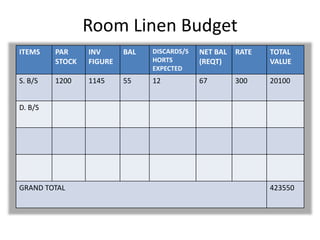

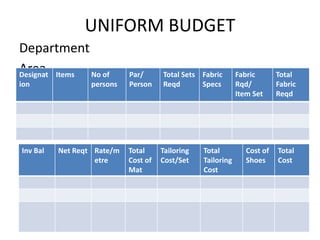

This document discusses budgets in the context of hotel housekeeping. It defines a budget as a financial plan for expected operations and resources over a specified period. The purposes of budgets are to state goals and expectations, communicate expectations, coordinate activities, and measure performance. Advantages include planning, coordination, establishing expectations to judge performance, optimizing resources, and measuring efficiency. Limitations include difficulty establishing realistic objectives and standards. The document then provides examples of housekeeping budget heads and templates for creating linen, guest supplies, table linen, uniform, and capital budgets.