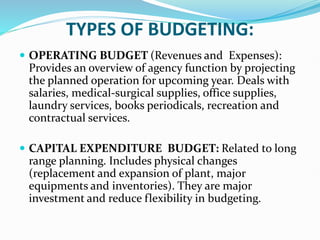

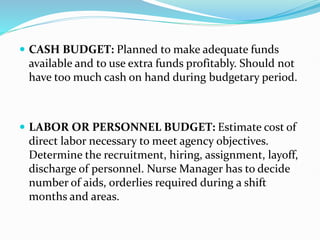

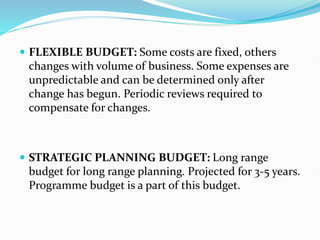

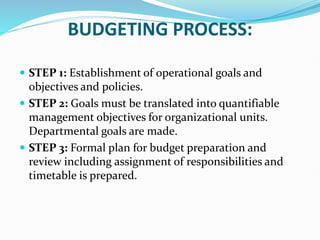

Budgeting is an operational plan expressed in financial terms for a defined period, usually a year. It is based on expected income and expenses. The purposes of budgeting include translating fiscal objectives into spending plans, enhancing fiscal planning, identifying controllable and uncontrollable costs, communicating objectives, allowing feedback, and identifying and solving problems. Budgeting requires an organizational structure, statistical data, chart of accounts, managerial support, and formal budgeting processes and procedures. Types of budgets include operating, capital expenditure, cash, labor, flexible, and strategic planning budgets. The budgeting process involves establishing goals and policies, setting departmental goals, planning preparation and review, developing the master budget, approval and distribution. Budgeting fixes accountability