Downloaded 32 times

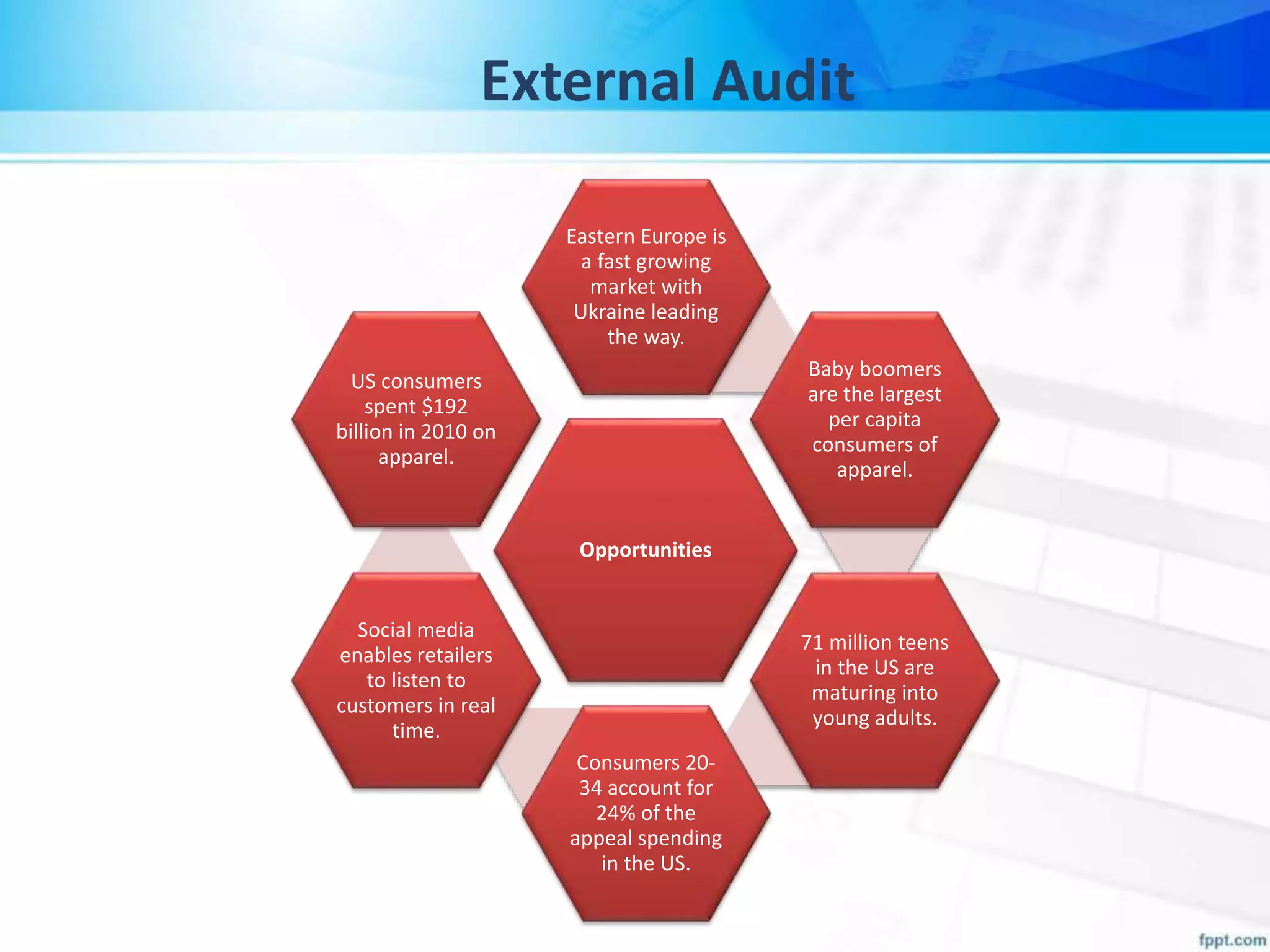

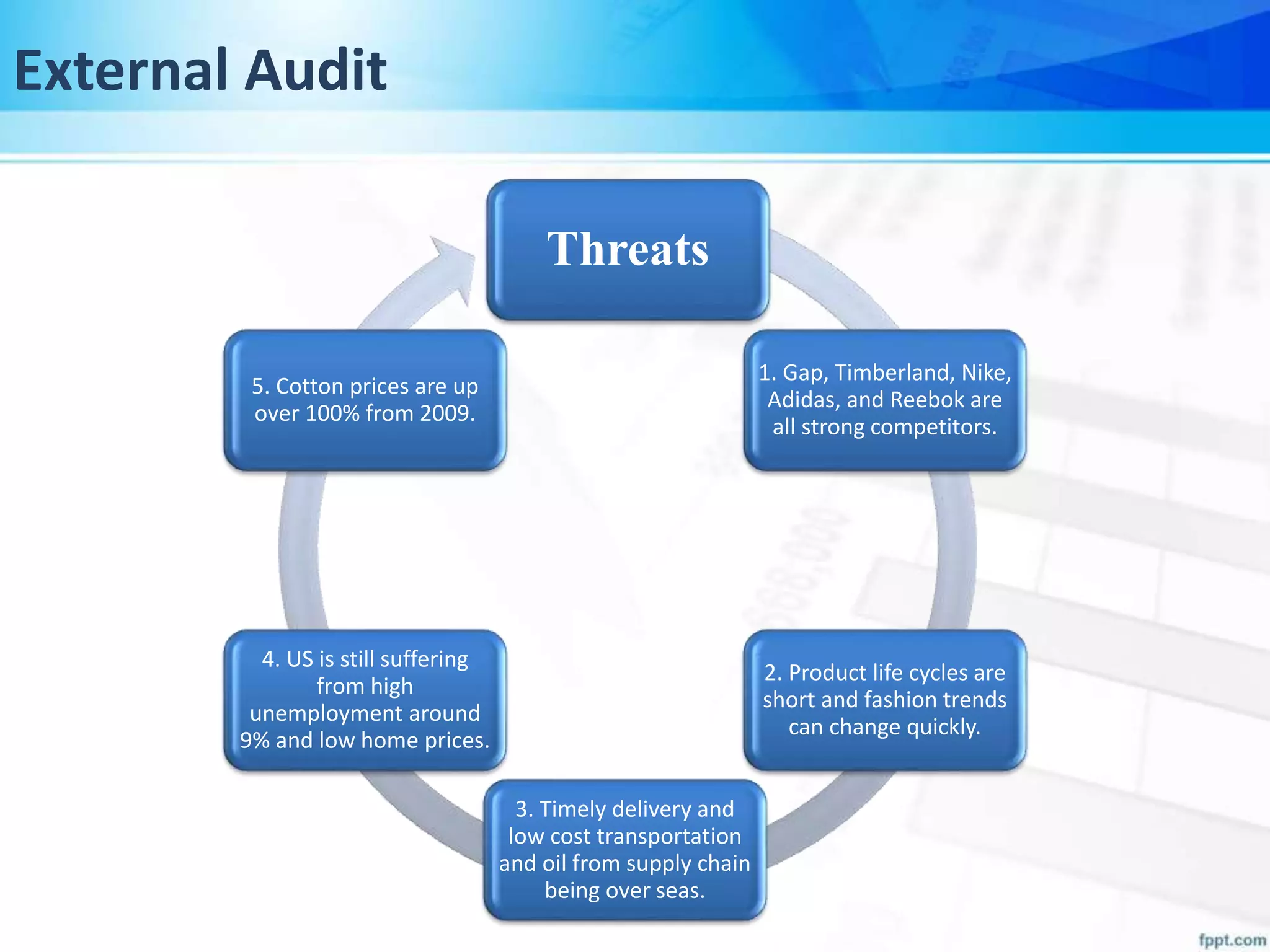

