Recommended

Recommended

More Related Content

Similar to Main ComputationExpectedStandardRisk PremiumReturnMonDeviationE(r.docx

Similar to Main ComputationExpectedStandardRisk PremiumReturnMonDeviationE(r.docx (9)

More from smile790243

More from smile790243 (20)

Recently uploaded

Recently uploaded (20)

Main ComputationExpectedStandardRisk PremiumReturnMonDeviationE(r.docx

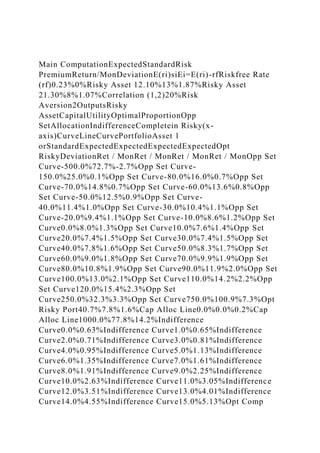

- 1. Main ComputationExpectedStandardRisk PremiumReturn/MonDeviationE(ri)siEi=E(ri)-rfRiskfree Rate (rf)0.23%0%Risky Asset 12.10%13%1.87%Risky Asset 21.30%8%1.07%Correlation (1,2)20%Risk Aversion2OutputsRisky AssetCapitalUtilityOptimalProportionOpp SetAllocationIndifferenceCompletein Risky(x- axis)CurveLineCurvePortfolioAsset 1 orStandardExpectedExpectedExpectedExpectedOpt RiskyDeviationRet / MonRet / MonRet / MonRet / MonOpp Set Curve-500.0%72.7%-2.7%Opp Set Curve- 150.0%25.0%0.1%Opp Set Curve-80.0%16.0%0.7%Opp Set Curve-70.0%14.8%0.7%Opp Set Curve-60.0%13.6%0.8%Opp Set Curve-50.0%12.5%0.9%Opp Set Curve- 40.0%11.4%1.0%Opp Set Curve-30.0%10.4%1.1%Opp Set Curve-20.0%9.4%1.1%Opp Set Curve-10.0%8.6%1.2%Opp Set Curve0.0%8.0%1.3%Opp Set Curve10.0%7.6%1.4%Opp Set Curve20.0%7.4%1.5%Opp Set Curve30.0%7.4%1.5%Opp Set Curve40.0%7.8%1.6%Opp Set Curve50.0%8.3%1.7%Opp Set Curve60.0%9.0%1.8%Opp Set Curve70.0%9.9%1.9%Opp Set Curve80.0%10.8%1.9%Opp Set Curve90.0%11.9%2.0%Opp Set Curve100.0%13.0%2.1%Opp Set Curve110.0%14.2%2.2%Opp Set Curve120.0%15.4%2.3%Opp Set Curve250.0%32.3%3.3%Opp Set Curve750.0%100.9%7.3%Opt Risky Port40.7%7.8%1.6%Cap Alloc Line0.0%0.0%0.2%Cap Alloc Line1000.0%77.8%14.2%Indifference Curve0.0%0.63%Indifference Curve1.0%0.65%Indifference Curve2.0%0.71%Indifference Curve3.0%0.81%Indifference Curve4.0%0.95%Indifference Curve5.0%1.13%Indifference Curve6.0%1.35%Indifference Curve7.0%1.61%Indifference Curve8.0%1.91%Indifference Curve9.0%2.25%Indifference Curve10.0%2.63%Indifference Curve11.0%3.05%Indifference Curve12.0%3.51%Indifference Curve13.0%4.01%Indifference Curve14.0%4.55%Indifference Curve15.0%5.13%Opt Comp

