CA Varun Sethi - IndAS 102 - IFRS 2 - Share based payments - Accounting for modification or settlements of SBP and SBP among group employees

•

1 like•613 views

Explains through flowboxes - IndAS 102 - IFRS 2 - Share based payments - especially 1. Accounting for modification or settlements of SBP and 2. SBP among group employees

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Similar to CA Varun Sethi - IndAS 102 - IFRS 2 - Share based payments - Accounting for modification or settlements of SBP and SBP among group employees

Similar to CA Varun Sethi - IndAS 102 - IFRS 2 - Share based payments - Accounting for modification or settlements of SBP and SBP among group employees (20)

More from Varun Sethi

More from Varun Sethi (18)

Recently uploaded

Recently uploaded (20)

CA Varun Sethi - IndAS 102 - IFRS 2 - Share based payments - Accounting for modification or settlements of SBP and SBP among group employees

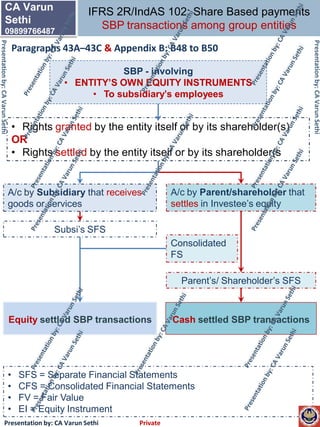

- 1. SBP - involving • ENTITY’S OWN EQUITY INSTRUMENTS • To subsidiary’s employees Equity settled SBP transactions Cash settled SBP transactions • Rights granted by the entity itself or by its shareholder(s) OR • Rights settled by the entity itself or by its shareholder(s A/c by Subsidiary that receives goods or services A/c by Parent/shareholder that settles in Investee’s equity Subsi’s SFS Parent’s/ Shareholder’s SFS Consolidated FS • SFS = Separate Financial Statements • CFS = Consolidated Financial Statements • FV = Fair Value • EI = Equity Instrument Presentation by: CA Varun Sethi Private CA Varun Sethi 09899766487 IFRS 2R/IndAS 102: Share Based payments SBP transactions among group entities Paragraphs 43A–43C & Appendix B: B48 to B50 Presentationby:CAVarunSethi Presentationby:CAVarunSethi

- 2. SBP - involving PARENT’S EQUITY INSTRUMENTS To Subsidiary’s employees EQUITY settled SBP transactions CASH settled SBP transactions 1. NO obligation of subsidiary 2. Obligation of PARENT 3. Rights granted by the PARENT /Subsidiary A/c by Subsidiary (that receives services) A/c by Parent (that settles in Investee’s equity) Subsi’s SFS Parent’s SFS Consolidated FS Presentation by: CA Varun Sethi Private CA Varun Sethi 09899766487 IFRS 2R/IndAS 102: Share Based payments SBP transactions among group entities Paragraphs 43A–43C & Appendix B: B51 to B55 Presentationby:CAVarunSethi Presentationby:CAVarunSethi • SFS = Separate Financial Statements • CFS = Consolidated Financial Statements • FV = Fair Value • EI = Equity Instrument

- 3. SBP - involving PARENT’S EQUITY INSTRUMENTS To Subsidiary’s employees CASH settled SBP transactions EQUITY settled SBP transactions 1. NO obligation of PARENT 2. Obligation of subsidiary 3. Rights granted by the Subsidiary A/c by Subsidiary (that receives services) A/c by Parent (that settles in Investee’s equity) Subsi’s SFS Parent’s CFS/ SFS Presentation by: CA Varun Sethi Private CA Varun Sethi 09899766487 IFRS 2R/IndAS 102: Share Based payments SBP transactions among group entities Paragraphs 43A–43C & Appendix B: B51 to B55 Presentationby:CAVarunSethi Presentationby:CAVarunSethi Presentationby:CAVarunSethi Presentationby:CAVarunSethi • SFS = Separate Financial Statements • CFS = Consolidated Financial Statements • FV = Fair Value • EI = Equity Instrument

- 4. SBP - involving Cash-settled payments to employees EQUITY settled SBP transactions CASH settled SBP transactions 1. Obligation of PARENT 2. NO obligation of subsidiary 3. Rights granted by the Subsidiary A/c by Subsidiary (that receives services) A/c by Parent (that settles in Investee’s equity) Subsi’s SFS Parent’s CFS/ SFS Presentation by: CA Varun Sethi Private CA Varun Sethi 09899766487 IFRS 2R/IndAS 102: Share Based payments SBP transactions among group entities Paragraphs 43A–43C & Appendix B: B56 to B58 Subsi’s employees will receive cash payments linked to price of its equity instruments Subsi’s employees will receive cash payments linked to price of PARENT’S equity instruments Presentationby:CAVarunSethi Presentationby:CAVarunSethi • SFS = Separate Financial Statements • CFS = Consolidated Financial Statements • FV = Fair Value • EI = Equity Instrument

- 5. Presentation by: CA Varun Sethi Private CA Varun Sethi 09899766487 IFRS 2R/IndAS 102: Share Based payments Modification / Cancellation/ Settlement of SBP Grant of SBP arrangement Expected to Satisfy vesting condition Modification / Cancellation/ Settlement of SBP 1. Modification is Beneficial to employee or 2. Increases Fair value Recognize compensation cost over the requisite service period Modification increases the FV of the EI granted Modification increases the No. of the EI granted Modification occurs during the vesting period Modification occurs after the vesting date Measurement of Compensation cost= Incremental FV (expensed over modified RSP) ADD: Original FV (unrecognised part expensed over original RSP) Measurement of Compensation cost= Incremental FV (expensed over modified RSP) 1 Refer next slide 2 21 Presentationby:CAVarunSethi Presentationby:CAVarunSethi Paragraphs 26-29 & Appendix B: B42 to B44 NO YESYES

- 6. Presentation by: CA Varun Sethi Private CA Varun Sethi 09899766487 IFRS 2R/IndAS 102: Share Based payments Modification / Cancellation/ Settlement of SBP Grant of SBP arrangement Expected to Satisfy vesting condition Modification occurs during the vesting period Modification occurs after the vesting date Measurement of Compensation cost= Incremental FV (FV of additional EI to be expensed over modified RSP) ADD: Original FV (Grant date based - unrecognised part is expensed over original RSP) Measurement of Compensation cost= Incremental FV (expensed over modified RSP) Refer previous slide Presentationby:CAVarunSethi Presentationby:CAVarunSethi Paragraphs 26-29 & Appendix B: B42 to B44 Modification / Cancellation/ Settlement of SBP 1. Modification is Beneficial to employee or 2. Increases Fair value Recognize compensation cost over the requisite service period Modification increases the FV of the EI granted Modification increases the No. of the EI granted 21 YESYES NO