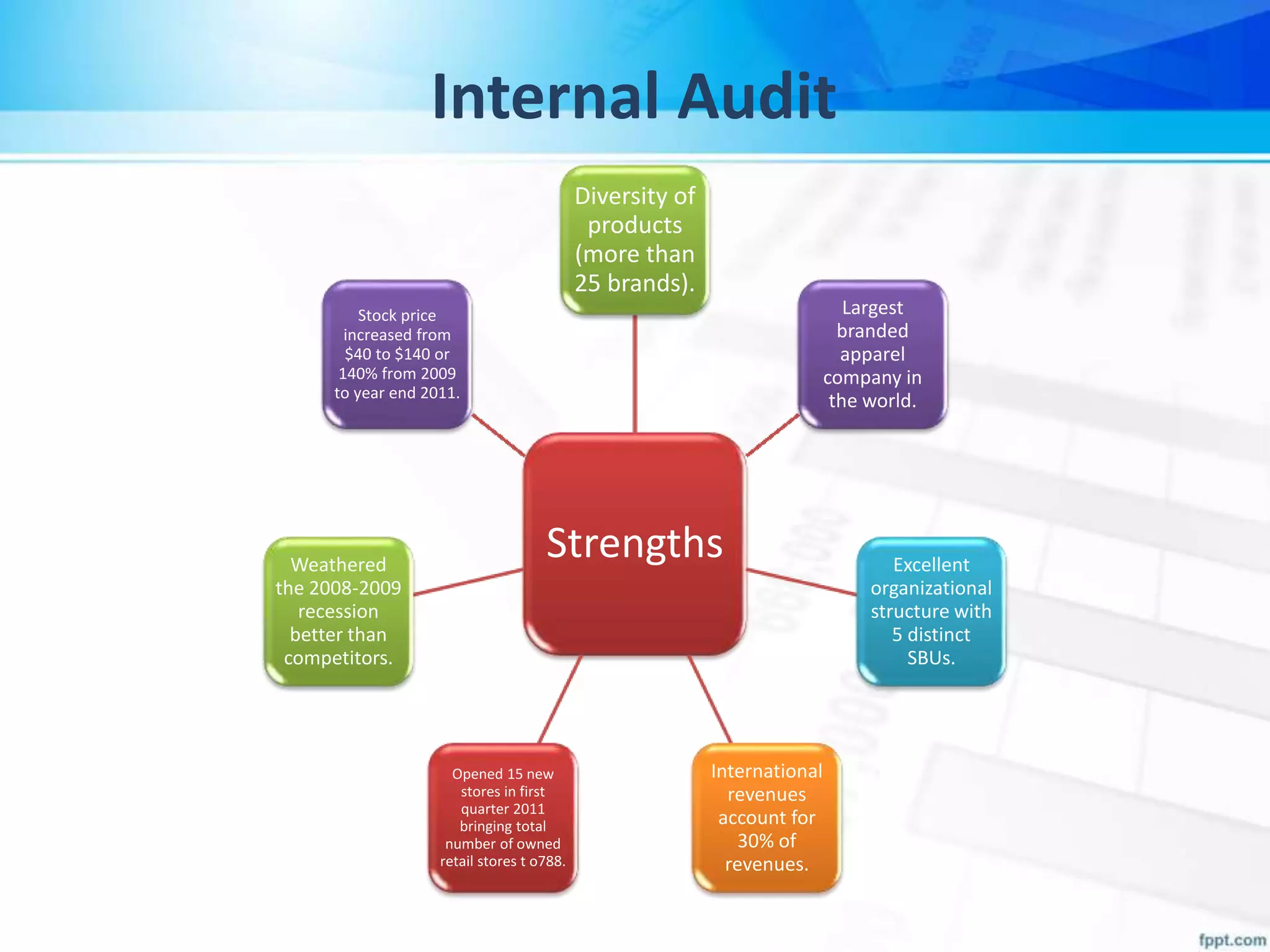

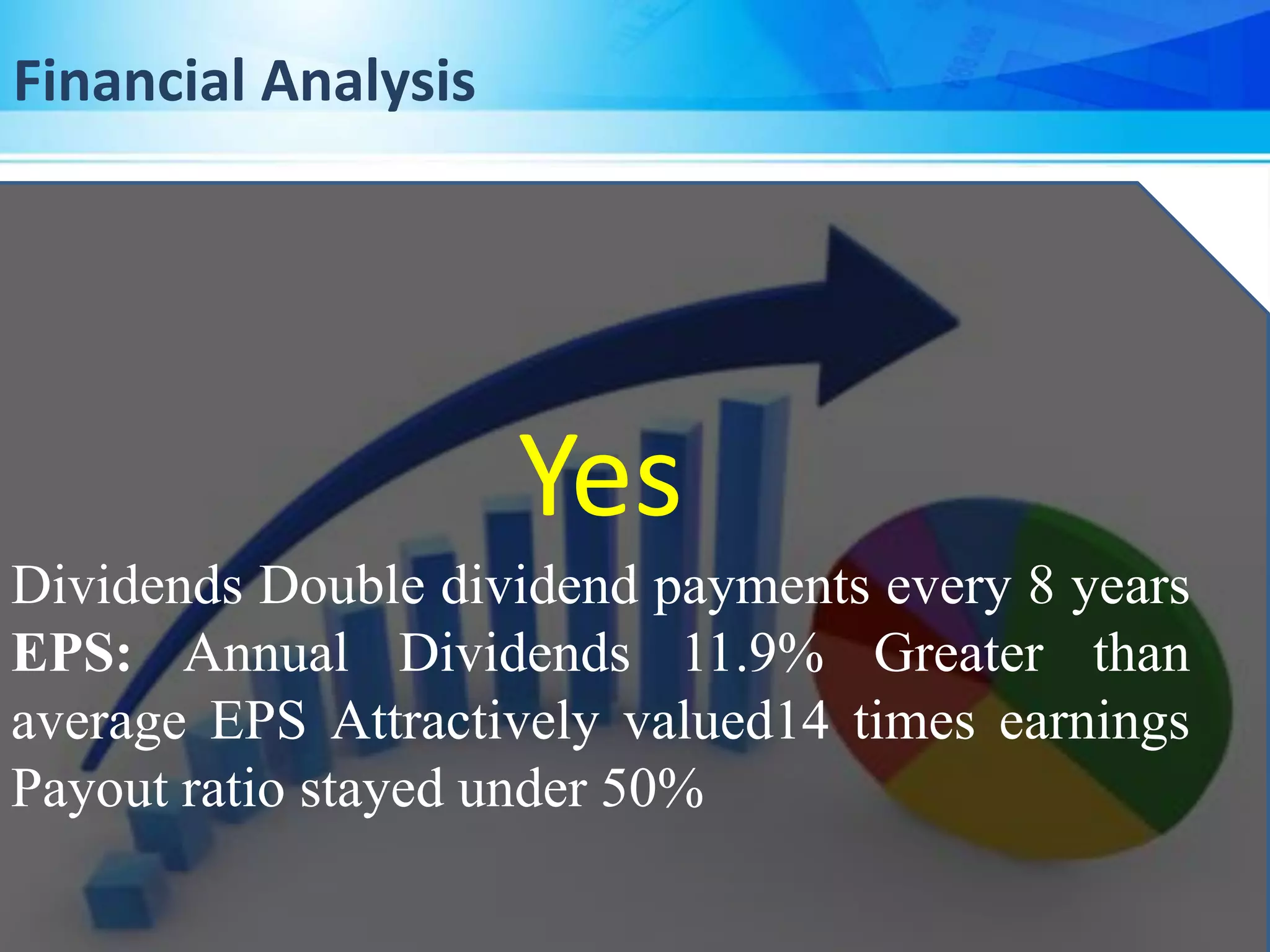

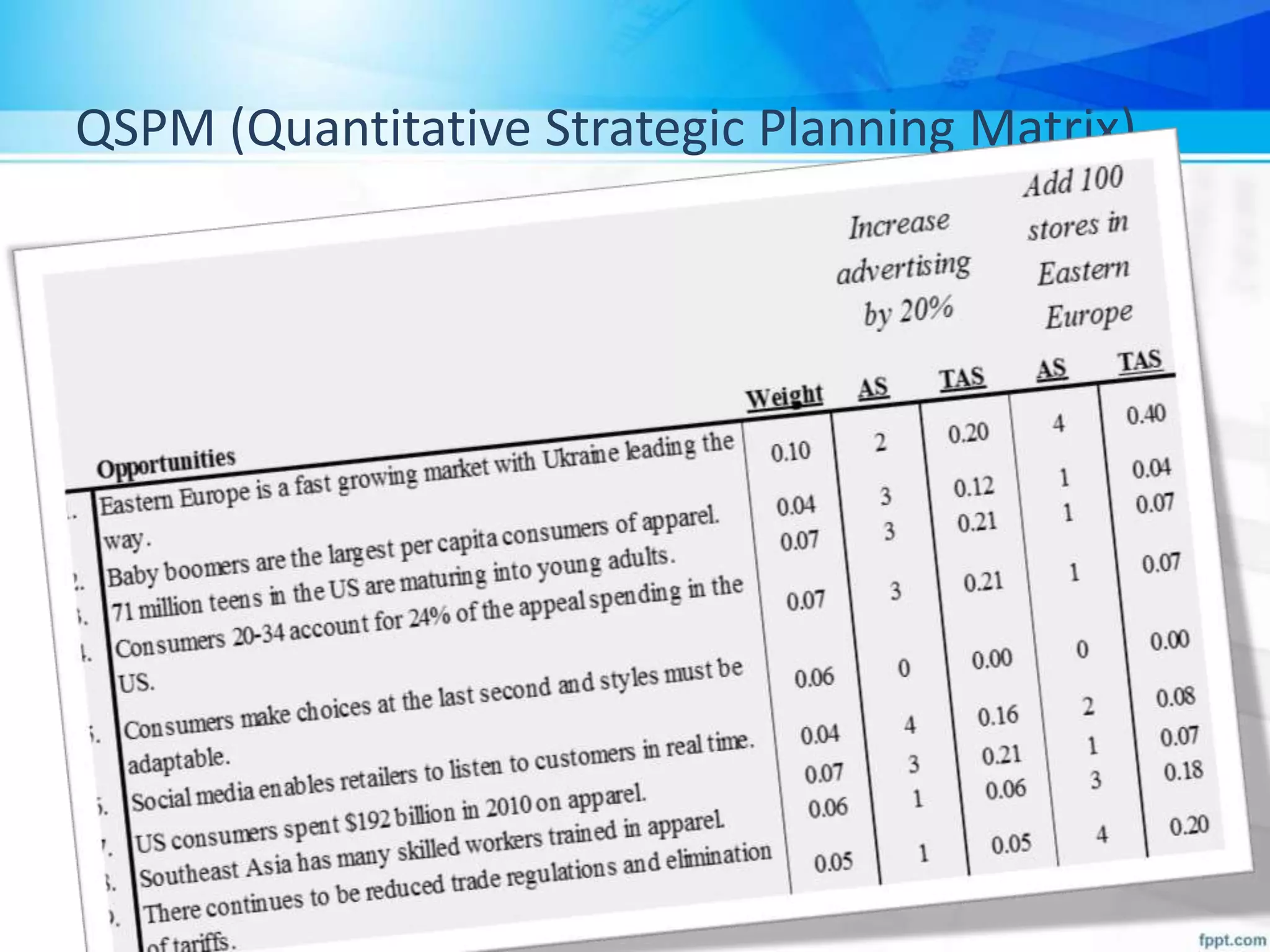

