Download as PDF, PPTX

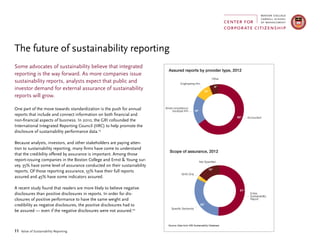

This document summarizes a study conducted by the Boston College Center for Corporate Citizenship and Ernst & Young LLP on the value of sustainability reporting. Some key findings from the study include: - Sustainability reporting can provide major value to companies in areas like improved reputation, increased employee loyalty, risk management, and access to capital. - The majority (95%) of large global companies now issue sustainability reports, with the Global Reporting Initiative framework being the most widely used standard. - While data availability and resources remain challenges, transparency with stakeholders is a major motivation for companies to report across all industries.