- 2. Port4.5%1.0%Constant Utility Value0.0063Risk aversionWeight TPWeight RFExp. ReturnStd. dev.Utility2.00.57630.42370.01030.04480.0063 Sheet1Risky Asset 1Risky Asset 2MonthBarrickIBMTreasury BillsDec 2009-7.75%3.60%1.137860.158Nov 200919.37%5.22%1.202270.148Oct 2009- 5.20%0.84%1.282780.148Sep 20099.22%1.32%1.121760.178Aug 2009- 0.57%0.57%0.944640.178Jul 20094.02%12.94%0.971480.202Jun 2009-11.90%- 1.75%1.073460.311May 200931.55%3.51%1.014420.316Apr 2009-10.24%6.52%0.976160.38Mar 20097.35%5.28%0.993190.602Feb 2009- 19.45%0.96%0.936430.587Jan 20091.96%8.90%1.03660.612Dec 200824.81%3.14%0.944450.671Nov 200830.43%- 11.69%0.898390.706Oct 2008-38.11%-20.51%1.013560.706Sep 20085.79%-3.92%0.950210.805Aug 2008-17.99%- 4.49%0.921410.795Jul 2008-6.92%7.97%0.852310.735Jun 200812.93%-8.42%0.722740.665May 20084.84%7.65%0.573010.575Apr 2008- 11.12%4.83%0.48950.525Mar 2008- 16.36%1.12%0.564360.565Feb 20080.99%6.68%0.498140.465Jan 200822.33%- 0.92%0.483750.44Dec 20073.80%2.78%0.604680.53Nov 2007- 7.86%-9.08%0.719860.475Oct 20079.56%- 1.43%0.662270.39Sep 200723.86%0.95%0.581650.34Aug 2007- 1.16%5.82%0.547090.28Jul 200713.18%5.13%0.613320.345Jun 2007-0.21%-1.27%0.570130.31May 20074.16%4.69%0.619080.3Apr 2007- 1.54%8.43%0.702580.35Mar 2007-4.42%1.42%0.642110.36Feb 20070.84%-5.96%0.613320.425Jan 2007- 3.52%2.06%0.656510.435Dec 2006-2.35%5.69%0.68530.51Nov 20061.77%-0.12%0.650750.435Oct 20060.91%12.68%0.665150.405Sep 2006- 8.24%1.20%0.549970.44Aug 20068.70%4.99%0.561490.46Jul

- 3. 20064.05%0.77%0.538450.435Jun 2006-3.30%- 3.85%0.498140.445May 20060.79%-2.60%0.477990.405Apr 200611.89%-0.16%0.659390.415Mar 2006- 0.48%2.78%0.771690.435Feb 2006-13.00%- 1.06%0.757290.44Jan 200612.88%-1.09%0.791840.425Dec 20054.74%-7.54%0.555730.64Nov 20055.82%8.82%0.618950.69Oct 2005- 13.08%2.07%0.633480.605Sep 200510.79%- 0.50%0.610240.48Aug 20057.02%-3.16%0.630580.555Jul 2005- 2.12%12.48%0.645110.485Jun 20058.87%- 1.79%0.682880.51May 20053.49%-0.82%0.650920.54Apr 2005- 6.84%-16.42%0.569550.575Mar 2005-3.78%- 1.30%0.473660.58Feb 200513.91%-0.71%0.386480.505Jan 2005-9.74%-5.23%0.317320.48Dec 2004- 1.50%4.61%0.317320.48Nov 20049.73%5.20%Oct 20046.99%4.68%Sep 20045.20%1.24%Aug 20044.60%- 2.53%Jul 2004-3.19%-1.23%Jun 2004-4.45%-0.50%May 20048.06%0.68%Apr 2004-19.13%-4.00%Mar 200416.28%- 4.83%Feb 20043.81%-2.59%Jan 2004-13.25%7.07%Dec 20031.66%2.36%Nov 200315.31%1.36%Oct 20033.40%1.30%Sep 2003-6.83%7.71%Aug 200318.05%1.13%Jul 2003-4.36%-1.52%Jun 20032.40%- 6.29%May 200317.66%3.89%Apr 2003-3.92%8.25%Mar 2003- 3.47%0.62%Feb 2003-2.01%-0.13%Jan 20036.75%0.90%Dec 20025.79%-10.84%Nov 2002-2.65%10.30%Oct 2002- 3.09%35.38%Sep 2002-3.24%-22.65%Aug 20024.90%7.29%Jul 2002-19.33%-2.22%Jun 2002-12.89%-10.50%May 20029.17%- 3.77%Apr 20028.14%-19.46%Mar 20022.83%5.99%Feb 20025.56%-8.93%Jan 20027.21%-10.81%Dec 20015.42%4.65%Nov 2001-2.25%7.09%Oct 2001- 10.14%17.83%Sep 20018.30%-8.23%Aug 20017.59%-4.87%Jul 2001-1.72%-6.89%Jun 2001-8.18%1.07%May 20011.03%- 2.78%Apr 200115.05%19.71%Mar 2001-11.79%-3.72%Feb 20014.72%-10.69%Jan 2001-5.56%31.76%Dec 20009.20%- 9.09%Nov 200012.97%-4.94%Oct 2000-12.30%-12.44%Sep 2000-4.31%-14.77%Aug 20000.00%17.51%Jul 2000-