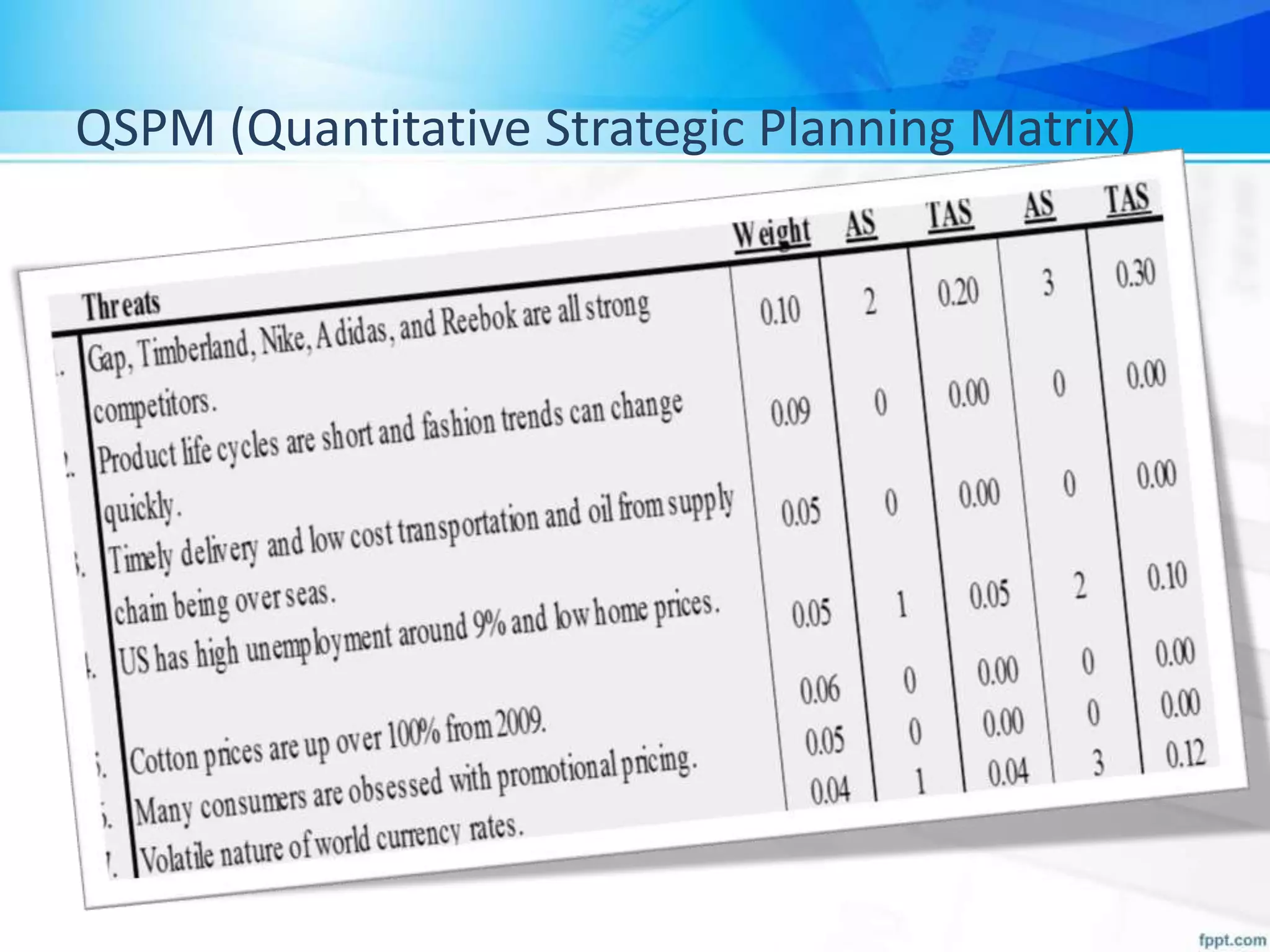

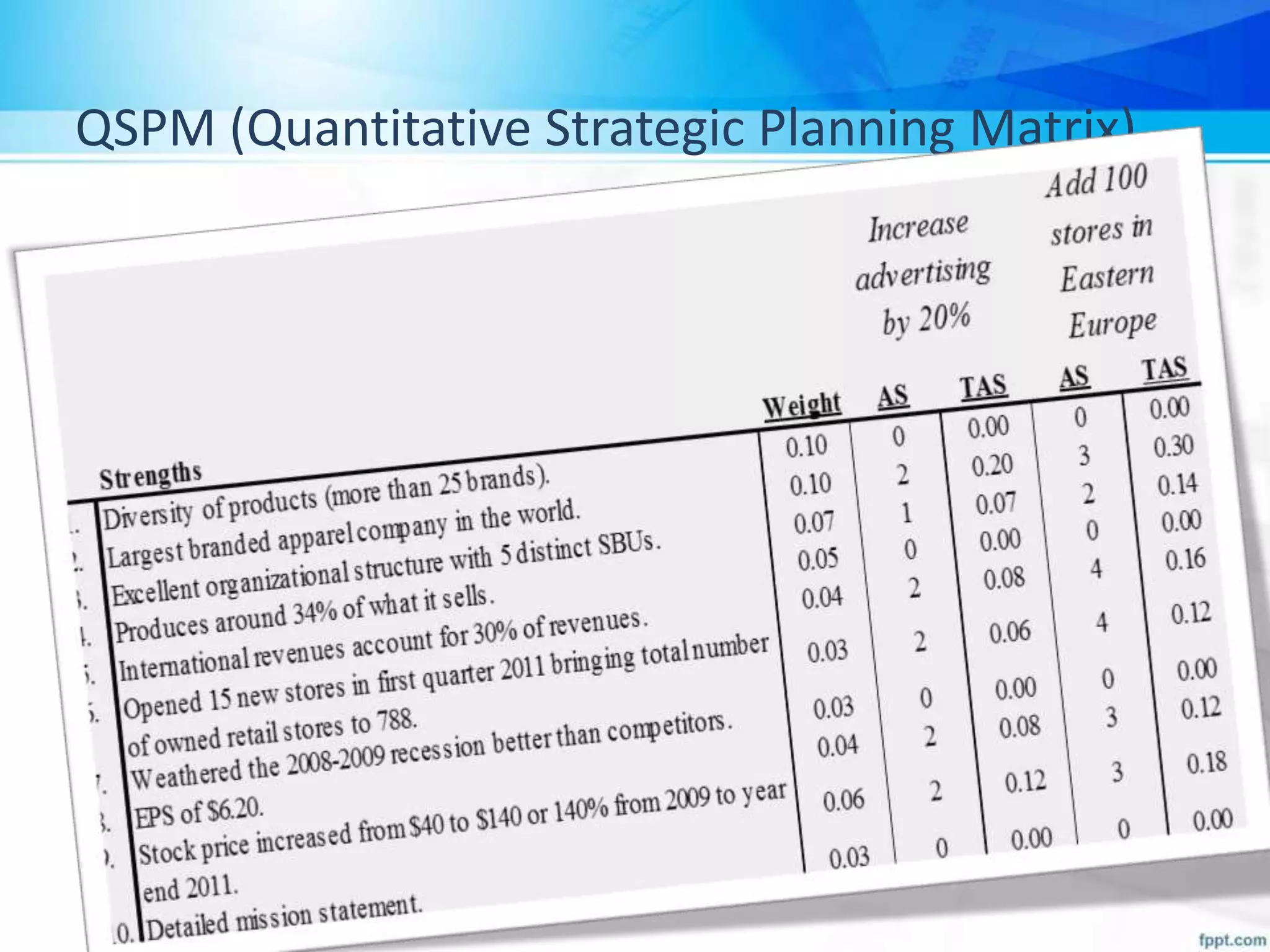

VF Corporation aims to grow by building leading lifestyle brands and fostering a culture of innovation and diversity. They face competition from major brands and challenges with product life cycles, but have strengths in their organizational structure and market position. The company seeks to expand its presence, particularly in Eastern Europe, and improve operational efficiency while maintaining strong financial metrics.