This document provides an overview of cost-volume-profit (CVP) analysis and how it can be used to answer questions about sales volumes, costs, income, and break-even points. It discusses identifying cost behavior as fixed, variable, or mixed; measuring cost behavior using scatter diagrams, the high-low method, and least-squares regression; using break-even analysis to determine the sales volume or dollars needed to cover fixed costs; computing income from sales and costs data; and sensitivity analysis of changes to estimates. Multiproduct CVP analysis and degree of operating leverage are also covered.

![22 - 23

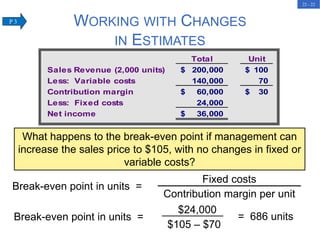

Income (pretax) = Sales – Variable costs – Fixed costs

COMPUTING INCOME

FROM SALES AND COSTS

Rydell expects to sell 1,500 units at $100 each next month.

Fixed costs are $24,000 per month and the unit variable

cost is $70. What amount of income should Rydell expect?

Income (pretax) = Sales – Variable costs – Fixed costs

= [1,500 units × $100] – [1,500 units × $70] – $24,000

= $21,000

C 2](https://image.slidesharecdn.com/chap022-221224195909-3055797a/85/Chap022-ppt-23-320.jpg)