- 4. 12.37%2.62%Jun 20000.34%2.04%May 20008.46%-3.58%Apr 20007.17%-5.51%Mar 2000-3.83%14.84%Feb 2000-0.38%- 8.36%Jan 2000-7.42%4.06%Average ReturnStandard Deviation Chart 1 Risky Opportunity Set, Capital Allocation Line, and Indifference Curve Risk Free 0 2.3E-3 Risky Asset 1 0.13 2.1000000000000001E-2 Risky Asset 2 0.08 1.2999999999999999E-2 Complete Portfolio 4.4841306731903098E-2 1.0342971157698472E-2 Optimum Portfolio 7.7808710077419324E-2 1.6256176939981118E-2 Portfolio Frontier 0.72670489196096655 0.24984995497297974 0.15987995496621835 0.14773828210724529 0.13592056503708333 0.12451907484397723 0.11365913953571882 0.10351135203445079 9.4305885288246918E-2 8.6344658201882932E-2 7.9999999999999946E-2 7.5679587736720635E-2 7.3740084079149254E-2 7.4368003872633287E-2 7.7500967735893461E-2 8.2855295545909438E-2 9.0035548535009224E-2 9.8643803657401621E-2 0.10834020491027328 0.11885873968707561 0.13 0.14161708936424308 0.15360208331920502 0.3231485726411305 1.0090713552569015 - 2.700000000000001E-2 1.0000000000000009E-3 6.5999999999999982E-3 7.3999999999999986E-3 8.199999999999999E-3 8.9999999999999993E-3 9.7999999999999962E-3 1.0599999999999998E-2 1.1400000000000007E-2 1.2200000000000009E-2

- 5. 1.3000000000000008E-2 1.3800000000000007E-2 1.46E-2 1.5399999999999999E-2 1.6199999999999999E-2 1.7000000000000001E-2 1.78E-2 1.8599999999999998E-2 1.9400000000000001E-2 2.0199999999999999E-2 2.1000000000000001E-2 2.18E-2 2.2600000000000002E-2 3.3000000000000002E-2 7.3000000000000009E-2 CML0 0.77808710077419319 2.3E-3 0.14186176939981118 Indifference Curve 0 0.01 0.02 0.03 0.04 0.05 0.06 7.0000000000000007E-2 0.08 0.09 0.1 0.11 0.12 0.13 0.14000000000000001 0.15 6.3214855788492359E-3 6.5214855788492355E-3 7.1214855788492362E-3 8.1214855788492354E-3 9.5214855788492356E-3 1.1321485578849237E-2 1.3521485578849236E-2 1.6121485578849237E-2 1.9121485578849236E-2 2.2521485578849233E-2 2.6321485578849238E-2 3.0521485578849233E-2 3.5121485578849233E-2 4.0121485578849238E-2 4.552148557884924E-2 5.1321485578849232E-2 The Risky Asset 1 and 2 0 0.13 0.08 2.3E-3 2.1000000000000001E-2 1.2999999999999999E-2 Standard Deviation (s) Expected Return / Month (1)

- 6. BUS329 (Investment Analysis) Assignment: How to download data from Yahoo Finance This guidelines show you how to download stock price data from Yahoo Finance. The first part is related to data you need to construct optimal complete portfolio and the second part is related to data you need to calculate systematic risks. First part: Constructing optimal complete portfolio (1) This part of the assignment is about constructing optimal complete portfolio with two risky assets and one risk-free asset. (2) For risk-free rate use 1 month Bank Accepted Bill (BAB) rate available on Reserve Bank of Australia (RBA) website as follow: (http://www.rba.gov.au/statistics/tables/#interest-rates) (Take the average of BAB rate during your sample period). You will need to click “Interest Rates and Yield – Money Market – Monthly – F1.1” to get this data. After clicking an excel file will be

- 7. downloaded, where you will find 1-moth BAB rate. (3) For risky assets choose two stocks from Australia Stock Exchange (ASX) (4) Download stock price data from Yahoo Finance for free (website: https://au.finance.yahoo.com/q/hp?s=ASX.AX) (5) How to download data from Yahoo Finance website: You need to enter stock symbol here to download the price of your selected stock. (6) Stock symbols are available in ASX website (http://www.asx.com.au/asx/research/listedCompanies.do). Clicking this link will give you the following web page: http://www.rba.gov.au/statistics/tables/#interest-rates https://au.finance.yahoo.com/q/hp?s=ASX.AX http://www.asx.com.au/asx/research/listedCompanies.do (2)

- 8. (7) You need to use these ASX codes (this is what we call symbol above) to download stock price. For example, suppose you want to download stock price of ABACUS PROPERTY GROUP. Code for this stock is ABP. So you type ABP in the box and click „Look Up‟ as follows: (8) This will return the following page: (9) Now click „Historical Prices‟. This will return the following page: (3) (10) Now select your start and end date here. Download monthly data by clicking „Monthly‟. I strongly recommend using monthly data to avoid the complexities of handling public holidays, non-trading day etc. Once you have selected start and end date and checked „Monthly‟, click „Get Prices‟ to download the data. When

