is likely to adversely impact

growth prospects for the T&D equipment suppliers as the sector has a high degree

of correlation with power capacity addition. Notably, around 60% of the planned

transmission expenditure for the Eleventh Plan is directly associated with the

concurrent addition in generation capacity. Historically, India has had a poor track

record with only 50-60% of planned capacity added during several previous plans

and even for the current Plan period, the execution rate has been pretty dismal

with around 54% of the projects already running behind schedule.

Margins to contract: During CY2010E -11E, we expect EBITDA margin to sedate to

10.5%, compared to historic margins of 15% (3-yr avg from CY2007 to CY2009).

This is mainly on account of:

(1) Increasing contribution of systems segment, which entails higher bought-out

items and hence comparatively lower margins.

(2) Increasing competitive pressure in the market; management has also admitted

to price undercutting by some players to win orders.

(3) The company's contracts have a price variation clause (PVC); hence, resultant

benefits from lower commodity prices would be passed on to customers.

Lower margins will spiral down to lesser profitability; Net profit margins are

estimated to come in at 5.1% by CY2011E, which has averaged around 8% (3-yr

avg. from CY2007 to CY2009).

Return ratios to decline: Areva T&D's return ratios seem to have peaked out and

are on a declining trend. During CY2010-11E, we expect company to clock 14.7%

and 22.2% RoE respectively, owing to contraction in the net profit margin coupled

with the fall in the asset turnover ratio. The asset turnover ratio is expected to

decline on the huge capex (Rs100cr) guided by the company for 2010E, while the

utilisation of the assets would improve gradually.

Outlook and Valuation: Acquisition of Areva’s global T&D business by Alstom and

Scheidner continues to play on the stock. Management is positive on this front and

feels it will bring in additional technological and industrial expertise in the

transmission and distribution business. However, management cited concerns over

pricing pressures and fear of increased competition from Chinese and Korean

imports. With several domestic and overseas players bidding aggressively, the

company could be pressured on the margins front. At the CMP of Rs288, the stock

trades at 29.1x CY2011E EPS. We maintain a Sell on the stock.

July 30, 2010 4

5. Areva T&D India | 2QCY2010 Result update

Exhibit 3: Actual v/s Angel estimates

Particulars (Rs cr) Actual Estimates Var. (%)

Revenues 885 918 3.7

Operating Profit 81 74 (8.8)

PAT 32 22 (31.3)

EPS (Rs) 1.3 0.9 (30.8)

Source: Company, Angel Research

Exhibit 4: Key Assumptions

Particulars (%) CY10E CY11E

Order Inflow Growth 20.0 15.0

Order Backlog Growth 12.6 13.8

Order Book to Sales 45.0 45.0

Source: Company, Angel Research

Exhibit 5: Angel EPS forecast

Year (%) Angel forecast Bloomberg consensus Var

CY2010E 5.6 7.0 (1.4)

CY2011E 9.9 9.9 -

Source: Company, Angel Research

Exhibit 6: One-year forward P/E band

800

600

400

200

0

Jun-07

Jun-10

Apr-05

Sep-06

Mar-08

Sep-09

Dec-05

Dec-08

Share Price (Rs) 8x 16x 24x 32x

Source: Company, Angel Research

July 30, 2010 5

11. Areva T&D India | 2QCY2010 Result update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Areva T&D

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock Yes

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

July 30, 2010 11