- 9. data download is complete, go to the bottom of the page and click „Download to SpreadSheet‟ to get data in CSV format. Finally save the data as per your convenience. For analysis purpose use the stock price along the „Adj Close‟ column (11) Repeat the same process to download your second stock price data. (12) Use monthly data from July 2008 to December 2016. (13) Next you will need to calculate stock return from stock prices. Use the following formula to calculate the return series: (4) 100 1

- 10. t tt t P PP r (1) For example, in the screenshot below „Adj Close‟ price on 1 June 2016 is AU$3.07 and that on 1 July 2016 is AU$3.10. Therefore return on 1 July 2016 is calculated as follows: %98.0 100 07.3$ 07.3$10.3$ 20161

- 11. AU AUAU r July Using stock price data the return series can easily be generated in excel. (14) If the data are downloaded from ‘New’ to ‘Old’, then you need to convert them from ‘Old’ to ‘New’. For example, in the screenshot above 1 July, 2016 data come first and then 1 June 2016 – this is ‘New’ to ‘Old’ pattern. You will need to convert them to ‘Old’ to ‘New’ form. This can easily be done by using ‘Sort’ under ‘Data’ in Excel (15) For your analysis you will need to calculate variance, covariance, standard deviation etc. for the stock return series. You can calculate these by using

- 12. formulas in excel. Please visit the following YouTube website to see how excel can be used to calculate those statistics: https://www.youtube.com/results?search_query=how+to+calcula te+variance%2C+covarian ce+in+excel (16) Calculate optimum weights of two risky assets (say, asset S and Asset B) by using the following formula [this is similar to the formula given in Equation 7.13 (page 217) of your text] https://www.youtube.com/results?search_query=how+to+calcula te+variance%2C+covariance+in+excel https://www.youtube.com/results?search_query=how+to+calcula te+variance%2C+covariance+in+excel (5) Use average of stock returns calculated using formula (1) above as a proxy for expected return, E(r), in the above equation. Similarly use the average of risk-free rate as a proxy

- 13. for rf in the above equation. (17) You will also be required a value for risk aversion coefficient, A. It is not available anywhere. It is a subjective value. Use any one of the following three risk aversion coefficients: (a) Highly risk-averse investor: if you think you are highly risk averse, then use 5 as your risk-aversion coefficient (i.e., A = 5) (b) Moderate risk-averse investor: if you think you are moderately risk averse, then use 4 as your risk-aversion coefficient (i.e., A = 4) (c) Low risk-averse investor: if you think you are low risk- averse investor, then use 3 as your risk-aversion coefficient (i.e., A = 3) (18) Split the whole sample into two sub-periods: (a) From July 2008 to December 2011 (this period is a proxy for Global Financial Crisis (GFC). (b) From January 2012 to December 2016 (this period is a proxy for post Global Financial Crisis (post-GFC).

- 14. (6) Second part: Systematic risk of the risky assets (1) In this part of the assignment you will be required to calculate the systematic risk of the risky assets, that is, two stocks used in Part A of the assignment. In other words, you are required to calculate β (beta) of each stock. (2) Split the whole sample into two sub-periods: (3) From July 2008 to December 2011 (this period is a proxy for Global Financial Crisis (GFC) and hence is expected to capture the effect of GFC on stocks‟ systematic risk) (4) From January 2012 to December 2016 (this period is a proxy for post Global Fnancial Crisis (post-GFC) and hence is expected to capture the stocks‟ systematic

- 15. risk during post-GFC period) (5) You can calculate beta by using the following formula: M Mi i rVar rrCov , here rM is return on market portfolio. You can use ASX All Ordinary index as a proxy for market portfolio. (6) To download ASX All Ordinary index data type „^AORD‟ in the box as below: (7) Now click „Look Up‟, which will return the following page. (7)

- 16. (8) Now click „Historical Prices‟ and download ASX All Ordinary index following steps described in above. (9) Calculate ASX All Ordinary index return using formula given in eq (1) above. (10) Calculate covariance between stock return and index return (you will need to calculate two co-variances for two stock returns. (11) Calculate variance of index return (12) Finally calculate beta using formula in equation (2) above. (13) Compare the betas (GFC beta vs post-GFC beta) Important Note: This is a group assignment. Each group will work on two firms‟ stock price data; however, each group has to work on different pair of firms‟ stock prices. For example, if Group 1 is works on Firm A and Firm B, no other group can work on Firm A and Firm B data; another group can work on Firm A and Firm C data or Firm B and Firm C data.

- 17. Remember exactly same two forms‟ data cannot be used by multiple groups. If two groups work on exactly same two firms’ data, they will arrive at exactly same result, which will be treated as serious type of plagiarism. So using exactly same two firms‟ data by more than one group is strictly prohibited.